Signature Revocable Living Trust Made Easy

Award-winning eSignature solution

Do more on the web with a globally-trusted eSignature platform

Outstanding signing experience

Trusted reports and analytics

Mobile eSigning in person and remotely

Industry polices and conformity

Signature revocable living trust, quicker than ever before

Useful eSignature extensions

See airSlate SignNow eSignatures in action

airSlate SignNow solutions for better efficiency

Our user reviews speak for themselves

Why choose airSlate SignNow

-

Free 7-day trial. Choose the plan you need and try it risk-free.

-

Honest pricing for full-featured plans. airSlate SignNow offers subscription plans with no overages or hidden fees at renewal.

-

Enterprise-grade security. airSlate SignNow helps you comply with global security standards.

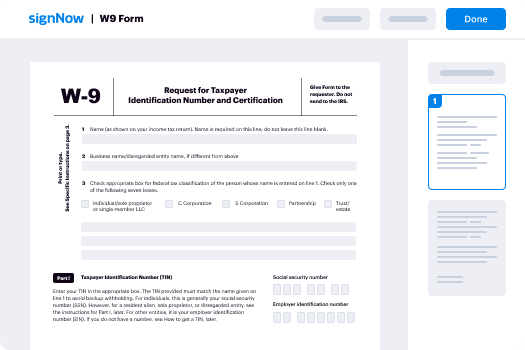

Your step-by-step guide — signature revocable living trust

Leveraging airSlate SignNow’s electronic signature any company can enhance signature workflows and eSign in real-time, giving a better experience to consumers and employees. Use signature Revocable Living Trust in a few simple actions. Our handheld mobile apps make operating on the run achievable, even while off-line! Sign signNows from any place in the world and close up trades in less time.

Follow the stepwise guide for using signature Revocable Living Trust:

- Log in to your airSlate SignNow profile.

- Locate your record in your folders or import a new one.

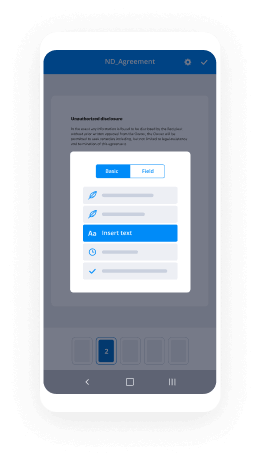

- Open up the template adjust using the Tools list.

- Drag & drop fillable boxes, type text and eSign it.

- Include numerous signees via emails configure the signing sequence.

- Specify which users can get an signed version.

- Use Advanced Options to limit access to the record and set up an expiry date.

- Press Save and Close when completed.

Additionally, there are more advanced features available for signature Revocable Living Trust. Include users to your common digital workplace, view teams, and keep track of cooperation. Numerous consumers all over the US and Europe agree that a system that brings people together in one cohesive digital location, is exactly what enterprises need to keep workflows working smoothly. The airSlate SignNow REST API allows you to integrate eSignatures into your app, website, CRM or cloud storage. Check out airSlate SignNow and get faster, smoother and overall more productive eSignature workflows!

How it works

airSlate SignNow features that users love

See exceptional results signature Revocable Living Trust made easy

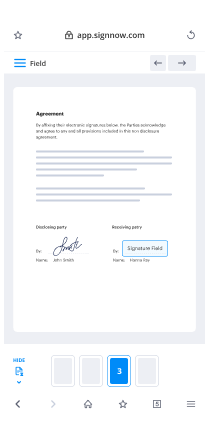

How to submit and eSign a document online

Try out the fastest way to signature Revocable Living Trust. Avoid paper-based workflows and manage documents right from airSlate SignNow. Complete and share your forms from the office or seamlessly work on-the-go. No installation or additional software required. All features are available online, just go to signnow.com and create your own eSignature flow.

A brief guide on how to signature Revocable Living Trust in minutes

- Create an airSlate SignNow account (if you haven’t registered yet) or log in using your Google or Facebook.

- Click Upload and select one of your documents.

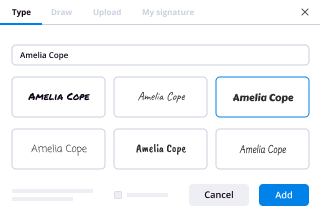

- Use the My Signature tool to create your unique signature.

- Turn the document into a dynamic PDF with fillable fields.

- Fill out your new form and click Done.

Once finished, send an invite to sign to multiple recipients. Get an enforceable contract in minutes using any device. Explore more features for making professional PDFs; add fillable fields signature Revocable Living Trust and collaborate in teams. The eSignature solution supplies a protected workflow and functions according to SOC 2 Type II Certification. Ensure that your records are guarded and therefore no one can take them.

How to eSign a PDF file in Google Chrome

Are you looking for a solution to signature Revocable Living Trust directly from Chrome? The airSlate SignNow extension for Google is here to help. Find a document and right from your browser easily open it in the editor. Add fillable fields for text and signature. Sign the PDF and share it safely according to GDPR, SOC 2 Type II Certification and more.

Using this brief how-to guide below, expand your eSignature workflow into Google and signature Revocable Living Trust:

- Go to the Chrome web store and find the airSlate SignNow extension.

- Click Add to Chrome.

- Log in to your account or register a new one.

- Upload a document and click Open in airSlate SignNow.

- Modify the document.

- Sign the PDF using the My Signature tool.

- Click Done to save your edits.

- Invite other participants to sign by clicking Invite to Sign and selecting their emails/names.

Create a signature that’s built in to your workflow to signature Revocable Living Trust and get PDFs eSigned in minutes. Say goodbye to the piles of papers sitting on your workplace and begin saving money and time for more essential activities. Picking out the airSlate SignNow Google extension is a smart practical choice with many different advantages.

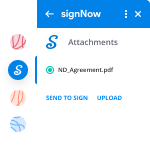

How to sign an attachment in Gmail

If you’re like most, you’re used to downloading the attachments you get, printing them out and then signing them, right? Well, we have good news for you. Signing documents in your inbox just got a lot easier. The airSlate SignNow add-on for Gmail allows you to signature Revocable Living Trust without leaving your mailbox. Do everything you need; add fillable fields and send signing requests in clicks.

How to signature Revocable Living Trust in Gmail:

- Find airSlate SignNow for Gmail in the G Suite Marketplace and click Install.

- Log in to your airSlate SignNow account or create a new one.

- Open up your email with the PDF you need to sign.

- Click Upload to save the document to your airSlate SignNow account.

- Click Open document to open the editor.

- Sign the PDF using My Signature.

- Send a signing request to the other participants with the Send to Sign button.

- Enter their email and press OK.

As a result, the other participants will receive notifications telling them to sign the document. No need to download the PDF file over and over again, just signature Revocable Living Trust in clicks. This add-one is suitable for those who choose working on more valuable things rather than burning time for nothing. Improve your daily monotonous tasks with the award-winning eSignature application.

How to eSign a PDF template on the go without an application

For many products, getting deals done on the go means installing an app on your phone. We’re happy to say at airSlate SignNow we’ve made singing on the go faster and easier by eliminating the need for a mobile app. To eSign, open your browser (any mobile browser) and get direct access to airSlate SignNow and all its powerful eSignature tools. Edit docs, signature Revocable Living Trust and more. No installation or additional software required. Close your deal from anywhere.

Take a look at our step-by-step instructions that teach you how to signature Revocable Living Trust.

- Open your browser and go to signnow.com.

- Log in or register a new account.

- Upload or open the document you want to edit.

- Add fillable fields for text, signature and date.

- Draw, type or upload your signature.

- Click Save and Close.

- Click Invite to Sign and enter a recipient’s email if you need others to sign the PDF.

Working on mobile is no different than on a desktop: create a reusable template, signature Revocable Living Trust and manage the flow as you would normally. In a couple of clicks, get an enforceable contract that you can download to your device and send to others. Yet, if you really want an application, download the airSlate SignNow mobile app. It’s secure, fast and has an incredible layout. Enjoy easy eSignature workflows from your office, in a taxi or on an airplane.

How to sign a PDF file having an iPad

iOS is a very popular operating system packed with native tools. It allows you to sign and edit PDFs using Preview without any additional software. However, as great as Apple’s solution is, it doesn't provide any automation. Enhance your iPhone’s capabilities by taking advantage of the airSlate SignNow app. Utilize your iPhone or iPad to signature Revocable Living Trust and more. Introduce eSignature automation to your mobile workflow.

Signing on an iPhone has never been easier:

- Find the airSlate SignNow app in the AppStore and install it.

- Create a new account or log in with your Facebook or Google.

- Click Plus and upload the PDF file you want to sign.

- Tap on the document where you want to insert your signature.

- Explore other features: add fillable fields or signature Revocable Living Trust.

- Use the Save button to apply the changes.

- Share your documents via email or a singing link.

Make a professional PDFs right from your airSlate SignNow app. Get the most out of your time and work from anywhere; at home, in the office, on a bus or plane, and even at the beach. Manage an entire record workflow seamlessly: generate reusable templates, signature Revocable Living Trust and work on documents with partners. Transform your device into a powerful company for closing offers.

How to sign a PDF Android

For Android users to manage documents from their phone, they have to install additional software. The Play Market is vast and plump with options, so finding a good application isn’t too hard if you have time to browse through hundreds of apps. To save time and prevent frustration, we suggest airSlate SignNow for Android. Store and edit documents, create signing roles, and even signature Revocable Living Trust.

The 9 simple steps to optimizing your mobile workflow:

- Open the app.

- Log in using your Facebook or Google accounts or register if you haven’t authorized already.

- Click on + to add a new document using your camera, internal or cloud storages.

- Tap anywhere on your PDF and insert your eSignature.

- Click OK to confirm and sign.

- Try more editing features; add images, signature Revocable Living Trust, create a reusable template, etc.

- Click Save to apply changes once you finish.

- Download the PDF or share it via email.

- Use the Invite to sign function if you want to set & send a signing order to recipients.

Turn the mundane and routine into easy and smooth with the airSlate SignNow app for Android. Sign and send documents for signature from any place you’re connected to the internet. Build professional-looking PDFs and signature Revocable Living Trust with a few clicks. Come up with a faultless eSignature workflow with just your smartphone and enhance your general efficiency.

Get legally-binding signatures now!

FAQs

-

How do you sign a revocable trust?

To register a revocable living trust, the trustee must file a statement with the court where the trustee resides or keeps trust records. The statement must include: the name and address of the trustee. an acknowledgment of the trusteeship. -

What is the main purpose of a trust?

What Is a Trust? A trust is traditionally used for minimizing estate taxes and can offer other benefits as part of a well-crafted estate plan. A trust is a fiduciary arrangement that allows a third party, or trustee, to hold assets on behalf of a beneficiary or beneficiaries. -

Why would a person want to set up a trust?

The trust holds property or assets for a specific person or group, called the beneficiary. ... There are many reasons to set up a trust, including avoiding probate, providing for your family after your death, and stating exactly how, and when, your descendants receive their inheritance. -

What assets should be placed in a revocable trust?

Generally, assets you want in your trust include real estate, bank/saving accounts, investments, business interests and notes payable to you. You will also want to change most beneficiary designations to your trust so those assets will flow into your trust and be part of your overall plan. -

How does a revocable trust work?

At the most basic level, a revocable living trust, also known simply as a revocable trust, is a written document that determines how your assets will be handled after you die. ... Assets you place in the trust are then transferred to your designated beneficiaries upon your death. -

What are the advantages of having a trust?

Among the chief advantages of trusts, they let you: Put conditions on how and when your assets are distributed after you die; Reduce estate and gift taxes; Distribute assets to heirs efficiently without the cost, delay and publicity of probate court. -

What should be included in a revocable trust?

A Revocable Living Trust Defined Assets can include real estate, valuable possessions, bank accounts and investments. As with all living trusts, you create it during your lifetime. (There are also testamentary trusts, which don't take effect until after you die.) -

What are the advantages of a revocable trust?

A living trust saves your family time and money by avoiding probate -- and it confers several additional benefits as well. By Mary Randolph, J.D. The main benefit of a revocable living trust is that it saves your family time and money by avoiding probate after your death. -

Does a trust need to be recorded in Arizona?

Do I Need a Living Trust in Arizona? ... A living trust allows you to preempt probate, so there is never a court proceeding or any public record of what property you leave at your death and to whom you leave it. -

How much does it cost to set up a revocable trust?

Assuming you decide you want a revocable living trust, how much should you expect to pay? If you are willing to do it yourself, it will cost you about $30 for a book, or $60 for living trust software. If you hire a lawyer to do the job for you, get ready to pay between $1,200 and $2,000. -

How much does it cost to change a living trust?

We also reserve the right to modify our fees at any time. Typical pricing is as follows: $300 to Amend Nomination of Successor Trustees & Executors. $400 minimum to Amend Gift, Inheritance & Beneficiary Provisions. -

Who needs a revocable trust?

Single People. Anyone who is single and has assets titled in their sole name should consider a Revocable Living Trust. The two main reasons are to keep you and your assets out of a court-supervised guardianship and to allow your beneficiaries to avoid the costs and hassles of probate. -

Can you make changes to a trust?

You can make changes to your trust in one of three ways. ... Sign a complete revocation of the original trust agreement and any amendments, then transfer the assets held in the revoked trust back into your own name. You can then create and fund a brand new revocable living trust if you choose. -

Do I need a revocable trust if I have a will?

But you still need a will since most trusts deal only with specific assets such as life insurance or a piece of property, but not the sum total of your holdings. Even if you have what's known as a revocable living trust in which you can put the bulk of your assets, you still need what's known as a pour-over will. -

What happens to a joint revocable trust when one spouse dies?

For a married couple, a joint revocable living trust means that both spouse's assets are held jointly in one trust. ... At the first spouse' death, the trust could direct that the trust be divided into two shares, the decedent's share and the survivor's share. The survivor's share can continue under the joint trust name.

What active users are saying — signature revocable living trust

Related searches to signature Revocable Living Trust made easy

E signature revocable living trust

hey so in this video I'm going to explain the gradual trends that have occurred up until 2020 in the area of a revocable living trust so I'm Paul Rabelais I'm an estate planning attorney I've helped thousands of clients get them keep their legal affairs in order first thing I want to say is happy new year I'm creating this video on January 1st 2020 new year new year new decade a lot to look forward to will have to look forward to on this YouTube channel okay so in in really all areas of law and finance we see gradual you know trends and it's no different in the area of estate planning and revocable living trusts so before I get into the the specific trends that I see I got to give you the background and the introduction of start with really what is a revocable living trust let me give you some background because when you die with certain assets in your name assets like real estate like a home assets like investments stock and shares of mutual funds if those things are in your name when you pass away those assets are gonna be frozen because it was determined years ago that our government our judicial system would oversee the administration the transfer and the disposition and disbursement of assets in your name when you die so when you die with assets in your name whether you have a will or whether you don't have a will but if you die with assets in your name your assets are frozen and your survivors will see a an attorney like myself and it's likely that you know many court documents will be prepared inventory all of the assets and debts that you own all these court pleadings will be filed at the local courthouse a judge will be assigned to the proceeding and if all of the paperwork you know is submitted accurately and timely than the then the judges sign the appropriate court orders and those court orders get submitted to the financial institutions where you have accounts and those accounts are frozen so the financial institutions lawyers will review the court orders and if everything looks good those court orders will order the financial institution to release the funds to your executor or to your heirs whatever the case may be those court orders will be filed in the real estate records where you own real estate and that will transfer the title of the real estate that you own and then those court orders will be given to other third parties ordering them to retitle assets from the name of the person who died into the names of the heirs so this this whole process of when someone dies assets frozen survivors hire lawyers courts oversee the whole process this is what's called probate he didn't hear where I live in Louisiana we call it succession it's the same thing but too many and look realize this is done at what is for many families a very difficult time because they just they just lost a family member and they're grieving so this process is perceived to as being you know expensive several thousand dollars to tens of thousands style of dollars it's perceived as being time-consuming several months two years and it's perceived as just an all-around hassle and inconvenience so some people in an attempt to make their estate settlement simpler by avoiding all of the government involvement the court supervision the attorney involvement some people create what we call a revocable living trust and here's how that works so assets titled in the name of your revocable living trust when you die they don't get frozen and they it and third parties don't require court orders to release those assets things in a trust don't they they don't get involved in that so your trust in a sense will replace your will and and and so your trust then says who's going to handle your trust when you die called the trustee as opposed to the executor of your will your trust will dictate who gets your assets those people are called beneficiaries of your trust as opposed to heirs and a will and a real important step is you create your trust and then that important step is you know while you're alive and while you're setting this up you're retitling those assets that were in your name that would have to go through probate when you die you retitle them into the name of your trust that's an important step sometimes it gets overlooked but the trust instrument governs the handling and distribution of assets that are titled in the name of your trust when you die so when you die typically the trust becomes irrevocable and you will have named a trustee probably a family member or maybe Co trustees maybe multiple family members to handle your trust when you die you state who's entitled to receive the trust assets when you die they're called principle beneficiaries and then the trustee merely just disperses the trust assets from the trust to those beneficiaries or typically family members and no lawyer and court involvement is necessary to get that done all right so now let's go into some of the kind of gradual trends that we're seeing for this year for this decade what happened last decade as we move forward so that the trend that I see is that states are attempting to create legislations so that fewer assets get frozen when you die and require all of this court involvement to get that asset transferred to the people that you would want it transfer to so let me give you a few examples so forever longer than I've been around people who have had life insurance policies they named beneficiaries and so when a person died owning a life insurance policy the family didn't need lawyers and courts to get involved to get the life insurance money they would just need a death certificate to the to submit to the life insurance company and then the life insurance company would those beneficiaries directly same thing with IRAs although there's some tax consequences their IRAs have beneficiaries annuities have beneficiaries so those you know for many many decades have been around those assets avoid probate and in recent years or recent decades states have enacted new legislation for other types of accounts things like transfer on death TOD things like payable on death p OD i know in louisiana our banking statutes permit payable on death bank accounts some investment accounts in some states they permit you to title those joint tenants with rights of survivorship you see a lot of married couples title assets that way and when the state commits it then when one of those joint tenants dies ownership automatically goes to the survivor and then you see some bank accounts where and this is kind of the informal way people do it you see mom or dad taking their child to the bank and adding their child as having signature authority on mom or dad or mom and dad's bank account and in many cases when mom or dad or mom and dad pass away that child who has signature signature Authority has access to the bank account the bank account doesn't get frozen go inquire your banks with your banks as to whether that works don't rely on your lawyer's advice that's a question for the bank here in in Louisiana where we are there's a mechanism available for people to leave their vehicles in their name and if their estate planning paperwork is set up right then when they die the depart office of Motor Vehicles doesn't need court orders to retitle those vehicles so that's another avoid probate mechanism with the vehicles and then here also here in Louisiana and started maybe a decade ago and and gets revised every couple of years we have our small succession affidavit procedure where if somebody lived in Louisiana when they and they had no will and they had less than 125,000 dollars in assets then the survivors can can complete this affidavit procedure and get get access to assets without having to go through the formal court proceeding so we're starting to see some things and some trends change in the area of trying to get families to have access to assets quicker and without court and government involvement here for example in Louisiana this Tod which you see in other states transfer on death it's not recognized here in Louisiana so if you have an investment account and you live in Louisiana and you own some shares of stock or investments in your name I'm not talking about your IRA that has beneficiaries but non IRA accounts then that's gonna have to go through probate if it's in your name when you die and here in Louisiana you can't title real estate or really any asset joint tenants with rights of survivorship it's not a form of ownership that's recognized here in Louisiana so if you own a home or own any real estate in your name when you die it's got to go through the probate or succession procedure even if you're married when the first spouse dies and that married couple bought a home together the surviving spouse is not going to be able to sell the home until that surviving spouse completes the probate of the first spouse to die so we still have some obstacles to cross to make it easy to avoid probate in Louisiana so so still that even with you know with all those you know gradual trends and those those kind of attempts at some probate avoidance mechanism you're likely to need a revocable living trust if your goal is to enable your survivors to avoid probate because there's likely some assets that you own that still would require a probate if they're in your name and even if you have assets that you know will avoid probate when you die even without you may still need a trust if you're leaving assets to miners who can't inherit as a miner if you're leaving assets to a special need heir who would get kicked off of government assistance if they were to inherit from you you'll want to have a trust in place to hold those assets correctly after you pass away or you'll need a trust if you just don't want to dump a chunk of money into one of your survivors laps maybe if maybe you feel like it would be better if it would be managed and doled out to that survivor of yours over a period of years to keep them from blowing it or you know handling it inappropriately all right so where we're at so far is 2020 and beyond if you own assets in your name there's likely to be a probate when you die which means your survivors got to go through court and attorney involvement many people set up their revocable living trust they title assets in their trust when they die they name the trustee who will handle things when they die and they name the beneficiaries of their trust who will receive assets when they die and when they die that trustee will be able to immediately immediately disperse the assets out of the trust to those beneficiaries without court and attorney involvement because things in a trust don't get frozen when you die okay so the next thing I want to go over is the the tax aspect to all of this and really the trend here in 2020 is for the next five years most families are going to avoid estate tax they don't even have to have the how do we avoid estate tax discussion but in 2026 and beyond our estate tax exclusion amount gets cut in half and so some families will be affected by the estate tax in the deal is many people who are getting their legal affairs in order this year in 2020 many of them are not going to die until after 2025 so of course the law the tax law in effect when they die is what applies in in this scenario so 2020 the estate tax exclusion or exempt amount is eleven point five eight million but in 2026 that that 10-year law sunsets and it comes back to five million dollars adjusted for inflation it'll probably be about six million dollars or so in 2026 so one of the questions is particularly for married couples is and and we have to answer this question while we're setting things up now so the question is you know when the first spouse dies does does that spouses share of the assets need to be kept out of or excluded from or not be lumped into the surviving spouses estate or do we want the assets of the you know and if the the first question was we don't want the surviving spouse perhaps to have an unusually large estate because the assets of the first spouse today got dumped into the estate of the surviving spouse maybe triggering that as that surviving spouse is a state to be more than the five million or the 11 million triggering 40% estate tax when the surviving spouse dies so we look at that or do we want the assets of the first spouse to die to be included in the surviving spouses estate in order to get what's called the double step-up in basis for capital gains tax purposes so I'm not going to get too much into all the intricate intricacies of that tax discussion but be aware that there are some some tax decisions that impact your family that need to be addressed when you're setting things up because it may be too late to fix it after the first spouse dies for married couples so just realize there's some there's some tax questions there all right so here's a couple of other things that I see that I think are important what I've found over the years doing this for some 28 29 years now that revocable living trust program that people put together when they do put it together and set everything up correctly it really forces you to inventory what you own kind of pull it all together go get the records because when you set up your revocable living trust plan correctly you're gonna be retitling certain assets that you own and so it's gonna force you to you know to go double-check get the records on what you own and have a good inventory of that and since it forces you to do that well that may be an easier scenario than just not inventory your assets having a will to dictate where whatever your own goes when you die and then when you die then your family is forced to inventory what you own and go seek out those records and it may be easier for you to do it than for them to do it so me personally my my wife Amy and I we've been married for 64 years between the two of us that's that's 32 each I thought you might like that one but and we have we have five kids who are all now young adults and just meet personally if something were to happen to me I don't want my wife to have to go hire other lawyers I'm a lawyer I don't want her to have to go hire other lawyers and and you know spend the effort and the resources that we built in an attempt for her to get access to be able to sell our house if that's necessary or access our investments and I certainly don't want our five kids having to go through that if something happens to me and my wife so that's that's one of the reasons that we you know set up our you know revocable living trust is we just you know I've specifically don't want my survivors to have to go through that so that's just that's just me personally excuse me so states are gradually trying to implement legislation that enables some assets to avoid this government supervision and attorney involvement but in no means has what they've done enabled most people to completely avoid the probate and since in general you know dealing with courts seems to be getting more complicated our government seems to be more complicated less efficient attorneys fees never go down from year to year you know attorneys and I'm an attorney and I'm just I've seen just you know this gradual kind of steep incline of the cost of probate over the years and so how most people feel is if you can do some things now to make it easier on your survivors then most people feel like you know they'd like to do that and kind of in my instance that's it'll be the the one final you know parental or fatherly gift that I provide for my kids to make it easier for them to get things settled one day I hope many decades from now so that should give you an idea on what's happening in this area of revocable living trusts in 2020 and beyond I'm gonna keep you informed make sure you hit the subscribe button in the notification bell so you don't miss anything make sure you give it a thumbs up if you found this was helpful and then share it there's a share arrow on your screen share it with other friends colleagues relatives of yours who may have an interest in wanting to try to make their estate settlement simpler for their families and their survivors I'm Paul Riley have a happy new year we'll see you next time

Show more