Consumer Caution and Homeownership Counseling Notice Form

What is the Consumer Caution and Homeownership Counseling Notice

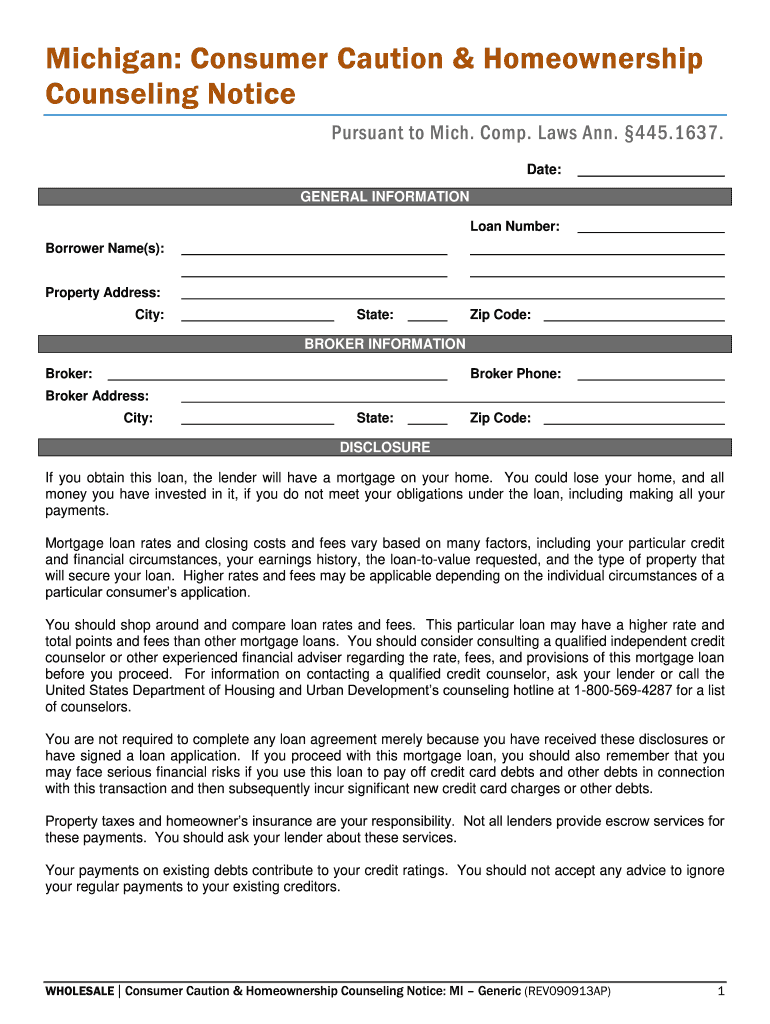

The Consumer Caution and Homeownership Counseling Notice is an essential document designed to inform potential homeowners about the risks and responsibilities associated with homeownership. This notice aims to provide consumers with necessary insights into the home buying process, ensuring they understand their rights and obligations. It emphasizes the importance of seeking professional counseling to navigate the complexities of homeownership, especially for first-time buyers or those with limited experience in real estate transactions.

Key elements of the Consumer Caution and Homeownership Counseling Notice

This notice includes several critical components that consumers should be aware of:

- Disclosure of Risks: It outlines the potential risks involved in purchasing a home, including financial obligations and market fluctuations.

- Encouragement for Counseling: The notice encourages consumers to seek homeownership counseling services, which can provide valuable guidance and support.

- Understanding Financial Commitments: It emphasizes the importance of understanding mortgage terms, interest rates, and the total cost of homeownership.

- Consumer Rights: The notice informs consumers of their rights under federal and state laws, ensuring they are aware of protections available to them.

Steps to complete the Consumer Caution and Homeownership Counseling Notice

Completing the Consumer Caution and Homeownership Counseling Notice involves several straightforward steps:

- Obtain the Form: Access the notice from a reliable source, such as a lender or housing authority.

- Read Carefully: Review the entire document to understand its contents and implications fully.

- Provide Required Information: Fill in any necessary personal details, including your name and contact information.

- Sign the Document: Ensure you sign the notice to acknowledge your understanding of the information presented.

- Submit the Notice: Return the completed notice to the appropriate party, typically your lender or housing counselor.

Legal use of the Consumer Caution and Homeownership Counseling Notice

The Consumer Caution and Homeownership Counseling Notice serves a legal purpose in the home buying process. It is often required by lenders to ensure that consumers are adequately informed before proceeding with a mortgage application. The notice helps protect consumers by documenting their acknowledgment of the risks associated with homeownership. Additionally, it may be referenced in legal proceedings to demonstrate that the consumer was informed about their responsibilities and rights.

How to use the Consumer Caution and Homeownership Counseling Notice

Using the Consumer Caution and Homeownership Counseling Notice effectively involves understanding its role in the home buying process. Consumers should present this notice to their lenders during the mortgage application process. It acts as a formal acknowledgment that they have received and understood the information provided. Furthermore, consumers can use the notice as a reference point when discussing their homeownership plans with financial advisors or counselors, ensuring they are making informed decisions.

How to obtain the Consumer Caution and Homeownership Counseling Notice

Obtaining the Consumer Caution and Homeownership Counseling Notice is a straightforward process. Consumers can typically request this notice from their mortgage lender or housing counseling agency. Many organizations provide the notice as part of their homebuyer education programs. Additionally, it may be available online through official housing authority websites or community resources focused on homeownership education.

Quick guide on how to complete consumer caution and homeownership counseling notice

Complete Consumer Caution And Homeownership Counseling Notice effortlessly on any device

Online document administration has gained popularity among organizations and individuals. It offers an ideal eco-friendly substitute for conventional printed and signed documents, as you can access the correct form and securely store it online. airSlate SignNow provides all the tools you need to create, modify, and electronically sign your documents quickly without delays. Manage Consumer Caution And Homeownership Counseling Notice on any platform with airSlate SignNow's Android or iOS applications and streamline any document-related procedure today.

How to modify and electronically sign Consumer Caution And Homeownership Counseling Notice with ease

- Locate Consumer Caution And Homeownership Counseling Notice and click Get Form to begin.

- Utilize the tools we provide to fill out your form.

- Emphasize important sections of your documents or conceal sensitive information with tools that airSlate SignNow offers for that purpose.

- Create your signature using the Sign tool, which takes seconds and holds the same legal validity as a conventional ink signature.

- Review the details and click the Done button to save your modifications.

- Choose your preferred method to send your form, via email, SMS, or invite link, or download it to your computer.

Eliminate concerns about lost or misplaced documents, frustrating form searches, or errors that necessitate printing new document copies. airSlate SignNow addresses your document management needs in just a few clicks from any device you prefer. Edit and eSign Consumer Caution And Homeownership Counseling Notice to ensure excellent communication at every stage of your form preparation process with airSlate SignNow.

Create this form in 5 minutes or less

Create this form in 5 minutes!

How to create an eSignature for the consumer caution and homeownership counseling notice

How to create an electronic signature for a PDF online

How to create an electronic signature for a PDF in Google Chrome

How to create an e-signature for signing PDFs in Gmail

How to create an e-signature right from your smartphone

How to create an e-signature for a PDF on iOS

How to create an e-signature for a PDF on Android

People also ask

-

What is a homeownership counseling notice?

A homeownership counseling notice is a crucial document that informs borrowers about the requirement to seek counseling before purchasing a home. It ensures that potential homeowners understand their financial obligations and the resources available to them for making informed decisions. This notice is an essential part of the home buying process.

-

How does airSlate SignNow help with sending a homeownership counseling notice?

airSlate SignNow simplifies the process of sending a homeownership counseling notice with its user-friendly eSignature platform. You can easily create, send, and track documents to ensure that all parties receive the notice promptly. This efficient workflow helps streamline your document management process.

-

What are the benefits of using airSlate SignNow for homeownership counseling notices?

Using airSlate SignNow for homeownership counseling notices offers several benefits, including reduced turnaround time and increased security for sensitive documents. You can also save on printing and mailing costs, making it a cost-effective solution for sending important notices. Additionally, the electronic signature feature enhances convenience for all parties involved.

-

Can I integrate airSlate SignNow with other tools for homeownership counseling notices?

Yes, airSlate SignNow offers seamless integrations with a variety of tools to enhance your document management process. Whether you use CRM software or cloud storage solutions, you can integrate them with airSlate SignNow to streamline the process of sending a homeownership counseling notice. This allows for better organization and efficiency.

-

Is there a cost associated with sending a homeownership counseling notice through airSlate SignNow?

AirSlate SignNow offers competitive pricing plans that allow you to send a homeownership counseling notice efficiently without breaking the bank. By choosing an appropriate plan based on your needs, you can enjoy unlimited document sending capabilities as well as access to other features. Investing in this solution saves you time and money in the long run.

-

What features does airSlate SignNow offer for managing homeownership counseling notices?

AirSlate SignNow offers various features for managing homeownership counseling notices, including customizable templates, tracking, and real-time notifications. These features ensure that your documents are always up-to-date and easily accessible. Additionally, the platform allows you to request signatures with ease, making the process seamless for all parties involved.

-

How secure is airSlate SignNow when handling homeownership counseling notices?

AirSlate SignNow prioritizes security and uses advanced encryption protocols to protect your documents, including homeownership counseling notices. This ensures that sensitive information remains confidential throughout the signing process. The platform also complies with regulatory standards, giving you peace of mind when handling important documents.

Get more for Consumer Caution And Homeownership Counseling Notice

Find out other Consumer Caution And Homeownership Counseling Notice

- Can I eSignature West Virginia Lawers Cease And Desist Letter

- eSignature Alabama Plumbing Confidentiality Agreement Later

- How Can I eSignature Wyoming Lawers Quitclaim Deed

- eSignature California Plumbing Profit And Loss Statement Easy

- How To eSignature California Plumbing Business Letter Template

- eSignature Kansas Plumbing Lease Agreement Template Myself

- eSignature Louisiana Plumbing Rental Application Secure

- eSignature Maine Plumbing Business Plan Template Simple

- Can I eSignature Massachusetts Plumbing Business Plan Template

- eSignature Mississippi Plumbing Emergency Contact Form Later

- eSignature Plumbing Form Nebraska Free

- How Do I eSignature Alaska Real Estate Last Will And Testament

- Can I eSignature Alaska Real Estate Rental Lease Agreement

- eSignature New Jersey Plumbing Business Plan Template Fast

- Can I eSignature California Real Estate Contract

- eSignature Oklahoma Plumbing Rental Application Secure

- How Can I eSignature Connecticut Real Estate Quitclaim Deed

- eSignature Pennsylvania Plumbing Business Plan Template Safe

- eSignature Florida Real Estate Quitclaim Deed Online

- eSignature Arizona Sports Moving Checklist Now