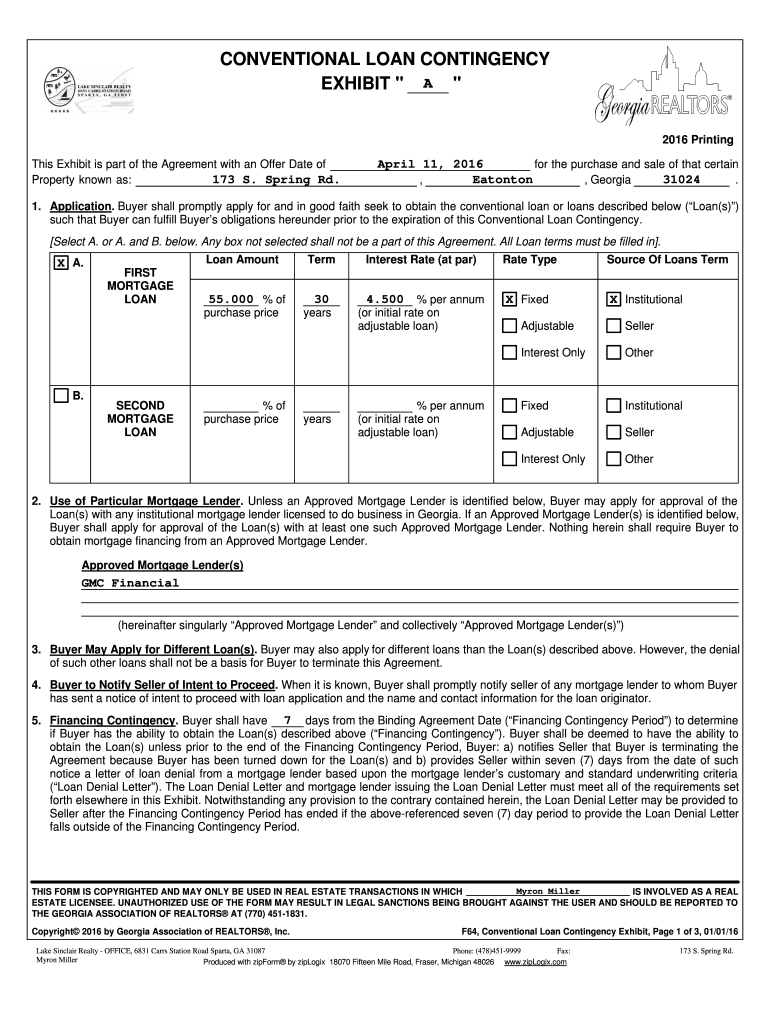

Conventional Loan Contingency Exhibit Form

What is the FHA Loan Contingency Exhibit

The FHA loan contingency exhibit is a critical document in real estate transactions involving Federal Housing Administration (FHA) loans. It outlines specific conditions that must be met for the sale to proceed, ensuring that both buyers and sellers are protected during the process. This exhibit typically includes stipulations regarding the buyer's ability to secure financing, inspections, and any necessary repairs that must be completed before closing. Understanding this exhibit is essential for both parties to ensure compliance with FHA guidelines and to facilitate a smooth transaction.

How to Use the FHA Loan Contingency Exhibit

Using the FHA loan contingency exhibit involves several steps to ensure that all necessary conditions are clearly defined and agreed upon by both parties. Initially, the buyer should fill out the exhibit, specifying the terms related to financing and any contingencies that may affect the sale. It is important for the seller to review these terms carefully, as they will dictate the timeline and responsibilities for both parties. Once completed, both the buyer and seller should sign the document, making it a legally binding part of the purchase agreement.

Key Elements of the FHA Loan Contingency Exhibit

Several key elements should be included in the FHA loan contingency exhibit to ensure clarity and legal validity. These elements typically consist of:

- Financing Terms: Details about the loan amount, interest rate, and type of FHA loan.

- Inspection Requirements: Conditions for property inspections and any necessary repairs.

- Closing Timeline: Deadlines for securing financing and closing the sale.

- Contingency Clauses: Specific conditions under which the buyer can withdraw from the agreement without penalty.

Including these elements helps both parties understand their obligations and ensures compliance with FHA regulations.

Steps to Complete the FHA Loan Contingency Exhibit

Completing the FHA loan contingency exhibit involves a systematic approach to ensure all necessary information is accurately captured. Follow these steps:

- Obtain the Exhibit: Access the FHA loan contingency exhibit form through a reliable source or real estate professional.

- Fill in Buyer Information: Provide the buyer's details, including name, contact information, and loan specifics.

- Specify Contingencies: Clearly outline any conditions that must be met for the sale to proceed.

- Review with Seller: Discuss the completed exhibit with the seller to ensure mutual understanding and agreement.

- Sign the Document: Both parties should sign the exhibit to make it legally binding.

By following these steps, both buyers and sellers can ensure that the FHA loan contingency exhibit is completed correctly and efficiently.

Legal Use of the FHA Loan Contingency Exhibit

The FHA loan contingency exhibit is legally binding when filled out and signed correctly. To ensure its legal use, both parties must comply with relevant laws and regulations governing real estate transactions. This includes adhering to the guidelines set forth by the FHA, as well as any state-specific laws that may apply. It is advisable to consult with a real estate attorney or professional to confirm that the exhibit meets all legal requirements and adequately protects the interests of both parties.

Quick guide on how to complete conventional loan contingency exhibit

Effortlessly Prepare Conventional Loan Contingency Exhibit on Any Device

Managing documents online has become increasingly favored by businesses and individuals alike. It serves as an ideal eco-friendly alternative to conventional printed and signed documents, allowing you to access the appropriate form and securely keep it online. airSlate SignNow equips you with all the tools necessary to create, modify, and eSign your documents quickly without delays. Handle Conventional Loan Contingency Exhibit on any platform using airSlate SignNow's Android or iOS applications and enhance any document-centric workflow today.

The Easiest Way to Edit and eSign Conventional Loan Contingency Exhibit with Minimal Effort

- Find Conventional Loan Contingency Exhibit and click on Get Form to begin.

- Utilize the tools we provide to complete your form.

- Emphasize signNow sections of the documents or obscure sensitive information using tools specifically designed by airSlate SignNow for that purpose.

- Create your signature with the Sign tool, which takes mere seconds and carries the same legal validity as a traditional wet ink signature.

- Review the information and click on the Done button to save your updates.

- Select your preferred method to send your form, whether through email, SMS, or invitation link, or download it to your computer.

Say goodbye to lost or misplaced documents, tedious form searches, or errors that necessitate printing new copies. airSlate SignNow addresses all your document management needs in just a few clicks from your device of choice. Modify and eSign Conventional Loan Contingency Exhibit to ensure exceptional communication at any point in your form preparation journey with airSlate SignNow.

Create this form in 5 minutes or less

Create this form in 5 minutes!

How to create an eSignature for the conventional loan contingency exhibit

How to create an electronic signature for a PDF online

How to create an electronic signature for a PDF in Google Chrome

How to create an e-signature for signing PDFs in Gmail

How to create an e-signature right from your smartphone

How to create an e-signature for a PDF on iOS

How to create an e-signature for a PDF on Android

People also ask

-

What is an FHA loan contingency exhibit?

An FHA loan contingency exhibit is a document that outlines the conditions under which a buyer can cancel a real estate purchase agreement if they are unable to secure an FHA loan. This exhibit protects both the buyer and the seller in the transaction, ensuring that all parties are aware of the financing terms. By incorporating the FHA loan contingency exhibit, buyers can safeguard their interests while navigating the home purchasing process.

-

How can airSlate SignNow help with the FHA loan contingency exhibit?

airSlate SignNow offers a seamless platform for creating, sending, and eSigning the FHA loan contingency exhibit and other important documents. With an easy-to-use interface, you can quickly customize your exhibit based on your specific requirements. Our solution not only streamlines the signing process but also enhances document security for all parties involved.

-

What are the pricing options for airSlate SignNow for managing FHA loan documents?

airSlate SignNow provides affordable pricing plans that cater to diverse business needs, including those dealing with FHA loan documents. You can choose from various subscription models based on the number of users and features required. The cost-effectiveness of our solution ensures that managing the FHA loan contingency exhibit and other documents is accessible for all real estate professionals.

-

What features does airSlate SignNow offer for eSigning the FHA loan contingency exhibit?

airSlate SignNow includes robust features for eSigning the FHA loan contingency exhibit, such as multi-party signing, document templates, and a dashboard for tracking document status. Additionally, our platform supports real-time collaboration, allowing parties to discuss and finalize details before signing. These features simplify the signing process and enhance overall efficiency.

-

Are there any benefits of using airSlate SignNow for FHA loan-related documents?

Using airSlate SignNow for FHA loan-related documents, including the FHA loan contingency exhibit, provides numerous benefits like increased speed, reduced paperwork, and enhanced convenience. Our platform allows you to access and manage all documentation online, making it easier to stay organized. Furthermore, the ability to track and audit document activity helps in maintaining compliance throughout the loan process.

-

Can airSlate SignNow integrate with other tools for FHA loan management?

Yes, airSlate SignNow offers robust integrations with popular real estate and finance tools, providing seamless management of FHA loans and associated documents. By integrating with your existing systems, you can enhance workflow efficiency and data sync across platforms. This means you can easily manage your FHA loan contingency exhibit alongside other essential workflows.

-

How does airSlate SignNow ensure the security of the FHA loan contingency exhibit?

airSlate SignNow prioritizes the security of all documents, including the FHA loan contingency exhibit, by employing advanced encryption and authentication measures. Our platform ensures that sensitive information remains protected during transmission and storage. Users can also benefit from audit trails that provide detailed logs of document access and modifications, enhancing trust in the signing process.

Get more for Conventional Loan Contingency Exhibit

- Tax year 1040 form

- Request for quote 19255 rfq 19255 a quotation due by bid due time vendor info 1007 120000 pm vendor 99999 form

- Guidelines and instructions tidewater community college web tcc form

- Reinstatement application residential builder license form

- Careplus class roster gwrra gwrra form

- Employee warning record glendale heights illinois web01 glendaleheights form

- Application for relicensure licensing and regulatory affairs dleg state mi form

- Available services form

Find out other Conventional Loan Contingency Exhibit

- How To Integrate Sign in Banking

- How To Use Sign in Banking

- Help Me With Use Sign in Banking

- Can I Use Sign in Banking

- How Do I Install Sign in Banking

- How To Add Sign in Banking

- How Do I Add Sign in Banking

- How Can I Add Sign in Banking

- Can I Add Sign in Banking

- Help Me With Set Up Sign in Government

- How To Integrate eSign in Banking

- How To Use eSign in Banking

- How To Install eSign in Banking

- How To Add eSign in Banking

- How To Set Up eSign in Banking

- How To Save eSign in Banking

- How To Implement eSign in Banking

- How To Set Up eSign in Construction

- How To Integrate eSign in Doctors

- How To Use eSign in Doctors