Installment Agreement to Pay Accident Damages ErnestoRomero Ernestoromero 2002-2026

Understanding the Agreement to Pay for Car Damages

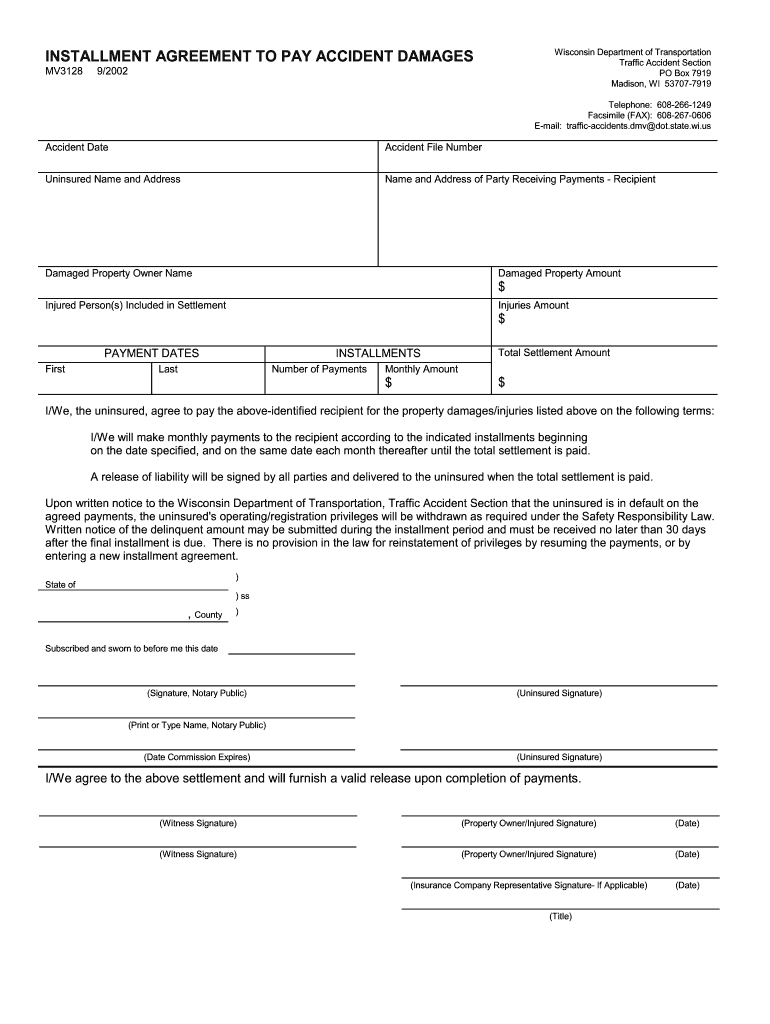

An agreement to pay for car damages is a legal document that outlines the terms under which one party agrees to compensate another for damages incurred to a vehicle. This agreement typically includes details such as the amount to be paid, payment schedule, and any conditions that must be met by either party. It serves to protect both the payer and the recipient by clearly defining responsibilities and expectations, thus reducing the likelihood of disputes.

Steps to Complete the Agreement to Pay for Car Damages

Completing an agreement to pay for car damages involves several key steps:

- Gather necessary information about the vehicle, including make, model, and VIN.

- Collect personal details of both parties, such as names, addresses, and contact information.

- Clearly state the amount of damages and how the payment will be made, whether in full or installments.

- Include any relevant dates, such as when the payment is due.

- Ensure both parties sign and date the document to make it legally binding.

Key Elements of the Agreement to Pay for Car Damages

Several essential components should be included in an agreement to pay for car damages:

- Identification of Parties: Clearly identify the parties involved, including their roles (e.g., payer and recipient).

- Description of Damages: Provide a detailed description of the damages being compensated.

- Payment Terms: Outline the total amount, payment schedule, and acceptable payment methods.

- Signatures: Both parties must sign the agreement to validate it legally.

- Date: Include the date the agreement is signed to establish a timeline.

Legal Use of the Agreement to Pay for Car Damages

For an agreement to pay for car damages to be legally enforceable, it must comply with state laws governing contracts. This includes ensuring that both parties have the legal capacity to enter into the agreement and that the terms are clear and unambiguous. It is advisable to consult with a legal professional to ensure the document meets all necessary legal requirements.

How to Use the Agreement to Pay for Car Damages

Using the agreement to pay for car damages involves several practical considerations:

- Ensure that both parties understand the terms before signing.

- Keep a copy of the signed agreement for personal records.

- Follow the agreed-upon payment schedule to maintain good faith and avoid potential legal issues.

- Communicate openly if any issues arise regarding payments or the condition of the vehicle.

Obtaining the Agreement to Pay for Car Damages

The agreement to pay for car damages can be obtained through various sources. Many legal websites offer templates that can be customized to fit specific situations. Alternatively, individuals may choose to draft their own agreement using basic legal principles. It is recommended to review any template or draft with a legal professional to ensure it is comprehensive and compliant with applicable laws.

Quick guide on how to complete installment agreement to pay accident damages ernestoromero ernestoromero

Simplify your life by finalizing Installment Agreement To Settling Accident Damages ErnestoRomero Ernestoromero form with airSlate SignNow

Whether you need to title a new vehicle, apply for a driver’s license, transfer ownership, or accomplish any other task related to automobiles, managing such RMV documents as Installment Agreement To Pay Accident Damages ErnestoRomero Ernestoromero is an essential hassle.

There are various methods to obtain them: via mail, at the RMV service center, or by downloading them online through your local RMV website and printing them. Each of these methods can be time-consuming. If you’re looking for a quicker way to fill them out and validate them with a legally-recognized signature, airSlate SignNow is your optimal choice.

How to fill out Installment Agreement To Pay Accident Damages ErnestoRomero Ernestoromero effortlessly

- Click on Show details to view a brief overview of the document you’re interested in.

- Select Get document to initiate and open the form.

- Follow the green label indicating the required fields if applicable.

- Utilize the top toolbar and make use of our professional feature set to modify, annotate, and enhance your form's appearance.

- Insert text, your initials, shapes, images, and other elements.

- Click Sign in in the same toolbar to create a legally-recognized signature.

- Review the form text to ensure it’s devoid of mistakes and inconsistencies.

- Press Done to complete the form submission.

Utilizing our service to finalize your Installment Agreement To Pay Accident Damages ErnestoRomero Ernestoromero and other relevant documents will signNowly save you time and hassle. Enhance your RMV document processing from day one!

Create this form in 5 minutes or less

FAQs

-

I need to pay an $800 annual LLC tax for my LLC that formed a month ago, so I am looking to apply for an extension. It's a solely owned LLC, so I need to fill out a Form 7004. How do I fill this form out?

ExpressExtension is an IRS-authorized e-file provider for all types of business entities, including C-Corps (Form 1120), S-Corps (Form 1120S), Multi-Member LLC, Partnerships (Form 1065). Trusts, and Estates.File Tax Extension Form 7004 InstructionsStep 1- Begin by creating your free account with ExpressExtensionStep 2- Enter the basic business details including: Business name, EIN, Address, and Primary Contact.Step 3- Select the business entity type and choose the form you would like to file an extension for.Step 4- Select the tax year and select the option if your organization is a Holding CompanyStep 5- Enter and make a payment on the total estimated tax owed to the IRSStep 6- Carefully review your form for errorsStep 7- Pay and transmit your form to the IRSClick here to e-file before the deadline

-

The company I work for is taking taxes out of my paycheck but has not asked me to complete any paperwork or fill out any forms since day one. How are they paying taxes without my SSN?

WHOA! You may have a BIG problem. When you started, are you certain you did not fill in a W-4 form? Are you certain that your employer doesn’t have your SS#? If that’s the case, I would be alarmed. Do you have paycheck stubs showing how they calculated your withholding? ( BTW you are entitled to those under the law, and if you are not receiving them, I would demand them….)If your employer is just giving you random checks with no calculation of your wages and withholdings, you have a rogue employer. They probably aren’t payin in what they purport to withhold from you.

-

As one of the cofounders of a multi-member LLC taxed as a partnership, how do I pay myself for work I am doing as a contractor for the company? What forms do I need to fill out?

First, the LLC operates as tax partnership (“TP”) as the default tax status if no election has been made as noted in Treasury Regulation Section 301.7701-3(b)(i). For legal purposes, we have a LLC. For tax purposes we have a tax partnership. Since we are discussing a tax issue here, we will discuss the issue from the perspective of a TP.A partner cannot under any circumstances be an employee of the TP as Revenue Ruling 69-184 dictated such. And, the 2016 preamble to Temporary Treasury Regulation Section 301.7701-2T notes the Treasury still supports this revenue ruling.Though a partner can engage in a transaction with the TP in a non partner capacity (Section 707a(a)).A partner receiving a 707(a) payment from the partnership receives the payment as any stranger receives a payment from the TP for services rendered. This partner gets treated for this transaction as if he/she were not a member of the TP (Treasury Regulation Section 1.707-1(a).As an example, a partner owns and operates a law firm specializing in contract law. The TP requires advice on terms and creation for new contracts the TP uses in its business with clients. This partner provides a bid for this unique job and the TP accepts it. Here, the partner bills the TP as it would any other client, and the partner reports the income from the TP client job as he/she would for any other client. The TP records the job as an expense and pays the partner as it would any other vendor. Here, I am assuming the law contract job represents an expense versus a capital item. Of course, the partner may have a law corporation though the same principle applies.Further, a TP can make fixed payments to a partner for services or capital — called guaranteed payments as noted in subsection (c).A 707(c) guaranteed payment shows up in the membership agreement drawn up by the business attorney. This payment provides a service partner with a guaranteed payment regardless of the TP’s income for the year as noted in Treasury Regulation Section 1.707-1(c).As an example, the TP operates an exclusive restaurant. Several partners contribute capital for the venture. The TP’s key service partner is the chef for the restaurant. And, the whole restaurant concept centers on this chef’s experience and creativity. The TP’s operating agreement provides the chef receives a certain % profit interest but as a minimum receives yearly a fixed $X guaranteed payment regardless of TP’s income level. In the first year of operations the TP has low profits as expected. The chef receives the guaranteed $X payment as provided in the membership agreement.The TP allocates the guaranteed payment to the capital interest partners on their TP k-1s as business expense. And, the TP includes the full $X guaranteed payment as income on the chef’s K-1. Here, the membership agreement demonstrates the chef only shares in profits not losses. So, the TP only allocates the guaranteed expense to those partners responsible for making up losses (the capital partners) as noted in Treasury Regulation Section 707-1(c) Example 3. The chef gets no allocation for the guaranteed expense as he/she does not participate in losses.If we change the situation slightly, we may change the tax results. If the membership agreement says the chef shares in losses, we then allocate a portion of the guaranteed expense back to the chef following the above treasury regulation.As a final note, a TP return requires knowledge of primary tax law if the TP desires filing a completed an accurate partnership tax return.I have completed the above tax analysis based on primary partnership tax law. If the situation changes in any manner, the tax outcome may change considerably. www.rst.tax

-

How much will a doctor with a physical disability and annual net income of around Rs. 2.8 lakhs pay in income tax? Which ITR form is to be filled out?

For disability a deduction of ₹75,000/- is available u/s 80U.Rebate u/s87AFor AY 17–18, rebate was ₹5,000/- or income tax which ever is lower for person with income less than ₹5,00,000/-For AY 18–19, rebate is ₹2,500/- or income tax whichever is lower for person with income less than 3,50,000/-So, for an income of 2.8 lakhs, taxable income after deduction u/s 80U will remain ₹2,05,000/- which is below the slab rate and hence will not be taxable for any of the above said AY.For ITR,If doctor is practicing himself i.e. He has a professional income than ITR 4 should be filedIf doctor is getting any salary than ITR 1 should be filed.:)

-

If you work for yourself doing government contracts and American Express asks for you to show them a current pay stub, how would you provide that? Is there a form that has an earnings statement that you can fill out yourself?

It seems to me you should just ask American Express if they have form you can fill out. It seems odd they would want to see an earnings statement, but if you need to show some sort of proof of income, typically in the absence of a pay stub, your most recently-filed tax return should suffice.I'd really ask them first before automatically sending them your tax returns though.

-

Why should it be so complicated just figuring out how much tax to pay? (record keeping, software, filling out forms . . . many times cost much more than the amount of taxes due) The cost of compliance makes the U.S. uncompetitive and costs jobs and lowers our standard of living.

Taxes can be viewed as having 4 uses (or purposes) in our (and most) governments:Revenue generation (to pay for public services).Fiscal policy control (e.g., If the government wishes to reduce the money supply in order to reduce the risk of inflation, they can raise interest rates, sell fewer bonds, burn money, or raise taxes. In the last case, this represents excess tax revenue over the actual spending needs of the government).Wealth re-distribution. One argument for this is that the earnings of a country can be perceived as belonging to all of its citizens since the we all have a stake in the resources of the country (natural resources, and intangibles such as culture, good citizenship, civic duties). Without some tax policy complexity, the free market alone does not re-distribute wealth according to this "shared" resources concept. However, this steps into the boundary of Purpose # 4...A way to implement Social Policy (and similar government mandated policies, such as environmental policy, health policy, savings and debt policy, etc.). As Government spending can be use to implement policies (e.g., spending money on public health care, environmental cleanup, education, etc.), it is equivalent to provide tax breaks (income deductions or tax credits) for the private sector to act in certain ways -- e.g., spend money on R&D, pay for their own education or health care, avoid spending money on polluting cars by having a higher sales tax on these cars or offering a credit for trade-ins [ref: Cash for Clunkers]).Uses # 1 & 2 are rather straight-forward, and do not require a complex tax code to implement. Flat income and/or consumption (sales) taxes can easily be manipulated up or down overall for these top 2 uses. Furthermore, there is clarity when these uses are invoked. For spending, we publish a budget. For fiscal policy manipulation, the official economic agency (The Fed) publishes their outlook and agenda.Use # 3 is controversial because there is no Constitutional definition for the appropriate level of wealth re-distribution, and the very concept of wealth re-distribution is considered by some to be inappropriate and unconstitutional. Thus, the goal of wealth re-distribution is pretty much hidden in with the actions and policies of Use #4 (social policy manipulation).Use # 4, however, is where the complexity enters the Taxation system. Policy implementation through taxation (or through spending) occurs via legislation. Legislation (law making) is inherently complex and subject to gross manipulation by special interests during formation and amendments. Legislation is subject to interpretation, is prone to errors (leading to loopholes) and both unintentional or intentional (criminal / fraudulent) avoidance.The record keeping and forms referred to in the question are partially due to the basic formula for calculating taxes (i.e., percentage of income, cost of property, amount of purchase for a sales tax, ...). However, it is the complexity (and associated opportunities for exploitation) of taxation legislation for Use # 4 (Social Policy implementation) that naturally leads to complexity in the reporting requirements for the tax system.

Create this form in 5 minutes!

How to create an eSignature for the installment agreement to pay accident damages ernestoromero ernestoromero

How to make an eSignature for your Installment Agreement To Pay Accident Damages Ernestoromero Ernestoromero online

How to make an eSignature for the Installment Agreement To Pay Accident Damages Ernestoromero Ernestoromero in Google Chrome

How to make an electronic signature for signing the Installment Agreement To Pay Accident Damages Ernestoromero Ernestoromero in Gmail

How to generate an eSignature for the Installment Agreement To Pay Accident Damages Ernestoromero Ernestoromero right from your smartphone

How to make an eSignature for the Installment Agreement To Pay Accident Damages Ernestoromero Ernestoromero on iOS devices

How to create an eSignature for the Installment Agreement To Pay Accident Damages Ernestoromero Ernestoromero on Android

People also ask

-

What is an 'agreement to pay for car damages template'?

An 'agreement to pay for car damages template' is a legal document designed to outline the terms of payment for damages incurred to a vehicle. This template helps parties define responsibilities and payment obligations clearly, ensuring clarity and reducing potential disputes. Using this template simplifies and streamlines the process, making it easier to handle car damage situations.

-

How can airSlate SignNow help with the 'agreement to pay for car damages template'?

airSlate SignNow provides a user-friendly platform that allows you to easily create, customize, and eSign your 'agreement to pay for car damages template'. The intuitive interface ensures that you can quickly generate a legally binding document, facilitating faster resolution of any vehicle damage issues. This feature helps simplify the documentation process for both individuals and businesses.

-

Is the 'agreement to pay for car damages template' legally binding?

Yes, an 'agreement to pay for car damages template' created using airSlate SignNow is legally binding when properly signed by all parties involved. The platform complies with eSignature laws, ensuring that your documents hold up in legal situations. This functionality provides reassurance that your agreement will be honored.

-

What are the pricing options for using airSlate SignNow with the 'agreement to pay for car damages template'?

airSlate SignNow offers a variety of pricing plans to fit different needs, starting from a free trial for new users. With flexible subscriptions, you can choose the plan that best suits your business requirements for using the 'agreement to pay for car damages template'. Comprehensive features are included in each plan, ensuring you get the best value for your investment.

-

Can I customize the 'agreement to pay for car damages template'?

Absolutely! With airSlate SignNow, you can fully customize the 'agreement to pay for car damages template' to suit your specific needs. The platform allows you to edit text, add clauses, and include your branding elements. This flexibility ensures your agreement reflects your unique terms and requirements.

-

What features does airSlate SignNow provide for the 'agreement to pay for car damages template'?

airSlate SignNow offers features such as eSigning, document sharing, and secure storage for the 'agreement to pay for car damages template'. Additionally, you can set reminders for signing and track the document status in real-time. These features enhance efficiency and ensure a smooth signing process for all parties involved.

-

Is there any integration available with external applications for the 'agreement to pay for car damages template'?

Yes, airSlate SignNow integrates seamlessly with a variety of external applications, enhancing the functionality of your 'agreement to pay for car damages template'. You can connect it with popular tools like Google Drive, Salesforce, and Microsoft Office, facilitating easy document management and workflows. This ensures your documents are easily accessible across platforms.

Get more for Installment Agreement To Pay Accident Damages ErnestoRomero Ernestoromero

- 96 well plate template 100041450 form

- Online par q form

- Formulario 001 del rut editable excel

- Tsc sick leave online application form

- Metric pattern cutting for menswear pdf form

- Insanity fit test sheet form

- Berojgari bhatta self declaration form pdf

- Www asap towing comwp contentuploadsx asap towing of bellingham form

Find out other Installment Agreement To Pay Accident Damages ErnestoRomero Ernestoromero

- Help Me With eSign Hawaii Lawers Word

- How Can I eSign Hawaii Lawers Document

- How To eSign Hawaii Lawers PPT

- Help Me With eSign Hawaii Insurance PPT

- Help Me With eSign Idaho Insurance Presentation

- Can I eSign Indiana Insurance Form

- How To eSign Maryland Insurance PPT

- Can I eSign Arkansas Life Sciences PDF

- How Can I eSign Arkansas Life Sciences PDF

- Can I eSign Connecticut Legal Form

- How Do I eSign Connecticut Legal Form

- How Do I eSign Hawaii Life Sciences Word

- Can I eSign Hawaii Life Sciences Word

- How Do I eSign Hawaii Life Sciences Document

- How Do I eSign North Carolina Insurance Document

- How Can I eSign Hawaii Legal Word

- Help Me With eSign Hawaii Legal Document

- How To eSign Hawaii Legal Form

- Help Me With eSign Hawaii Legal Form

- Can I eSign Hawaii Legal Document