Offer to Buy Real Estate and Acceptance NAI LeGrand & Company Form

What is the Offer to Buy Real Estate and Acceptance NAI LeGrand & Company

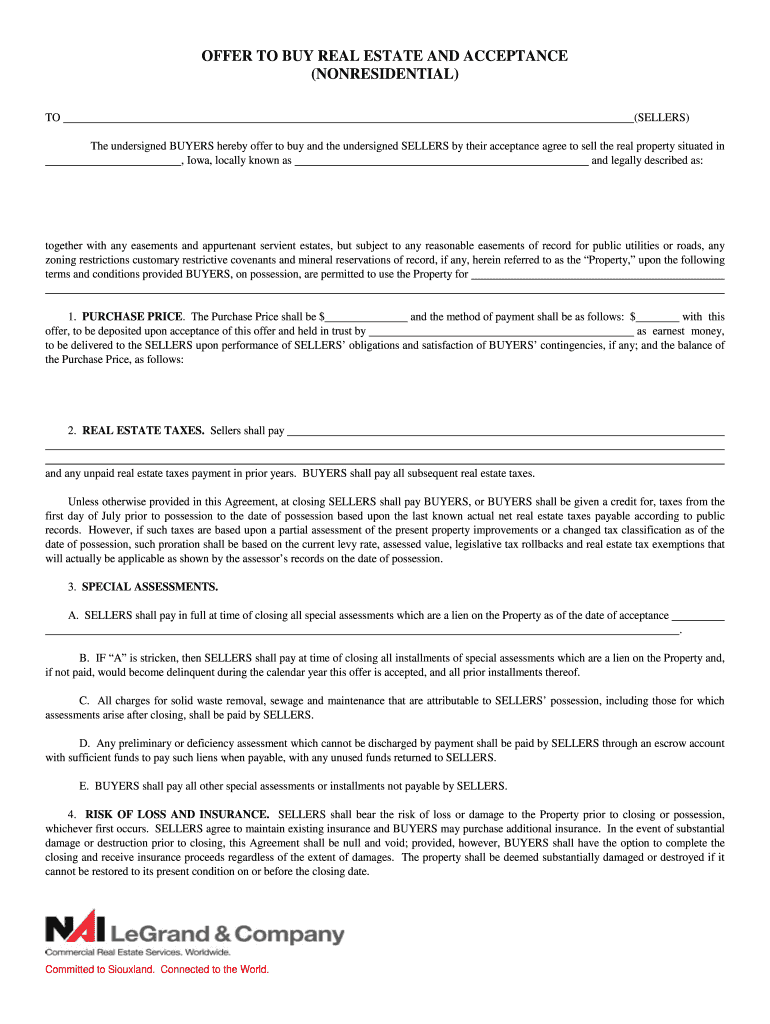

The Offer to Buy Real Estate and Acceptance NAI LeGrand & Company is a formal document used in real estate transactions. It outlines the terms under which a buyer proposes to purchase a property. This document serves as a legally binding agreement once accepted by the seller. It typically includes details such as the purchase price, financing terms, contingencies, and the closing date. Understanding this form is crucial for both buyers and sellers to ensure a smooth transaction process.

Key Elements of the Offer to Buy Real Estate and Acceptance NAI LeGrand & Company

This form includes several essential components that must be clearly defined to avoid misunderstandings. Key elements typically encompass:

- Purchase Price: The amount the buyer is willing to pay for the property.

- Financing Terms: Information on how the buyer plans to finance the purchase.

- Contingencies: Conditions that must be met for the sale to proceed, such as home inspections or financing approvals.

- Closing Date: The date when the property transfer will be finalized.

- Expiration Date: The timeframe in which the seller must respond to the offer.

Steps to Complete the Offer to Buy Real Estate and Acceptance NAI LeGrand & Company

Completing the Offer to Buy Real Estate and Acceptance involves several steps to ensure accuracy and compliance. Here are the steps to follow:

- Gather necessary information about the property and the buyer.

- Fill out the form, ensuring all sections are completed accurately.

- Review the offer with a real estate professional to confirm that all terms are clear and fair.

- Submit the completed form to the seller or their agent.

- Await the seller's response, which may include acceptance, rejection, or a counteroffer.

Legal Use of the Offer to Buy Real Estate and Acceptance NAI LeGrand & Company

This form must comply with state and federal real estate laws to be legally binding. It is essential that both parties understand their rights and obligations as outlined in the document. Proper execution of the form ensures that the agreement is enforceable in a court of law, should any disputes arise. Consulting with a legal professional can provide additional assurance that the document meets all legal requirements.

How to Obtain the Offer to Buy Real Estate and Acceptance NAI LeGrand & Company

The Offer to Buy Real Estate and Acceptance can typically be obtained through real estate professionals, such as agents or brokers associated with NAI LeGrand & Company. Additionally, many real estate websites provide downloadable templates of this form. It is important to ensure that you are using the most current version of the form to comply with any recent legal updates.

Examples of Using the Offer to Buy Real Estate and Acceptance NAI LeGrand & Company

Practical examples of using this form include:

- A buyer making an offer on a residential property after attending an open house.

- A real estate investor submitting multiple offers on different properties to secure a favorable deal.

- A seller receiving multiple offers and needing to evaluate terms before accepting one.

Quick guide on how to complete offer to buy real estate and acceptance nai legrand amp company

The ideal method to obtain and sign Offer To Buy Real Estate And Acceptance NAI LeGrand & Company

At the level of a whole organization, unproductive workflows related to paper approvals can consume a signNow amount of working time. Signing documents such as Offer To Buy Real Estate And Acceptance NAI LeGrand & Company is an integral aspect of operations in any company, which is why the effectiveness of each agreement’s lifecycle has a profound impact on the firm’s overall productivity. With airSlate SignNow, signing your Offer To Buy Real Estate And Acceptance NAI LeGrand & Company can be as straightforward and quick as possible. You’ll have access to the latest version of nearly any document through this platform. Even better, you can sign it instantly without needing to install external software on your computer or printing out any physical copies.

Steps to acquire and sign your Offer To Buy Real Estate And Acceptance NAI LeGrand & Company

- Explore our collection by category or utilize the search bar to locate the document you require.

- View the form preview by clicking Learn more to ensure it’s the correct one.

- Click Get form to start editing immediately.

- Fill in your form and provide any necessary information using the toolbar.

- Once completed, click the Sign tool to sign your Offer To Buy Real Estate And Acceptance NAI LeGrand & Company.

- Choose the signature method that suits you best: Draw, Create initials, or upload an image of your handwritten signature.

- Click Done to finish editing and proceed to document-sharing options as needed.

With airSlate SignNow, you have everything you need to handle your documentation efficiently. You can search, complete, modify, and even send your Offer To Buy Real Estate And Acceptance NAI LeGrand & Company all in one tab without any complications. Enhance your workflows by utilizing a single, intelligent eSignature solution.

Create this form in 5 minutes or less

FAQs

-

Real Estate Investing: Should I buy a 4 units apartment to rent out to other renters or Should I buy 4 condo and rent them out to other renters? What are the con and pro for those choices?

Buy the 4plex.The reason isn't the condo fees. The reason is that a condo board can, at any time, vote to limit, or not allow renters any longer. They can even vote not to grandfather any current rentals in, which would force to to sell at an unforeseen time. The only time I recommend buying condos as an investment is when they are "fee simple," which means that each unit cares for all exterior and interior upkeep. The small board for a "fee simple" structure only deals with common elements such as landscaping, road maintenance and community activities.Now, that being said. 4plex's have issues too. It's hard to get the tax valuations lowered on them to reduce your property taxes, because they are definitely income producing. Also, you almost always have one water meter for the building, so you have to individually meter after you buy, or devise a strategy for collecting the water bill from each unit, or build the water bill into the rent. You also often have parking disputes almost tenants. Then there is the fact that you must pay for mowing and landscaping. Can you tell I've owned a few?My current purchases for rentals are as follows: Small single family homes with off street parking. I prefer ranch homes. Why? The tenant takes care of ALL utilities and landscaping. It's easy to get the taxes lowered to what I paid, because the board of revision doesn't know if it will be income producing or not. They are easy to rent. There is a huge need for single floor living due to the older population and people with disabilities. You get 3x the applications. Hope this helps!

-

How are so many Chinese people able to get money out of the country to buy real estate abroad, given the capital controls?

The most common ways are: (ranked from least effective to the most effective)1. You use your friends' or relatives' quota to convert $50k worth of USD per person per year. This is probably the more time consuming alternative but it is definitely one of the safest way of getting enough foreign currency legitimately for overseas investments.2. Similar to the method above, but instead of exchanging currency at the local bank, you exchange it with scalpers for a more competitive rate and bypassing the US$50k cap. Scalpers are everywhere near these official currency exchange branches. 3. Illegal off-shore money exchange, known locally as 'Qian Zhuang'. This is a much more convenient way of transferring funds as it not only allows you to transfer without a limit, but it also eliminates the need for you to physically carry the cash to your destination. However you do need to pay a premium as well as facing the risk of being scammed of your money. This is more of an issue if you use less reputable Qian Zhuangs typically because your destination country is not one of the more popular ones. 4. Walk into Bank of China in GuangZhou. Yup, the state bank actually has a program (called 'You Hui Tong') that allows you to transfer unlimited amount of CNY to the foreign currency of your choice. When you think about it, the US alone estimated that $22 billion of its real estate purchases in 2013 was done by Chinese buyers. That would have caused an awful lot of people queuing up to exchange for the green back, $50k at a time. You Hui Tong was created somewhere in 2011 and became the easiest and the most legitimate way of foreign currency exchange. It has recently been exposed by CCTV that this program directly violates China's foreign currency control. However the consensus is that the $50k cap has become quite a draconian policy and I honestly have never come across a Chinese investor losing sleep over this. The bottom line: if you can make enough money in China to afford an overseas real estate investment, then you should be capable of finding a way to swap Chairman Mao with Benjamin Franklin on a piece of paper.

-

How do you invest in real estate for rental income? What are the pros and cons to buying and renting out an apartment as opposed to a house?

I love investing in rental real estate for the income instead of appreciation. It’s a much more surefire way to build wealth.My practice is dedicated to assisting real estate investors and their are two huge causes for investment failure that I see time and time again.Not knowing the market and the neighborhood you are investing in;Failing to understand financial formulas and operating costs.Figure those two things out and you will do well. I’m not a handy person, so I build property management and maintenance expenses into my financial models. I spend months researching an area before I feel comfortable investing in it.Houses are nice because they have better exit options. Everyone wants to buy a house. Additionally, the tenants usually mow the lawn and service the property with minor maintenance issues.Multi-family, in my opinion, is a much better route to take (and the one I’ve taken). The exit options are reduced as not everyone wants to buy multi-family, but the you benefit from economies of scale.For instance, I have three-units, but one roof to repair and one yard to mow.When one tenant moves out, I still have two more that are paying on a monthly basis. Vacancy becomes much less painful.Hope this helps!

-

How do I get the capital or loans to invest in real estate and rent real estate out?

It depends whether you’re investing in commercial or residential real estate.The process to receive funding for a real estate investment differs on the type of property you’re looking to invest in, with the first and most important decision being between Residential real estate (homes and 2–4 unit Multifamily buildings), and Commercial real estate (buildings occupied by companies, or 5+ unit Multifamily properties).If you are looking to get started with Residential real estate investing and not sure where to start, there is a lot of great content on BiggerPockets: The Real Estate Investing Social Network - both guides and forums with other investors. The short answer is that funding will largely be based on your own credit score and finances.If you are looking to get involved in Commercial real estate, the process for receiving funding is a little bit different. Broadly, you can raise Equity (co-owners of your property), and generally you’ll supplement the total equity with Debt (an interest-bearing loan against the property).If you’re going commercial and have enough equity lined up, between yourself or an LLC with multiple investors including yourself, then next step is to find the property to invest in and create a great plan. Lenders in commercial real estate will evaluate the property itself and the plan, to determine metrics like the ratio of the property’s income to interest owed (Debt Service Coverage Ratio), the percent of the building value represented by the loan (Loan to Value), and some other measures of return and risk. These factors, plus your experience and financial strength, will determine the type of loan you qualify for. Banks, private lenders, and several other types of entities play in the commercial loan space.We’ve made it easy to find the best property-backed commercial lenders in the US by creating a platform that guides you through the loan application process, and instantly matches you with top lenders that are pre-selected for your deal scenario. Check out StackSource to learn more, or feel free to ask me other questions related to commercial real estate lending!

-

Real Estate Investing: What should I and my buddy know before we buy a multi-family residential building to successfully renovate and rent it out at a profit?

I’ll approach this from the return on investment angle. Of course, there are lots of other responses along the lines of remodeling knowledge, local market knowledge, finance knowledge, etc. One of the axioms of real estate investing is that you make your money when you buy the property. To do so, you need understand your exit strategy, knowing when you plan to sell and the expected value at that time. From there, you back into what you can pay for the property today. It’s simple math really: final value less sale commissions, costs for design, permits, renovation, carry, and financing, and desired profit equals what you can pay for the property. Of course, the devil is in the details.The tricky part is establishing a credible estimate of those costs. If you are not in the construction or development world today, get to know someone who is and would be willing to mentor you along in this. Items to consider include: architect and engineering, permits (including how long it will take to get them), renovation costs, potential off-site costs (cities love new sidewalks), tenant improvements, commissions, financing, administrative costs, etc.Now if your plan is to keep the investment for cash flow, you would target what the stabilized proforma, or projected income stream will look like once your renovation is complete and you’ve leased up the property. Once you know that, you can project what the value will be and amount of debt it will support. Lenders will look at this from three perspectives: cash flow to debt service, loan to value, and loan to cost. Trust me, the almost always take the lower of the three. Knowing the amount financing your stabilized property will obtain will tell you how much equity you must come up with to pay for the property and renovation costs (hard and soft). You can raise this from your personal reserves or if it’s your first project, friends and family. Some other pieces of advice:Work with competent experts. Hire a good real estate attorney to work for you. Find a smart real estate broker who knows the market you’re interested in.Don’t be embarrassed to seek out experienced developers and investors for advice.Always include an appropriate contingency reserve (5% of hard costs and 3-5% of soft costs)Getting permits almost always takes longer than what the municipality tells you it will take.Don’t allow your earnest money deposit to become non-refundable until you have all of your ducks in a row: Solid proforma, funding nailed down, completed understanding of the permit process (try to not be required to close until you have obtained the necessary permits)

-

I'm 19 and thinking of getting into real estate. How much would I need to save to start up, both for buy to let and residential options?

This is how I started in Real Estate and you are at a good age to do it. There is a great deal more to remember than just saving enough to buy and let a property. That’s easy. The harder part is buying the right property because success in real estate is often about location, location, location and once you own a property, even it it doesn’t perform, even if it depreciates, you still have to pay taxes and maintain it. So with that in mind remember that a poor or mediocre house in a good or up and coming neighborhood is almost always better than a great house in a bad or declining neighborhood. Do your research and find out where you want to buy before you even start looking for a property. Make connections with a realtor — and not the first one you meet, actually go an interview them — and then work with them based on your chemistry, their understanding of what you want and how well you get along. If you make the right partnership, a good realtor can help you make a great deal of money and it’s something that could last years and years and as the realtor becomes more successful, he or she will help propel you to success as well. They will also work to help you find tenants for your apartments. This is much more challenging than it sounds and it is time consuming and worrisome. A bad tenant is a disaster and you want to avoid that if at all possible. It doesn’t hurt to take a real estate course either. There are different kinds of courses such as a course that helps you get your real estate license or one that focuses on valuation of properties. If real estate development and accrual is your goal, either or both of these courses will be valuable.Now you have to think about the money. If you have a steady income from a regular job you can purchase a property with as little as 5 percent down plus closing costs, but you will have to pay PMI. PMI is a total rip-off and you need to keep an eye on it. Make sure you always know what your building is worth because once you hit 20 percent loan-to-value you can have PMI removed. But if you don’t pay attention the bank WILL NEVER TELL YOU when you no longer need PMI and will let you pay forever. That’s good money thrown down the sewer.One of the best strategies I have found is to buy a multi-family property because the bank assumes the rental income as part of your income and it allows you to purchase a much bigger building. For example, when I started I could only afford a house in the 100,000 range, but by purchasing a multi-family, I was able to get a house in the 200,000 dollar range. Not only did I have a place to live, but I was getting income from the apartments that reduced the amount I had to use to pay the mortgage.When you are starting out and money is tight you have to seriously consider your strategy. Are you purchasing to hold? Purchasing to re-sell for appreciation? Flipping fast? Or what? Each will determine the kind of mortgage you want to get. For couples starting out in life I always recommend a 30 year fixed mortgage because it’s safest mortgage with the easiest monthly payments. Although an ARM may have a lower rate, it’s for a short time and at the end, the monthly payment could skyrocket and you could lose the house if you can’t make the payment. But if your goal is to get in, fix up the house on the cheap and get out, then a short term ARM with a low rate is a good idea. But you really have to get out before the ARM expires and the rate goes up. If you plan to hold and let the property appreciate and it’s a multi-family that makes good income then get that 30 year fixed mortgage and let your money work for you instead of you working for your money. Keep an eye on mortgage rates and don’t be afraid to refinance as rates go down. The name of the game is maximizing the money in your pocket today and in the long run and the lower the rate, the more money you get to keep in your pocket month after month instead of paying to the mortgage company. When you’ve had enough and the building has appreciated enough, then you can sell it and take profits.You will want to make connections with certain people if you are going to collect properties. You want a good tax accountant; you want a good contractor who can repair the buildings fast and cheaply (good is desirable too, but it depends on your strategy — if you are flipping, “good” is a relative thing - “good enough” is the more likely strategy because time is money and YOU WANT TO GET OUT FAST when you are flipping.). You will need a landscaper or someone who can take care of the property and a manager who the tenants can call at 3AM to fix their clogged toilet. At the beginning, you will be all these things yourself but as you acquire property it will become too onerous to do it yourself. Taxation, in particular, is complicated. There are depreciation schedules and write-offs and if this is your real business, then there are even more complications and write-offs, but usually a tax professional knows how to handle them. You will need the numbers of a plumber, a locksmith, an electrician, your insurance agent and eventually a lawyer, especially if you decide to incorporate to limit liability.People think they can find cheap properties in foreclosures and short sales and often you can — but you usually have to be capable of putting up 10,000 dollars in a certified check immediately and then you have to be capable of getting a mortgage for the rest in a reasonable time frame. This requires either saving enough for the check, a big down payment and the ability to make the mortgage or a partner with deep pockets who can finance you for a piece of the pie.If you start to accrue properties there will come an inflection point when the income from the rents will be enough to sustain you and allow you to live a better life but that will not be right away. You will have to work at another, secure job for awhile to keep income coming in. You can refinance, consolidate loans and use property for leverage to purchase more properties but you must maintain a fine balance and not over-leverage yourself. Too much debt can bring the entire thing down like a house of cards. You have to reduce costs through re-fis and consolidation but you also have to work to maximize revenues through rents, appreciation and sales.Real estate has been a tried-and-true mechanism for generating wealth throughout the centuries and you can do it, too, if you are careful.

-

What is the best way to make money investing in real estate? Ideally they would be need to be deals that are less than $75k. Should I buy foreclosures or get a loan from the bank? Do I flip the property, or buy it and rent it out?

Note: I am not clear on the background (time commitments, risk tolerance etc.) of the OP. Hence, I will provide a generic answer. Here it goes:There is no "best way" to make money in Real Estate. Here's a simple analogy to help you understand.What you are asking is like walking into a Chinese buffet for lunch and asking "Which item in the buffet will fill you up?" Answer: Everything will fill you up.It depends on your preferences, and whether you are vegetarian, whether you are allergic, how full you already are, and so on.In real estate, everything makes you money. Also everything makes you losses. Here's the secret to making money in real estate. Learn one or two strategies and get good at them. Get really good at them. And you will make money.Typically, these are the 4 constraints that will impact your ability to decide on a strategy.1. Knowledge - The how tos and the art of investing. Includes underwriting, analysis, negotiation, finding deals and so on. It's about knowing what deals to NOT do, that will impact your ability to make money in the long run. E.g. when flipping, you need to buy a property max at 70-75% of its After Repair Value (ARV). Else, you will likely break even or not make any money.2. Capital - How much capital you have access to. You will approach real estate differently if you have $1 million cash versus $10,000 cash in your bank account.3. Time - How much time you can allocate to investing will determine the type of deals you can find and do. With time on your hands, you can find your own deals and maximize your returns. If you have a family and busy with life, find realtors or wholesalers, give them your investing criteria, and they will find deals for you to invest in. However, there is an expense associated with using middle men. Your returns will be lower.4. Risk tolerance - Short term risk, long term risk, do you need to make money tomorrow or are you ok with waiting 10 years?Finally, here's the pros and cons of a number of investing methods from my experience. I have written these in increasing order of capital (money) required since capital is the biggest constraints for most new investors.1. Wholesaling: You are finding an undervalued deal. E.g. you find a $100k property and negotiate with seller and get it under contract for $80k. Before the deal closes, you sell the contract to another investor for $85k, and pocket $5k at closing. You do not get to own properties. You need to be a hustler.Knowledge required: HighCapital: Low ($3-5k only)Time Commitment: High Risk: Very lowPros- Gets your feet wet in Real Estate. And make risk free moneyCons- Not a consistent source of income, you don't get to build long term wealth, not passive income.2. Creative investing: Doing funky things with real estate finance. Such as buying on terms, vendor take backs, mortgage wraps, rent to own and so on. This is one of the most lucrative ways to invest in Real estate. You become owner of properties with little money down. And you build long term wealth.Knowledge required: Very HighCapital: Low-MedTime commitment: HighRisk: depends on how the deal is being structured / financed3. Flipping - You buy run down properties, and flip them for a profit. You make large chunks of cash when you are able to fix up and sell property. I don't have a construction background so I always partner with contractor buddies for these deals.Knowledge required: Low-medium (one excel sheet is all you need with some rules of thumb. Look at the flipping calculator on bigger pockets.www.Biggerpockets.com)Capital: Med-HighTime commitment: MedRisk: Medium-High4. Buy and hold: You buy rental property and hold on to it. What I have heard from realtor friends is that the wealthiest people they know are buy and hold investors. You are leveraging the banks money and making money on appreciation in the long term. Prep for a 15-20 year hold. You can always refinance and cash out periodically. However, you have to be OK with vacancy periods, tenant headaches and market downturns.Always strive to buy cash flowing offmarket properties. These will typically not be on MLS. (Sorry for the realtors who might disagree - but I am YET to buy a property on MLS which has made me money)Knowledge required: Low-MedCapital: HighTime commitment: LowRisk: Short term risks are high. Over the long term, the risks are low5. Foreclosures - Quite lucrative in the US. Not so much in Canada. Key is to find the foreclosures in excellent areas of town. Low crimes, good schools etc.Knowledge required: Low-MedCapital: Med-HighTime commitment: MedRisk: Short term risks are high. Over the long term, the risks are low.Disclaimer: Some of the creative techniques may or may not be possible depending on the laws in your state or country.

-

When making an offer to buy real estate, if I ask for 6% sellers assist and the closing costs are only 5%, what happens to the remaining 1%?

The guidelines for various loan programs specify the maximum amount of permissible “seller contribution” or “seller concession.” FHA loans are capped at 6%, but others are lower.The seller concession can cover only the actual closing costs. More than that, and it becomes a contribution toward the down payment, which is not generally allowed.There are two solutions when the seller concession exceeds the closing costs:Reduce the sales price by the amount of the excessApply the excess to the new loan’s principal. If the loan is $300,000 and the seller concession is $1,000 more than the closing costs, the buyer would wind up with a $299,000 loan at closing.I hope this is helpful.

Create this form in 5 minutes!

How to create an eSignature for the offer to buy real estate and acceptance nai legrand amp company

How to create an eSignature for your Offer To Buy Real Estate And Acceptance Nai Legrand Amp Company online

How to make an eSignature for your Offer To Buy Real Estate And Acceptance Nai Legrand Amp Company in Chrome

How to create an eSignature for putting it on the Offer To Buy Real Estate And Acceptance Nai Legrand Amp Company in Gmail

How to create an electronic signature for the Offer To Buy Real Estate And Acceptance Nai Legrand Amp Company straight from your smartphone

How to generate an eSignature for the Offer To Buy Real Estate And Acceptance Nai Legrand Amp Company on iOS devices

How to generate an electronic signature for the Offer To Buy Real Estate And Acceptance Nai Legrand Amp Company on Android

People also ask

-

What is the process for creating an Offer To Buy Real Estate And Acceptance with NAI LeGrand & Company?

Creating an Offer To Buy Real Estate And Acceptance with NAI LeGrand & Company is straightforward. Simply log into your airSlate SignNow account, select the appropriate template, and fill in the required details. Our intuitive platform allows you to customize the document to fit your needs, ensuring a seamless transaction.

-

How does airSlate SignNow ensure the security of my Offer To Buy Real Estate And Acceptance NAI LeGrand & Company documents?

airSlate SignNow uses advanced encryption protocols to secure all your documents, including the Offer To Buy Real Estate And Acceptance NAI LeGrand & Company. We take data protection seriously, implementing robust measures to prevent unauthorized access and ensure that your information remains confidential.

-

Are there any additional fees for using airSlate SignNow to create an Offer To Buy Real Estate And Acceptance?

No, there are no hidden fees when using airSlate SignNow for your Offer To Buy Real Estate And Acceptance NAI LeGrand & Company. Our pricing is transparent and designed to provide you with a cost-effective solution for all your document signing needs.

-

Can I integrate airSlate SignNow with other tools when preparing an Offer To Buy Real Estate And Acceptance NAI LeGrand & Company?

Yes, airSlate SignNow offers seamless integrations with various tools and platforms. You can connect your account with CRM systems, cloud storage services, and other applications to streamline the creation and signing process of your Offer To Buy Real Estate And Acceptance NAI LeGrand & Company.

-

What features does airSlate SignNow provide for managing my Offer To Buy Real Estate And Acceptance NAI LeGrand & Company?

airSlate SignNow provides a range of features for managing your Offer To Buy Real Estate And Acceptance NAI LeGrand & Company. You can track document status, set reminders for signatures, and utilize templates to save time on future transactions, making the process efficient and user-friendly.

-

Is it possible to use airSlate SignNow on mobile devices for my Offer To Buy Real Estate And Acceptance NAI LeGrand & Company?

Absolutely! airSlate SignNow is fully optimized for mobile devices, allowing you to create, send, and sign your Offer To Buy Real Estate And Acceptance NAI LeGrand & Company on the go. Our mobile app ensures that you can manage your documents anytime and anywhere.

-

How can airSlate SignNow benefit my real estate business when handling Offers To Buy Real Estate And Acceptance NAI LeGrand & Company?

Using airSlate SignNow can signNowly enhance your real estate business by streamlining the document signing process. It allows for quicker transactions, reduces paperwork, and provides a professional image to your clients when managing Offers To Buy Real Estate And Acceptance NAI LeGrand & Company.

Get more for Offer To Buy Real Estate And Acceptance NAI LeGrand & Company

- Mediation intake form 328552388

- Health science academy volunteer log form

- Valic payroll deduction forms

- Medical proforma

- Sworn declaration of intention to depart from the philippines permanently form

- Childrens home inventory for listening difficulties form

- Counseling facility license application form

- Request for passport waiver letter form

Find out other Offer To Buy Real Estate And Acceptance NAI LeGrand & Company

- Help Me With eSignature Florida Courts Affidavit Of Heirship

- Electronic signature Alabama Banking RFP Online

- eSignature Iowa Courts Quitclaim Deed Now

- eSignature Kentucky Courts Moving Checklist Online

- eSignature Louisiana Courts Cease And Desist Letter Online

- How Can I Electronic signature Arkansas Banking Lease Termination Letter

- eSignature Maryland Courts Rental Application Now

- eSignature Michigan Courts Affidavit Of Heirship Simple

- eSignature Courts Word Mississippi Later

- eSignature Tennessee Sports Last Will And Testament Mobile

- How Can I eSignature Nevada Courts Medical History

- eSignature Nebraska Courts Lease Agreement Online

- eSignature Nebraska Courts LLC Operating Agreement Easy

- Can I eSignature New Mexico Courts Business Letter Template

- eSignature New Mexico Courts Lease Agreement Template Mobile

- eSignature Courts Word Oregon Secure

- Electronic signature Indiana Banking Contract Safe

- Electronic signature Banking Document Iowa Online

- Can I eSignature West Virginia Sports Warranty Deed

- eSignature Utah Courts Contract Safe