Form 8804 Schedule a Penalty for Underpayment of Estimated Section 1446 Tax by Partnerships 2014

What is the Form 8804 Schedule A Penalty For Underpayment Of Estimated Section 1446 Tax By Partnerships

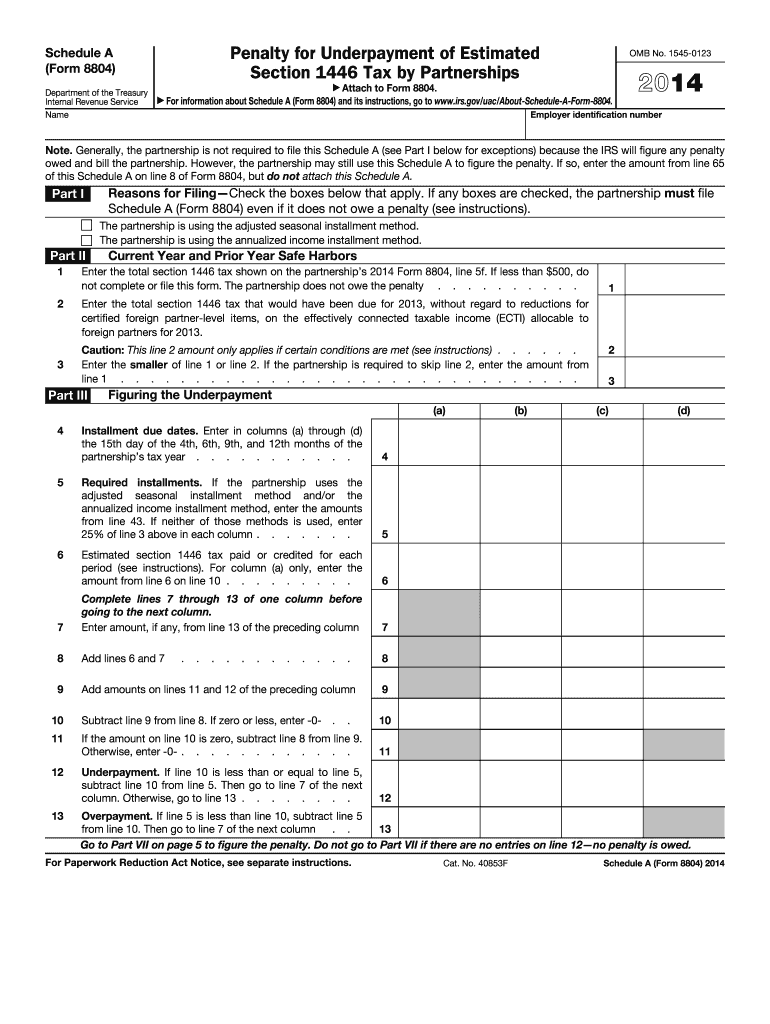

The Form 8804 Schedule A is specifically designed for partnerships that are subject to Section 1446 of the Internal Revenue Code. This form addresses penalties incurred due to underpayment of estimated taxes owed by partnerships. Partnerships that have foreign partners must ensure compliance with these tax obligations to avoid penalties. The penalties can arise if the partnership fails to pay the required estimated tax amounts on time, which can lead to additional financial burdens and complications in tax filings.

Steps to complete the Form 8804 Schedule A Penalty For Underpayment Of Estimated Section 1446 Tax By Partnerships

Completing the Form 8804 Schedule A involves several key steps:

- Gather necessary financial information, including partnership income and deductions.

- Calculate the total estimated tax liability for the partnership.

- Determine the amount of tax that has already been paid or credited.

- Calculate any penalties for underpayment by comparing the estimated tax due with the amounts already paid.

- Complete the form accurately, ensuring all fields are filled out as required.

- Review the completed form for accuracy and compliance with IRS guidelines.

How to obtain the Form 8804 Schedule A Penalty For Underpayment Of Estimated Section 1446 Tax By Partnerships

The Form 8804 Schedule A can be obtained directly from the Internal Revenue Service (IRS) website. It is crucial to ensure that you are using the most current version of the form to avoid issues with your submission. Additionally, many tax preparation software solutions include this form, allowing for easier completion and filing. Always ensure that you are accessing official resources to obtain the form to guarantee its validity.

Penalties for Non-Compliance

Failing to comply with the requirements of the Form 8804 Schedule A can result in significant penalties. These penalties may include interest on the unpaid tax amount and additional fines for late payments. The IRS may assess these penalties based on the amount of underpayment and the duration of the non-compliance. It is essential for partnerships to stay informed about their tax obligations to avoid these financial repercussions.

IRS Guidelines

The IRS provides specific guidelines regarding the completion and submission of the Form 8804 Schedule A. These guidelines outline the necessary information required, deadlines for submission, and the penalties associated with underpayment. Partnerships should familiarize themselves with these guidelines to ensure compliance and minimize the risk of incurring penalties. Regular consultation with tax professionals can also provide clarity on these regulations.

Filing Deadlines / Important Dates

Partnerships must adhere to strict filing deadlines for the Form 8804 Schedule A. Typically, the form is due on the 15th day of the fourth month following the end of the partnership's tax year. It is crucial to mark these dates on your calendar to ensure timely submission. Missing these deadlines can lead to penalties and interest on unpaid taxes, which can significantly increase the financial burden on the partnership.

Quick guide on how to complete 2014 form 8804 schedule a penalty for underpayment of estimated section 1446 tax by partnerships

Discover the simplest method to complete and sign your Form 8804 Schedule A Penalty For Underpayment Of Estimated Section 1446 Tax By Partnerships

Are you still spending time preparing your official documents on paper instead of online? airSlate SignNow offers a superior way to complete and sign your Form 8804 Schedule A Penalty For Underpayment Of Estimated Section 1446 Tax By Partnerships and associated forms for public services. Our intelligent eSignature solution equips you with all the necessary tools to handle paperwork swiftly and in compliance with official standards - robust PDF editing, management, security, signing, and sharing features all available within a user-friendly interface.

Only a few steps are needed to complete and sign your Form 8804 Schedule A Penalty For Underpayment Of Estimated Section 1446 Tax By Partnerships:

- Upload the editable template to the editor using the Get Form button.

- Verify the information you need to include in your Form 8804 Schedule A Penalty For Underpayment Of Estimated Section 1446 Tax By Partnerships.

- Move between the fields using the Next option to ensure nothing is overlooked.

- Utilize Text, Check, and Cross tools to fill in the fields with your information.

- Modify the content with Text boxes or Images from the upper toolbar.

- Emphasize what is important or Conceal sections that are no longer relevant.

- Click on Sign to create a valid eSignature using your preferred method.

- Place the Date next to your signature and conclude your work with the Done button.

Store your completed Form 8804 Schedule A Penalty For Underpayment Of Estimated Section 1446 Tax By Partnerships in the Documents folder of your profile, download it, or transfer it to your preferred cloud storage. Our solution also offers versatile form sharing. There’s no need to print your templates when you can send them directly to the proper public office - do it via email, fax, or by requesting a USPS “snail mail” delivery from your account. Experience it today!

Create this form in 5 minutes or less

Find and fill out the correct 2014 form 8804 schedule a penalty for underpayment of estimated section 1446 tax by partnerships

FAQs

-

As one of the cofounders of a multi-member LLC taxed as a partnership, how do I pay myself for work I am doing as a contractor for the company? What forms do I need to fill out?

First, the LLC operates as tax partnership (“TP”) as the default tax status if no election has been made as noted in Treasury Regulation Section 301.7701-3(b)(i). For legal purposes, we have a LLC. For tax purposes we have a tax partnership. Since we are discussing a tax issue here, we will discuss the issue from the perspective of a TP.A partner cannot under any circumstances be an employee of the TP as Revenue Ruling 69-184 dictated such. And, the 2016 preamble to Temporary Treasury Regulation Section 301.7701-2T notes the Treasury still supports this revenue ruling.Though a partner can engage in a transaction with the TP in a non partner capacity (Section 707a(a)).A partner receiving a 707(a) payment from the partnership receives the payment as any stranger receives a payment from the TP for services rendered. This partner gets treated for this transaction as if he/she were not a member of the TP (Treasury Regulation Section 1.707-1(a).As an example, a partner owns and operates a law firm specializing in contract law. The TP requires advice on terms and creation for new contracts the TP uses in its business with clients. This partner provides a bid for this unique job and the TP accepts it. Here, the partner bills the TP as it would any other client, and the partner reports the income from the TP client job as he/she would for any other client. The TP records the job as an expense and pays the partner as it would any other vendor. Here, I am assuming the law contract job represents an expense versus a capital item. Of course, the partner may have a law corporation though the same principle applies.Further, a TP can make fixed payments to a partner for services or capital — called guaranteed payments as noted in subsection (c).A 707(c) guaranteed payment shows up in the membership agreement drawn up by the business attorney. This payment provides a service partner with a guaranteed payment regardless of the TP’s income for the year as noted in Treasury Regulation Section 1.707-1(c).As an example, the TP operates an exclusive restaurant. Several partners contribute capital for the venture. The TP’s key service partner is the chef for the restaurant. And, the whole restaurant concept centers on this chef’s experience and creativity. The TP’s operating agreement provides the chef receives a certain % profit interest but as a minimum receives yearly a fixed $X guaranteed payment regardless of TP’s income level. In the first year of operations the TP has low profits as expected. The chef receives the guaranteed $X payment as provided in the membership agreement.The TP allocates the guaranteed payment to the capital interest partners on their TP k-1s as business expense. And, the TP includes the full $X guaranteed payment as income on the chef’s K-1. Here, the membership agreement demonstrates the chef only shares in profits not losses. So, the TP only allocates the guaranteed expense to those partners responsible for making up losses (the capital partners) as noted in Treasury Regulation Section 707-1(c) Example 3. The chef gets no allocation for the guaranteed expense as he/she does not participate in losses.If we change the situation slightly, we may change the tax results. If the membership agreement says the chef shares in losses, we then allocate a portion of the guaranteed expense back to the chef following the above treasury regulation.As a final note, a TP return requires knowledge of primary tax law if the TP desires filing a completed an accurate partnership tax return.I have completed the above tax analysis based on primary partnership tax law. If the situation changes in any manner, the tax outcome may change considerably. www.rst.tax

Create this form in 5 minutes!

How to create an eSignature for the 2014 form 8804 schedule a penalty for underpayment of estimated section 1446 tax by partnerships

How to generate an eSignature for your 2014 Form 8804 Schedule A Penalty For Underpayment Of Estimated Section 1446 Tax By Partnerships online

How to generate an electronic signature for the 2014 Form 8804 Schedule A Penalty For Underpayment Of Estimated Section 1446 Tax By Partnerships in Google Chrome

How to create an electronic signature for putting it on the 2014 Form 8804 Schedule A Penalty For Underpayment Of Estimated Section 1446 Tax By Partnerships in Gmail

How to generate an eSignature for the 2014 Form 8804 Schedule A Penalty For Underpayment Of Estimated Section 1446 Tax By Partnerships from your smartphone

How to make an eSignature for the 2014 Form 8804 Schedule A Penalty For Underpayment Of Estimated Section 1446 Tax By Partnerships on iOS devices

How to generate an electronic signature for the 2014 Form 8804 Schedule A Penalty For Underpayment Of Estimated Section 1446 Tax By Partnerships on Android devices

People also ask

-

What is the Form 8804 Schedule A Penalty For Underpayment Of Estimated Section 1446 Tax By Partnerships?

The Form 8804 Schedule A Penalty For Underpayment Of Estimated Section 1446 Tax By Partnerships is a penalty that partnerships may incur if they fail to pay estimated taxes on income effectively connected with a U.S. trade or business. This form is crucial for compliance with IRS regulations, ensuring that partnerships pay their fair share of taxes on time.

-

How can airSlate SignNow help me with Form 8804 Schedule A filings?

airSlate SignNow streamlines the process of collecting signatures and managing documents related to Form 8804 Schedule A filings. By using our platform, partnerships can easily eSign necessary documents, ensuring accurate and timely submissions to avoid penalties for underpayment of estimated Section 1446 tax.

-

What features does airSlate SignNow offer for managing tax documents?

airSlate SignNow offers a variety of features, including customizable templates, real-time tracking, and secure cloud storage for managing tax documents like Form 8804 Schedule A. These features simplify the document management process, making it easier for partnerships to comply with tax obligations.

-

Is there a cost associated with using airSlate SignNow for Form 8804 Schedule A?

Yes, airSlate SignNow offers various pricing plans tailored to fit different business needs. By investing in our service, partnerships can signNowly reduce the risk of incurring penalties related to Form 8804 Schedule A filings while benefiting from our efficient eSignature solutions.

-

Can I integrate airSlate SignNow with my accounting software for Form 8804 Schedule A management?

Absolutely! airSlate SignNow integrates seamlessly with popular accounting software, allowing you to manage Form 8804 Schedule A and other tax documents more efficiently. This integration helps streamline your workflow, ensuring all necessary forms are completed and submitted on time.

-

What are the benefits of using airSlate SignNow for tax-related documents?

Using airSlate SignNow for tax-related documents, including Form 8804 Schedule A, provides numerous benefits, such as enhanced security, faster turnaround times, and reduced paperwork. Our easy-to-use platform ensures that partnerships can focus on their core business while we handle the documentation.

-

How does airSlate SignNow ensure the security of my Form 8804 Schedule A documents?

airSlate SignNow prioritizes the security of your documents, including Form 8804 Schedule A, with advanced encryption and compliance with industry standards. This ensures that your sensitive tax information is protected throughout the eSigning process.

Get more for Form 8804 Schedule A Penalty For Underpayment Of Estimated Section 1446 Tax By Partnerships

- Kids r first child care centre preschool parent handbook kidsrfirstchildcare form

- Us passport renewal fillable savable form

- Sterilization record log form

- Thrift savings plan form 76

- Insinkerator rebate form

- Form to apply for an original license or to change or renew an existing license

- Irs form 4989

- Distinguished veteran pass application for pass terms and form

Find out other Form 8804 Schedule A Penalty For Underpayment Of Estimated Section 1446 Tax By Partnerships

- How Can I Sign California Residential lease agreement form

- How To Sign Georgia Residential lease agreement form

- Sign Nebraska Residential lease agreement form Online

- Sign New Hampshire Residential lease agreement form Safe

- Help Me With Sign Tennessee Residential lease agreement

- Sign Vermont Residential lease agreement Safe

- Sign Rhode Island Residential lease agreement form Simple

- Can I Sign Pennsylvania Residential lease agreement form

- Can I Sign Wyoming Residential lease agreement form

- How Can I Sign Wyoming Room lease agreement

- Sign Michigan Standard rental agreement Online

- Sign Minnesota Standard residential lease agreement Simple

- How To Sign Minnesota Standard residential lease agreement

- Sign West Virginia Standard residential lease agreement Safe

- Sign Wyoming Standard residential lease agreement Online

- Sign Vermont Apartment lease contract Online

- Sign Rhode Island Tenant lease agreement Myself

- Sign Wyoming Tenant lease agreement Now

- Sign Florida Contract Safe

- Sign Nebraska Contract Safe