Form N 323, , Carryover of Tax Credits Hawaii Gov 2013

What is the Form N-323, Carryover of Tax Credits Hawaii gov

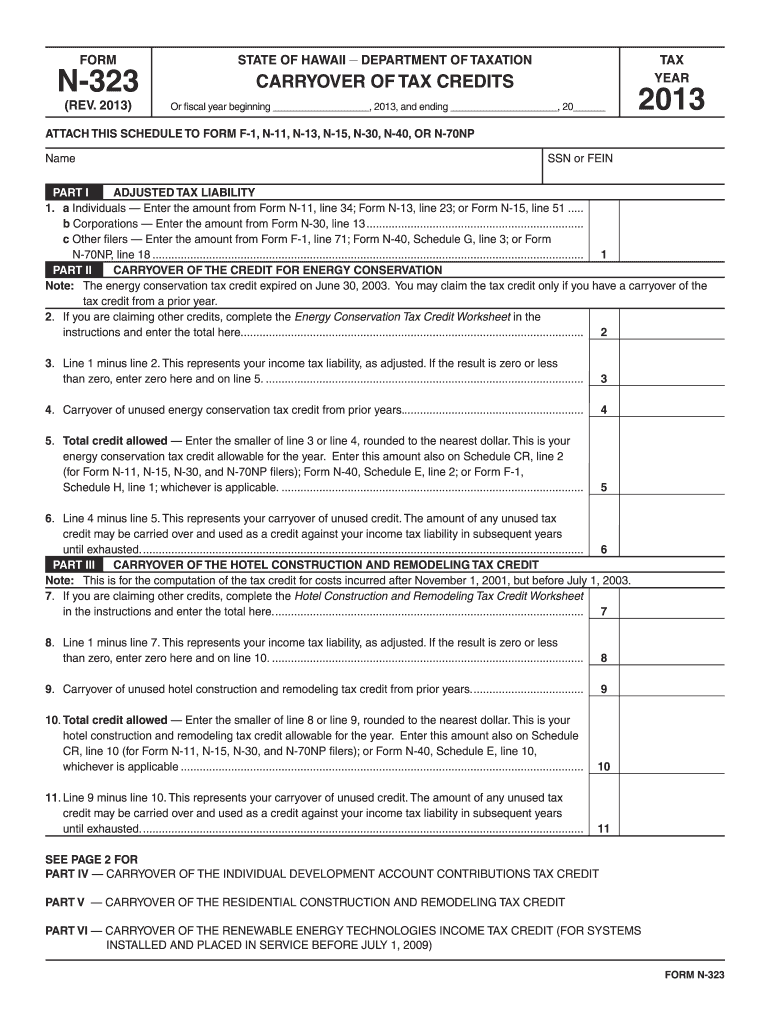

The Form N-323 is a tax form used in Hawaii for reporting the carryover of tax credits. This form allows taxpayers to claim credits that they were unable to use in previous tax years, ensuring they can benefit from these credits in the current tax year. The carryover provisions are particularly important for individuals and businesses that may have incurred expenses eligible for tax credits but did not have sufficient tax liability to utilize them fully. Understanding the specifics of this form is essential for accurate tax reporting and compliance with state tax regulations.

Steps to Complete the Form N-323, Carryover of Tax Credits Hawaii gov

Completing Form N-323 involves several key steps to ensure accurate reporting of tax credits. Begin by gathering all necessary documentation related to the tax credits you wish to carry over. This may include previous tax returns, credit certificates, and any supporting documents that validate your claims. Next, fill in your personal information, including your name, address, and taxpayer identification number. Follow the instructions provided on the form to accurately report the amount of credit being carried over. It is crucial to double-check all entries for accuracy before submission to avoid potential issues with the Hawaii Department of Taxation.

How to Obtain the Form N-323, Carryover of Tax Credits Hawaii gov

The Form N-323 can be obtained directly from the Hawaii Department of Taxation's website. It is available as a downloadable PDF, which allows you to print and fill it out manually. Alternatively, if you prefer to complete the form digitally, you can use online tax software that supports Hawaii tax forms. Ensure that you have the most current version of the form to comply with any changes in tax laws or regulations.

Legal Use of the Form N-323, Carryover of Tax Credits Hawaii gov

Form N-323 is legally recognized for reporting tax credit carryovers in Hawaii. To ensure its legal validity, it must be filled out accurately and submitted within the specified deadlines. The form should be signed and dated by the taxpayer or their authorized representative. Utilizing an electronic signature, where permitted, can streamline the submission process while maintaining compliance with legal standards. It is advisable to keep a copy of the completed form and any supporting documents for your records, as they may be required for future reference or audits.

Filing Deadlines / Important Dates

Filing deadlines for Form N-323 align with Hawaii's tax return deadlines. Typically, individual taxpayers must file their state tax returns by April 20th of the following year. However, if you are filing for an extension, be aware of the extended deadlines and ensure that Form N-323 is submitted accordingly. Staying informed about these dates is crucial to avoid penalties and ensure that you can fully utilize your carryover credits.

Form Submission Methods (Online / Mail / In-Person)

Form N-323 can be submitted through various methods, accommodating different preferences. Taxpayers can file the form online using approved tax software that supports Hawaii forms, which often allows for quicker processing. Alternatively, the completed form can be mailed to the Hawaii Department of Taxation, ensuring it is postmarked by the filing deadline. For those who prefer in-person submissions, visiting a local tax office may be an option, although this method may require an appointment and adherence to local health guidelines.

Quick guide on how to complete form n 323 2013 carryover of tax credits hawaiigov

Your assistance manual on how to prepare your Form N 323, , Carryover Of Tax Credits Hawaii gov

If you’re curious about how to finalize and submit your Form N 323, , Carryover Of Tax Credits Hawaii gov, here are a few straightforward recommendations on how to streamline tax reporting.

To begin, you simply need to set up your airSlate SignNow account to transform how you manage documents online. airSlate SignNow is an exceptionally user-friendly and robust document solution that enables you to modify, generate, and complete your income tax forms effortlessly. With its editor, you can toggle between text, check boxes, and eSignatures and revert to modify information as necessary. Simplify your tax administration with advanced PDF editing, eSigning, and user-friendly sharing.

Follow the procedures below to complete your Form N 323, , Carryover Of Tax Credits Hawaii gov in a few minutes:

- Set up your account and begin working on PDFs in just a few minutes.

- Utilize our catalog to find any IRS tax form; browse through variants and schedules.

- Click Get form to access your Form N 323, , Carryover Of Tax Credits Hawaii gov in our editor.

- Populate the necessary fillable fields with your information (text, numbers, check marks).

- Use the Sign Tool to add your legally-binding eSignature (if necessary).

- Review your document and amend any mistakes.

- Save modifications, print your copy, send it to your recipient, and download it to your device.

Utilize this manual to file your taxes online with airSlate SignNow. Please be aware that filing on paper can lead to increased return errors and delays in reimbursements. Additionally, before e-filing your taxes, check the IRS website for declaration guidelines in your state.

Create this form in 5 minutes or less

Find and fill out the correct form n 323 2013 carryover of tax credits hawaiigov

FAQs

-

If you played one of those $10,000 a spin slot machines in Vegas would that mean that anytime it won anything even one credit I would still have to fill out a tax form?

Yes, although they can set the machine to accumulated credit mode, and a staffer will sit by recording each jackpot on a form, then quickly resetting the machine so it’s ready to go again. You get a single W2G at the end of the session.It’s close to impossible to play extremely high-limit machines at any decent speed by feeding it currency and stopping for traditional hand-pays.

-

The company I work for is taking taxes out of my paycheck but has not asked me to complete any paperwork or fill out any forms since day one. How are they paying taxes without my SSN?

WHOA! You may have a BIG problem. When you started, are you certain you did not fill in a W-4 form? Are you certain that your employer doesn’t have your SS#? If that’s the case, I would be alarmed. Do you have paycheck stubs showing how they calculated your withholding? ( BTW you are entitled to those under the law, and if you are not receiving them, I would demand them….)If your employer is just giving you random checks with no calculation of your wages and withholdings, you have a rogue employer. They probably aren’t payin in what they purport to withhold from you.

-

As one of the cofounders of a multi-member LLC taxed as a partnership, how do I pay myself for work I am doing as a contractor for the company? What forms do I need to fill out?

First, the LLC operates as tax partnership (“TP”) as the default tax status if no election has been made as noted in Treasury Regulation Section 301.7701-3(b)(i). For legal purposes, we have a LLC. For tax purposes we have a tax partnership. Since we are discussing a tax issue here, we will discuss the issue from the perspective of a TP.A partner cannot under any circumstances be an employee of the TP as Revenue Ruling 69-184 dictated such. And, the 2016 preamble to Temporary Treasury Regulation Section 301.7701-2T notes the Treasury still supports this revenue ruling.Though a partner can engage in a transaction with the TP in a non partner capacity (Section 707a(a)).A partner receiving a 707(a) payment from the partnership receives the payment as any stranger receives a payment from the TP for services rendered. This partner gets treated for this transaction as if he/she were not a member of the TP (Treasury Regulation Section 1.707-1(a).As an example, a partner owns and operates a law firm specializing in contract law. The TP requires advice on terms and creation for new contracts the TP uses in its business with clients. This partner provides a bid for this unique job and the TP accepts it. Here, the partner bills the TP as it would any other client, and the partner reports the income from the TP client job as he/she would for any other client. The TP records the job as an expense and pays the partner as it would any other vendor. Here, I am assuming the law contract job represents an expense versus a capital item. Of course, the partner may have a law corporation though the same principle applies.Further, a TP can make fixed payments to a partner for services or capital — called guaranteed payments as noted in subsection (c).A 707(c) guaranteed payment shows up in the membership agreement drawn up by the business attorney. This payment provides a service partner with a guaranteed payment regardless of the TP’s income for the year as noted in Treasury Regulation Section 1.707-1(c).As an example, the TP operates an exclusive restaurant. Several partners contribute capital for the venture. The TP’s key service partner is the chef for the restaurant. And, the whole restaurant concept centers on this chef’s experience and creativity. The TP’s operating agreement provides the chef receives a certain % profit interest but as a minimum receives yearly a fixed $X guaranteed payment regardless of TP’s income level. In the first year of operations the TP has low profits as expected. The chef receives the guaranteed $X payment as provided in the membership agreement.The TP allocates the guaranteed payment to the capital interest partners on their TP k-1s as business expense. And, the TP includes the full $X guaranteed payment as income on the chef’s K-1. Here, the membership agreement demonstrates the chef only shares in profits not losses. So, the TP only allocates the guaranteed expense to those partners responsible for making up losses (the capital partners) as noted in Treasury Regulation Section 707-1(c) Example 3. The chef gets no allocation for the guaranteed expense as he/she does not participate in losses.If we change the situation slightly, we may change the tax results. If the membership agreement says the chef shares in losses, we then allocate a portion of the guaranteed expense back to the chef following the above treasury regulation.As a final note, a TP return requires knowledge of primary tax law if the TP desires filing a completed an accurate partnership tax return.I have completed the above tax analysis based on primary partnership tax law. If the situation changes in any manner, the tax outcome may change considerably. www.rst.tax

-

How much will a doctor with a physical disability and annual net income of around Rs. 2.8 lakhs pay in income tax? Which ITR form is to be filled out?

For disability a deduction of ₹75,000/- is available u/s 80U.Rebate u/s87AFor AY 17–18, rebate was ₹5,000/- or income tax which ever is lower for person with income less than ₹5,00,000/-For AY 18–19, rebate is ₹2,500/- or income tax whichever is lower for person with income less than 3,50,000/-So, for an income of 2.8 lakhs, taxable income after deduction u/s 80U will remain ₹2,05,000/- which is below the slab rate and hence will not be taxable for any of the above said AY.For ITR,If doctor is practicing himself i.e. He has a professional income than ITR 4 should be filedIf doctor is getting any salary than ITR 1 should be filed.:)

-

Why should it be so complicated just figuring out how much tax to pay? (record keeping, software, filling out forms . . . many times cost much more than the amount of taxes due) The cost of compliance makes the U.S. uncompetitive and costs jobs and lowers our standard of living.

Taxes can be viewed as having 4 uses (or purposes) in our (and most) governments:Revenue generation (to pay for public services).Fiscal policy control (e.g., If the government wishes to reduce the money supply in order to reduce the risk of inflation, they can raise interest rates, sell fewer bonds, burn money, or raise taxes. In the last case, this represents excess tax revenue over the actual spending needs of the government).Wealth re-distribution. One argument for this is that the earnings of a country can be perceived as belonging to all of its citizens since the we all have a stake in the resources of the country (natural resources, and intangibles such as culture, good citizenship, civic duties). Without some tax policy complexity, the free market alone does not re-distribute wealth according to this "shared" resources concept. However, this steps into the boundary of Purpose # 4...A way to implement Social Policy (and similar government mandated policies, such as environmental policy, health policy, savings and debt policy, etc.). As Government spending can be use to implement policies (e.g., spending money on public health care, environmental cleanup, education, etc.), it is equivalent to provide tax breaks (income deductions or tax credits) for the private sector to act in certain ways -- e.g., spend money on R&D, pay for their own education or health care, avoid spending money on polluting cars by having a higher sales tax on these cars or offering a credit for trade-ins [ref: Cash for Clunkers]).Uses # 1 & 2 are rather straight-forward, and do not require a complex tax code to implement. Flat income and/or consumption (sales) taxes can easily be manipulated up or down overall for these top 2 uses. Furthermore, there is clarity when these uses are invoked. For spending, we publish a budget. For fiscal policy manipulation, the official economic agency (The Fed) publishes their outlook and agenda.Use # 3 is controversial because there is no Constitutional definition for the appropriate level of wealth re-distribution, and the very concept of wealth re-distribution is considered by some to be inappropriate and unconstitutional. Thus, the goal of wealth re-distribution is pretty much hidden in with the actions and policies of Use #4 (social policy manipulation).Use # 4, however, is where the complexity enters the Taxation system. Policy implementation through taxation (or through spending) occurs via legislation. Legislation (law making) is inherently complex and subject to gross manipulation by special interests during formation and amendments. Legislation is subject to interpretation, is prone to errors (leading to loopholes) and both unintentional or intentional (criminal / fraudulent) avoidance.The record keeping and forms referred to in the question are partially due to the basic formula for calculating taxes (i.e., percentage of income, cost of property, amount of purchase for a sales tax, ...). However, it is the complexity (and associated opportunities for exploitation) of taxation legislation for Use # 4 (Social Policy implementation) that naturally leads to complexity in the reporting requirements for the tax system.

Create this form in 5 minutes!

How to create an eSignature for the form n 323 2013 carryover of tax credits hawaiigov

How to generate an electronic signature for your Form N 323 2013 Carryover Of Tax Credits Hawaiigov online

How to create an electronic signature for the Form N 323 2013 Carryover Of Tax Credits Hawaiigov in Google Chrome

How to generate an eSignature for putting it on the Form N 323 2013 Carryover Of Tax Credits Hawaiigov in Gmail

How to generate an eSignature for the Form N 323 2013 Carryover Of Tax Credits Hawaiigov right from your smartphone

How to make an eSignature for the Form N 323 2013 Carryover Of Tax Credits Hawaiigov on iOS devices

How to create an eSignature for the Form N 323 2013 Carryover Of Tax Credits Hawaiigov on Android OS

People also ask

-

What is Form N 323, Carryover Of Tax Credits Hawaii gov?

Form N 323, Carryover Of Tax Credits Hawaii gov, is a state tax form used by businesses to carry over unused tax credits to future tax years. This form allows taxpayers to maximize their tax benefits by utilizing credits that they were unable to claim in the current tax year. Understanding how to properly complete this form can signNowly impact your overall tax strategy.

-

How can airSlate SignNow help with Form N 323, Carryover Of Tax Credits Hawaii gov?

airSlate SignNow offers a streamlined solution for eSigning and sending important documents, including Form N 323, Carryover Of Tax Credits Hawaii gov. With our platform, you can easily prepare, sign, and store your tax forms securely, ensuring compliance and efficiency in your tax filing process.

-

What features does airSlate SignNow offer for tax form management?

airSlate SignNow includes features such as customizable templates, automated workflows, and secure cloud storage, all essential for managing documents like Form N 323, Carryover Of Tax Credits Hawaii gov. These tools help businesses save time and reduce errors during the document preparation process, making tax season less stressful.

-

Is airSlate SignNow affordable for small businesses?

Yes, airSlate SignNow provides cost-effective pricing plans, making it accessible for small businesses looking to manage their documents efficiently. By using our platform for forms like Form N 323, Carryover Of Tax Credits Hawaii gov, you can save on printing and mailing costs, ultimately benefiting your bottom line.

-

Can I integrate airSlate SignNow with other software for tax preparation?

Absolutely! airSlate SignNow offers integrations with various accounting and tax preparation software, which can enhance your ability to manage Form N 323, Carryover Of Tax Credits Hawaii gov. These integrations allow for seamless data transfer, ensuring all your documents are in sync and readily available.

-

What are the benefits of using airSlate SignNow for eSigning tax forms?

Using airSlate SignNow for eSigning tax forms like Form N 323, Carryover Of Tax Credits Hawaii gov, offers numerous benefits, including increased efficiency and reduced turnaround times. You can sign and send documents from anywhere, which is particularly advantageous during tax season when time is of the essence.

-

How secure is airSlate SignNow for handling sensitive tax information?

airSlate SignNow prioritizes the security of your sensitive tax information, including Form N 323, Carryover Of Tax Credits Hawaii gov. Our platform uses advanced encryption and complies with industry standards to ensure that your documents are protected at all times.

Get more for Form N 323, , Carryover Of Tax Credits Hawaii gov

- Warranty deed from husband and wife to llc maryland form

- Maryland judgment form

- Letter tenant notice 497310221 form

- Md landlord tenant notice form

- Letter from tenant to landlord containing notice that premises in uninhabitable in violation of law and demand immediate repair 497310223 form

- Tenant notice repair template form

- Maryland letter notice form

- Md tenant landlord form

Find out other Form N 323, , Carryover Of Tax Credits Hawaii gov

- Electronic signature West Virginia Business Ethics and Conduct Disclosure Statement Free

- Electronic signature Alabama Disclosure Notice Simple

- Electronic signature Massachusetts Disclosure Notice Free

- Electronic signature Delaware Drug Testing Consent Agreement Easy

- Electronic signature North Dakota Disclosure Notice Simple

- Electronic signature California Car Lease Agreement Template Free

- How Can I Electronic signature Florida Car Lease Agreement Template

- Electronic signature Kentucky Car Lease Agreement Template Myself

- Electronic signature Texas Car Lease Agreement Template Easy

- Electronic signature New Mexico Articles of Incorporation Template Free

- Electronic signature New Mexico Articles of Incorporation Template Easy

- Electronic signature Oregon Articles of Incorporation Template Simple

- eSignature Montana Direct Deposit Enrollment Form Easy

- How To Electronic signature Nevada Acknowledgement Letter

- Electronic signature New Jersey Acknowledgement Letter Free

- Can I eSignature Oregon Direct Deposit Enrollment Form

- Electronic signature Colorado Attorney Approval Later

- How To Electronic signature Alabama Unlimited Power of Attorney

- Electronic signature Arizona Unlimited Power of Attorney Easy

- Can I Electronic signature California Retainer Agreement Template