§24.759 PROXY STATEMENTS:

STRATEGY & FORMS

24-410© 1992 Jefren Publishing

Company, Inc.

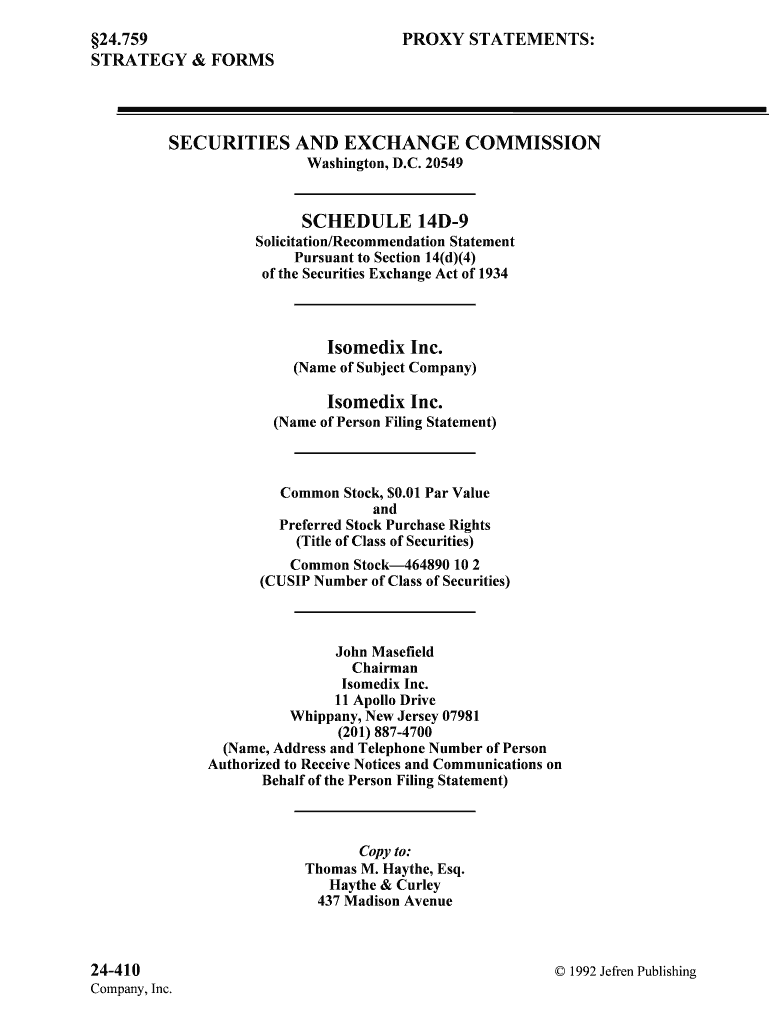

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14D-9

Solicitation/Recommendation Statement

Pursuant to Section 14(d)(4)

of the Securities Exchange Act of 1934

Isomedix Inc.

(Name of Subject Company)

Isomedix Inc.

(Name of Person Filing Statement)

Common Stock, $0.01 Par Value and

Preferred Stock Purchase Rights (Title of Class of Securities)

Common Stock—464890 10 2

(CUSIP Number of Class of Securities)

John Masefield Chairman

Isomedix Inc.

11 Apollo Drive

Whippany, New Jersey 07981 (201) 887-4700

(Name, Address and Telephone Number of Person

Authorized to Receive Notices and Communications on Behalf of the Person Filing Statement)

Copy to:

Thomas M. Haythe, Esq. Haythe & Curley

437 Madison Avenue

DISCLOSURES AND NOTICES§24.759

September 1992 24-411

New York, New York 10022

(212) 308-5900

§24.759 PROXY STATEMENTS:

STRATEGY & FORMS

24-412© 1992 Jefren Publishing

Company, Inc.

Item 1. Security and Subject Company.

The name of the subject company is lsomedix Inc. (the “Company”). The address of the

principal executive offices of the Company is 11 Apollo Drive, Whippany, New Jersey 07981.

The title of the class of equity securities to which this statement rel ates is the common stock,

$.01 par value (the “Common Stock”), of the Company including the associated Preferred Stoc k

Purchase Rights (the “Rights”) issued pursuant to the Rights Agreement dated as of June 10,

1988 between the Company and Midlantic National Bank, as rights agent (the “Rights Pla n”).

The Common Stock and the Rights together are sometimes referred to herein as the “Shares.”

Item 2. Tender Offer of the Bidder.

This statement relates to the tender offer being made by RSI Acquisition, Inc., a California

corporation (the “Offeror”) and a wholly owned subsidiary of Radiation Sterilizers, Incorporated,

a privately held California corporation (the “Parent”), as disclosed in a Tender Offe r Statement

on Schedule 14D-1 filed with the Securities and Exchange Commission by the Offeror and the

Parent on September 23, 1988, to purchase all outstanding Shares at $9 per Share, net to the

seller in cash, upon the terms and subject to the conditions set forth in the Offer t o Purchase

dated September 23, 1988 (the “Offer to Purchase”) and the related Letter of Transmittal and

Letter of Transmittal Supplement (which together constitute the “Offer”). According to the Offer

to Purchase, the principal office of the Offeror and the Parent is located at 46721 Fremont

Boulevard, Fremont, California 94538.

Item 3. Identity and Background.

(a) The name and business address of the Company, which is the person filing this

statement, are set forth in Item I above.

(b) Certain contracts, agreements, arrangements and understandings between the

Company or its affiliates and certain of the Company’s directors, executive office rs or affiliates

are described in the sections entitled “COMPENSATION OF DIRECTORS AND EXECUTIVE

OFFICERS” at pages 7 through 15 and “OTHER INFORMATION CONCERNING

DIRECTORS, OFFICERS AND STOCKHOLDERS” at pages 15 through 17 of the Company’s

Proxy Statement, dated March 31, 1988, for its 1988 Annual Meeting of Stockholders (the

“Proxy Statement”). Copies of such pages are filed as Exhibit 1 hereto and the sect ions thereof

referred to above are incorporated herein by reference.

In addition, in April 1988, the Company entered into employment agreements with each of

John Masefield, the Chairman of the Board, President, Chief Executive Officer and a di rector of

the Company; George R. Dietz, the Vice President and a director of the Company; and T homas

J. DeAngelo, the Secretary and Treasurer of the Company. The term of each employment

agreement commenced as of February 1, 1988 and ends January 31, 1991, with automatic

extensions of the term of agreement, unless a notice of non-extension is given by either part y, for

periods of one year from the expiration date of the then-current term of the agreement. The

employment agreements provide for an annual salary of $160,696 to Mr. Masefield, $103,906 to

Mr. Dietz, and $57,932 to Mr. DeAngelo, subject to increases pursuant to the Consumer Price

Index (as defined in such employment agreements) and additional increases at the disc retion of

the Board of Directors. Mr. DeAngelo’s annual salary was subsequently increased to $65,000.

Each agreement also provides for a cash payment equal to three times the avera ge annual cash

compensation of Mr. Masefield, Mr. Dietz or Mr. DeAngelo, as the case may be, during the most

recent five taxable years of the Company ending before the date of such termination (or during

such portion of such period as such person was employed by, or rendered services for, the

Company), less $1,000, in the event of the termination of employment of Mr. Masefield, Mr.

Dietz or Mr. DeAngelo, as the case may be, other than for cause or the voluntary termi nation of

employment by such person. In the event of the occurrence of certain change of control events

(as defined in such employment agreements) involving the Company without the approval of the

DISCLOSURES AND NOTICES§24.759

September 1992 24-413

Board of Directors, Mr. Masefield, Mr. Dietz or Mr. DeAngelo may terminate their respective

employment agreements with the Company during the one-year period following such change of

control events and such termination of employment shall entitle the terminating person to the

termination payment described above.

Copies of such employment agreements are filed as Exhibits 2,3 and 4 hereto and are

incorporated herein by reference.

§24.759 PROXY STATEMENTS:

STRATEGY & FORMS

24-414© 1992 Jefren Publishing

Company, Inc.

Item 4. The Solicitation or Recommendation.

(a) At a meeting held on October 5, 1988 (the “October 5 Meeting”), the Board of

Directors of the Company unanimously determined that the Offer is inadequate, excessively

conditional and not in the best interests of the Company and its stockholders. The Board of

Directors unanimously recommends that the Company’s stockholders reject the Offer and not

tender any of their Shares pursuant to the Offer.

The Board unanimously adopted resolutions at the October 5 Meeting rejecting the

Offeror’s request that the Board redeem the Rights and approve the Offer and subsequent

business combination of the Company and the Offeror (the “Merger”) for purposes of the

Delaware Takeover Statute (as hereinafter defined) and the supermajority voting require ments in

the Company’s certificate of incorporation. See Item 8. The Board has determined in t he exercise

of its fiduciary duty to take no action which would lessen the Company’s and the stockholde rs

protections against coercive and inadequate offers like the Offer.

The Company has received assurances from certain substantial holders of Shares (which

include members of the Board and executives of the Company) that such holders do not int end to

tender their Shares pursuant to the Offer. See Item 6. In view of all of the foregoing, the Boa rd

believes (i) the Rights Condition (as hereinafter defined) cannot be satisfied absent a judicial

determination that the Rights are inapplicable or invalid (See Item 8(b)), (ii) i t is highly

improbable that the Section 203 Condition (as hereinafter defined) will be satisfied absent the

Offeror acquiring at least 85% of the Common Stock (excluding Common Stock held by

directors who are also officers and certain employee stock plans) pursuant to the Offer or a

judicial determination that Section 203 of the Delaware General Corporation Law (t he

“Delaware Takeover Statute”) is unconstitutional or otherwise inapplicable (See Ite m 8(a)), and

(iii) it is highly improbable that the Supermajority Condition (as hereinafter de fined) will be

satisfied (See Item 8(c)). Although the Offeror reserves the right to waive, reduce or otherwi se

modify any of the many conditions to the Offer, the Offeror has slated that “there can be no

assurance that [it] will do so and [it] has not determined whether it would be willing to do so

under any circumstances.”

The forms of the letter to stockholders communicating the Board’s recommendation and the

press release announcing such recommendation are filed as Exhibits 5 and 6, respectively, hereto

and are incorporated herein by reference.

(b) The position of the Board that the Offer is inadequate, excessively conditional and not

in the best interests of the Company and its stockholders and the recommendation of the Board

that stockholders reject the Offer is based upon the Board’s careful consideration of a num ber of

factors viewed by it as being relevant to an evaluation of the Offer. In making its evaluation and

reaching its conclusion, the Board received and considered presentations from, and reviewed t he

Offer with, the Company’s senior management, Baring Brothers & Co., Inc., the Company’s

investment bankers (“Baring Brothers”), and Haythe & Curley, the Company’s legal counsel. In

reaching its conclusions, the Board did not assign particular weight to any specific factor or

determine that any specific factor was of overriding importance. Rather, the Board views its

conclusions and recommendation as being based on all the information presented to and

considered by it.

(c) In reaching its conclusions with respect to the Offer, the Board of Directors considered

a number of factors, including, but not limited to, the following:

1. The opinion expressed by Baring Brothers at the October 5 Meeting that the $9

per Share being offered as the consideration in the Offer is inadequate from a financial point

of view to the holders of Common Stock. In addition to Baring Brothers’ presentation to the

Board in support and explanation of that opinion, Baring Brothers provided the Board with a

written opinion to that effect, setting forth the matters considered and limitati ons on the

DISCLOSURES AND NOTICES§24.759

September 1992 24-415

review undertaken, a copy of which opinion is filed as Exhibit 7 hereto and is incorporated

herein by reference. Baring Brothers’ opinion is subject to a number of assumptions and is

based on projections and other information supplied by management as described in the

written opinion,. Stockholders should review carefully Baring Brothers’ written opinion.

2. The presentation made by senior management of the Company to the Board

concerning the Company’s historical, present and expected future financial and operating

results. In view of this presentation and based upon both (i) the Board’s familiarity with the

Company’s current business, financial condition and operations, the expected increased

needs of its customers, historic growth levels, the Company’s position in the contract

sterilization industry relative to its competitors, the markets in which

§24.759 PROXY STATEMENTS:

STRATEGY & FORMS

24-416© 1992 Jefren Publishing

Company, Inc.

the Company operates and general economic and stock market conditions and (ii) the

Board’s belief as to future levels of financial performance of the Company, the Board

unanimously concluded that the Offer does not reflect the long-term value of the Shares.

3. The fact that the terms of the Offer are so excessively conditional that there is

no assurance that the Offeror will purchase any Shares tendered pursuant to the Offer.

Among other things, the Board was concerned that:

(i) the Offer is conditioned upon there being available to the Offeror

sufficient funds on terms acceptable to the Offeror and the Parent to purchase all

outstanding Shares on a fully diluted basis and pay related expenses, but the Offeror

has only “commenced discussions with banks and other financing sources” and has

not obtained any commitments for financing and has not provided sufficient

assurances that it will be able to arrange financing or otherwise obtain the necessa ry

funds;

(ii) the Offer is also conditioned on a minimum of 2,204,757 Shares being

tendered and not withdrawn, such number representing approximately 53.3% of the

total presently outstanding Shares not already owned by the Offeror or its affiliates;

(iii) the Offer is also conditioned on the compliance with or the

inapplicability of the Delaware Takeover Statute, which the Board believes is likely

to be satisfied only if the Offeror holds at least 85% of the then outstanding shares of

Common Stock, as computed under Section 203, following its Offer (see Item 8(a));

(iv) the Offer is also conditioned upon the Offeror obtaining at least 80% of

the Company’s “voting securities” (as defined in Article FOURTEENTH of the

Company’s Certificate of Incorporation) following the Offer or obtaining the

approval of the Board for either the consummation of the Offer or a subsequent

business combination between the Company and the Offeror (the “Supermajority

Condition”) (see Item 8(c));

(v) the Offer is also conditioned on the Board redeeming the Rights (which

the Company’s stockholders received as a dividend and which entitle the holders

thereof, upon certain circumstances, to purchase shares of Common Stock at 50% of

market (see Item 8(b))) or otherwise having the Rights declared invalid or

inapplicable as they apply to the Offer by a court of competent jurisdiction (the

“Rights Condition”); and

(vi) the Offer also contains conditions requiring the absence of certain

circumstances concerning the Company, the satisfaction of which conditions will be

in the sole and subjective judgment of the Offeror; in certain cases (such as those

conditions relating to the covenants, terms and conditions of the Company’s or its

subsidiaries’ contractual obligations) the relevant circumstances were publicly

available prior to the commencement of the Offer, but the Offeror has not provided

any indication as to its subjective evaluation of those publicly known circumstances.

4. The fact that, even if the Offeror is able to and does purchase Shares tendered

pursuant to the Offer, the Offeror has not arranged, and may not be able to arrange, the

financing which would be required to purchase Shares then owned by any remaining

unaffiliated stockholders following the Offer. Furthermore, while the Offeror has stated

that it intends to propose to acquire the Shares of such remaining stockholders at the $9 per

Share offer price, it has no obligation to do so and has not provided the assurance that it

will actually seek to or be able to consummate any such transaction or that it will not

attempt to acquire the remaining Shares other than for cash and/or at a lower c onsideration

than provided in the Offer.

DISCLOSURES AND NOTICES§24.759

September 1992 24-417

5. The fact that the sales prices for the Shares as reported by the National

Association of Securities Dealers National Market System has not been below $9.50 per

share from the date of the Offer, September 23, 1988, through October 5, 1988.

6. The Company’s belief that the contingent liabilities of the Parent referred to in

the Parent’s financial statements for the years ended March 31, 1988 and 1987, coupled

with the Parent’s already substantial liabilities, including large long-term debt obl igations

(approximately 83% of the Parent’s long-term debt obligations are secured by various

letters of credit, which are each guaranteed by the majority shareholder of the Pare nt),

could require the Parent to effect some or all of the courses of action it has reserved for the

Company, namely, the sale of some of the Company’s assets and/or the depletion of the

Company’s cash reserves to repay the Parent’s financing source for file Offer, thereby

potentially having a material adverse effect on the ability of the Company to maintain its

current level of growth and to permit stockholders who do not tender their Shares pursuant

to the Offer to realize

§24.759 PROXY STATEMENTS:

STRATEGY & FORMS

24-418© 1992 Jefren Publishing

Company, Inc.

fully the inherent value in the Common Stock. Further, the Offeror may not be able to gra nt

“a security interest in the assets of the Company” in connection with the proposed Merge r

as it suggests without obtaining the consent of certain of the Company’s (and/or its

subsidiaries’) existing lenders or the repayment of certain of the Company’s outstanding

indebtedness.

7. The Company’s belief that the Offer may raise substantial and serious legal

questions, which the Company has instructed its counsel to review.

For information concerning certain other actions taken by the Board since the

announcement of the Offer, see Item 7.

Item 5. Persons Retained, Employed or to be Compensated.

In March 1988, the Company engaged Baring Brothers to provide financial advisory

services to the Company in connection with the Company’s acquisition program. In June 1988,

the Company also engaged Baring Brothers to serve as its financial advisor in connecti on with

proposals received for the acquisition of the Company. The engagement agreement provides for

the Company to pay Baring Brothers an initial retainer of $8,333.33 per month, which under the

terms of the agreement has been increased to $75,000 per month as a result of the Offer. In

addition, should the Company engage in certain acquisition transactions during the term of the

engagement or within 12 months thereafter, Baring Brothers is entitled to receive a fee based on

the consideration paid in the transaction as follows. Baring Brothers will receive a fee of 6% of

the consideration paid by another person to acquire an interest of less than 50% in the C ompany.

Baring Brothers will also receive a fee if the Company acquires a substantial interest in another

entity or a substantial portion of the stock or assets of the Company is acquired by another

person (other than an acquisition by another person of an interest in the Company of less than

50%) equal to the sum of 5% of the consideration paid up to $3 million, 3% of the consideration

paid in excess of $3 million but up to $6 million, and 1% of any excess over $6 million. The

Company has also agreed to reimburse Baring Brothers for its reasonable out-of-pocket expenses

and to indemnify and hold Baring Brothers harmless against certain liabilities.

The Company has retained Noonan/Russo Communications as a public relations advisor in

connection with the Offer and may retain an information agent to assist the Compa ny in

connection with its communications to its stockholders with respect to, and to provide other

services to the Company in connection with, the Offer. Such firms will receive rea sonable and

customary compensation for their services and reimbursement of out-of-pocket expenses in

connection therewith.

Neither the Company nor any person acting on its behalf currently intends to employ, reta in

or compensate any other person to make solicitations or recommendations to security holders on

its behalf concerning the Offer.

Item 6. Recent Transactions and Intent with Respeet to Securities.

(a) No transactions in the Shares have been effected during the past 60 days by the

Company or, to the best of the Company’s knowledge, by any executive officer, director,

affiliate or subsidiary of the Company.

(b) To the best of the Company’s knowledge, none of the Company’s executive officers,

directors, affiliates or subsidiaries currently intends to tender any Shares that are he ld of record

or beneficially owned by such persons pursuant to the Offer. The foregoing does not include any

Shares over which, or with respect to which, any such executive officer, director, affiliate or

subsidiary acts in a fiduciary or representative capacity or is subject to the instruct ions of some

third party in respect of such tender.

Item 7. Certain Negotiations and Transactions by the Subject Company.

DISCLOSURES AND NOTICES§24.759

September 1992 24-419

(a) Except as set forth in paragraph (b) below, no negotiation is being undertaken or is

under way by the Company in response to the Offer which relates to or would result in (i) a n

extraordinary transaction, such as a merger or reorganization, involving the Company or any

subsidiary thereof; (ii) a purchase, sale or transfer of a material amount of assets by the Company

or any subsidiary thereof; (iii) a tender offer for or other acquisition of securities by or of the

Company; or (iv) any material change in the present capitalization or dividend poli cy of the

Company.

(b) At a meeting of the Board held on September 28, 1988, the Board authorized and

directed management and Baring Brothers to explore various possible alternatives that would be

designed to maximize the value

§24.759 PROXY STATEMENTS:

STRATEGY & FORMS

24-420© 1992 Jefren Publishing

Company, Inc.

of the Shares, including, without limitation, possible sales of the Company’s capital stoc k to

third parties, possible repurchases of Shares, possible dividends to the Company’s stockholders

and possible acquisitions of one or more other companies. At that meeting, it was the c onsensus

of the Board that it was appropriate, in light of the Board’s ongoing evaluation of the Offer, for

Baring Brothers to have discussions with third parties with respect to such possible alternati ves.

There can be no assurance that any transaction will be recommended or consummated.

In order not to jeopardize the continuation of any discussions or negotiations that the

Company may conduct with respect to the transactions referred to above, the Board has adopt ed

a resolution directing the Company not to disclose the possible terms of any such transact ions, or

the parties thereto, unless and until an agreement in principle relating thereto has been reached.

Item 8. Additional Information to be Furnished.

(a) Delaware Takeover Statute. The Delaware Takeover Statute, 8 Del. C. §203, which

was signed into law on February 2, 1988, may have the effect of significantly delaying the

Offeror’s acquisition of the entire equity interest in the Company.

In general, the Delaware Takeover Statute prevents an “Interested Stockholder” (defined

generally as a person owning 15 percent or more of a corporation’s outstanding voting stock

other than any person who owned shares in excess of the 15 percent limitation or acquired suc h

shares pursuant to a tender offer commenced prior to December 23, 1987) from engaging in a

“Business Combination” (defined as a variety of transactions, including mergers, as set forth

below) with the Delaware corporation for three years following the date such person became an

Interested Stockholder unless: (i) before such person became an Interested Stockholder, the

board of directors of the corporation approved the transaction in which the Interested

Stockholder became an Interested Stockholder or approved the Business Combination; (ii) upon

consummation of the transaction which resulted ill the Interested Stockholder becoming an

Interested Stockholder, the Interested Stockholder owned at least 85 percent of the voting st ock

of the corporation outstanding at the time the transaction commenced (excluding stock he ld by

directors who are also officers and employee stock ownership plans in which employee

participants do not have the right to determine confidentially whether shares held subje ct to the

plan will be tendered in a tender or exchange offer); or (iii) following the transaction in which

such person became all Interested Stockholder, the Business Combination is (x) approved by the

board of directors of the corporation and (y) authorized at a meeting of stockholders by the

affirmative vote of the holders of two-thirds of the outstanding voting stock of the corporation

not owned by the Interested Stockholder.

Under the Delaware Takeover Statute, the restrictions described above do not apply if,

among other things, (i) the corporation’s original certificate of incorporation contains a provision

expressly electing not to be governed by the Delaware Takeover Statute, (ii) the corporat ion, by

action of its board of directors, adopted an amendment to its by-laws within 90 days of February

2, 1988, the effective date of the Delaware Takeover Statute, expressly electing not to be

governed by the Delaware Takeover Statute, which amendment may not be further amende d by

the board of directors (the Board did not adopt such a resolution), (iii) the corporation, by a ction

of its stockholders, adopts an amendment to its certificate of incorporation or by-laws expressl y

electing not to be governed by the Delaware Takeover Statute, provided that, in addi tion to any

other vote required by law, such amendment to the certificate of incorporation or by-laws must

be approved by the affirmative vote of a majority of the shares entitled to vote (such an

amendment would not be effective until 12 months after the adoption of such amendment and

would not apply to any Business Combination between the corporation and any person who

became an Interested Stockholder of the corporation on or prior to the date of such adoption),

(iv) the corporation does not have a class of voting stock that is (x) listed on a national securities

exchange, (y) authorized for quotation on an inter-dealer quotation system of a registered

national securities association or (z) held of record by more than 2,000 stockholders, unless any

DISCLOSURES AND NOTICES§24.759

September 1992 24-421

of the foregoing results from action taken, directly or indirectly, by an Interested Stockholder or

from a transaction in which a person becomes an Interested Stockholder, or (v) a stockholder

becomes an Interested Stockholder “inadvertently” and thereafter divests itself of a sufficient

number of shares so that such stockholder ceases to be an Interested Stockholder. The Dela ware

Takeover Statute would also not apply to certain Business Combinations proposed by an

Interested Stockholder following the announcement or notification of one of certain

extraordinary

§24.759 PROXY STATEMENTS:

STRATEGY & FORMS

24-422© 1992 Jefren Publishing

Company, Inc.

transactions involving the corporation and a person who had not been an Interested Stockholder

during the three years preceding the date of the Business Combination or who became a n

Interested Stockholder with the approval of a majority of the corporation’s board of directors.

The Delaware Takeover Statute provides that during such three-year period the corporation

may not merge or consolidate with an Interested Stockholder or any affiliate or associat e thereof,

and also may not engage in certain other transactions with an Interested Stockholder or any

affiliate or associate thereof, including, without limitation, (i) any sale, lea se, exchange,

mortgage, pledge, transfer or other disposition of assets (except proportionately as a stockholder

of the corporation) having an aggregate market value equal to 10 percent or more of the

aggregate market value of all assets of the corporation determined on a consolidate d basis or the

aggregate market value of all the outstanding stock of the corporation, (ii) any transact ion which

results in the issuance or transfer by the corporation or by certain subsidiaries thereof of any

stock of the corporation or of such subsidiaries to the Interested Stockholder, except pursuant to,

among other things, a transaction which effects a pro rata distribution to all stockholders of the

corporation, (iii) any transaction involving the corporation or certain subsidiaries thereof which

has the effect of increasing the proportionate share of the stock of any class or series, or

securities convertible into the stock of any class or series, of the corporation or any such

subsidiary which is owned directly or indirectly by the Interested Stockholder (except as a result

of immaterial changes due to fractional share adjustments or as a result of any purc hase or

redemption of any shares of stock not caused, directly or indirectly, by the Interested

Stockholder), or (iv) any receipt by the Interested Stockholder of the benefit (except

proportionately as a stockholder of such corporation) of any loans, advances, guarantees, pledges

or other financial benefits provided by or through the corporation.

Unless the Offeror acquires a sufficient number of Shares pursuant to the Offer to satisfy the

share percentage provision of the Delaware Takeover Statute or unless the provisions of clauses

(ii) or (iii) of the second preceding paragraph or clause (iii) of the third preceding pa ragraph are

complied with, the Offeror would be unable to effect the Merger for a period of three years a nd

would be prevented from engaging in certain transactions by the Delaware Takeover Statute.

If the Offeror acquires a sufficient number of Shares pursuant to the Offer to satisfy the 85

percent requirement of the Delaware Takeover Statute, the Offeror would be able to effect the

Merger without any application of the three-year waiting period. The Board believes tha t it is

highly improbable that the Offeror will be able to acquire such number of Shares in view of the

assurances received by the Company from certain substantial holders of Shares (which include

members of the Board and executives of the Company) that such holders do not intend to t ender

their Shares pursuant to the Offer. See Item 6.

(b) Rights Platt. On June 10, 1988, the Board unanimously adopted the Rights Plan and

declared a dividend distribution of one right (collectively, the “Rights”) for each outst anding

share of Common Stock, payable to stockholders of record at the close of business on June 21,

1988 (the “Record Date”). Except as set forth below, each Right, when exercisable, e ntitles the

registered holder to purchase from the Company one one-hundredth share of a new series of

preferred stock, designated as Series A Preferred Stock, $l.00 par value (the “Preferred Shares”),

at a price of $20 per one one-hundredth of a Preferred Share (the “Purchase Price”), subject to

adjustment.

The Rights Plan is designed to protect stockholders against unsolicited, coercive at tempts to

acquire control of the Company.

Until the Distribution Date (as defined in the Rights Plan), the Rights will be e videnced by

the certificates representing the Common Stock in respect of which the Rights a re issued and will

be transferred upon and only upon transfer of the related Common Stock, and no separate Rights

certificates will be distributed. As soon as practicable following the Distribution Date , separate

DISCLOSURES AND NOTICES§24.759

September 1992 24-423

certificates evidencing the Rights (“Rights Certificates”) will be mailed to holders of record of

the Common Stock as of the close of business on the Distribution Date, and the Rights

Certificates alone will then evidence the Rights and will be seoarately transferable.

The Rights are not exercisable until the Distribution Date. The Rights will expi re on the

earlier of (i) June 10, 1998 (unless extended), or (ii) redemption by the Company as described

below.

Under the terms of the Rights Plan, the Rights could be detached as early as Octobe r 7,

1988, as a result of the commencement of the Offer, At the October 5 meeting, the Boa rd

determined, in accordance with the

§24.759 PROXY STATEMENTS:

STRATEGY & FORMS

24-424© 1992 Jefren Publishing

Company, Inc.

Rights Plan, to defer the date on which the Rights are to be detached (the Distribution Date) until

October 13, 1988 (or such later date as may be determined by the Board).

In the event any Person (as defined in the Rights Plan) shall become an Acquiring Person

(defined in the Rights Plan to be a Person or group of affiliated Persons which acquires or

obtains the right to acquire beneficial ownership of 20% or more of the shares of Common

Stock), each holder of a Right (other than an Acquiring Person, whose Rights will become void)

shall thereafter have a right to receive, upon exercise thereof at a price equa l to the then current

Purchase Price multiplied by the number of one one-hundredths of a Preferred Share for which a

Right is then exercisable, in accordance with the terms of the Rights Plan and in lieu of Preferred

Shares, such number of shares of Common Stock as shall equal the result obtained by (x)

multiplying the then current Purchase Price by the number of one one-hundredths of a Preferred

Share for which a Right is then exercisable arid dividing that product by (y) 50% of the then

current per share market price of the Common Stock on the date such Person became an

Acquiring Person. In the event that any Person shall become an Acquiring Person and the Rights

shall then be outstanding, the Company shall not take any action which would elimina te or

diminish the benefits intended to be afforded by the Rights.

At any time after the acquisition by a person or group of affiliated or associated persons of

beneficial ownership of 20% or more of the outstanding shares of Common Stock, the Board of

Directors of the Company may exchange the Rights (other than Rights owned by such person or

group, which shall become void), in whole or in part, at an exchange ratio of one share of

Common Stock, or one one-hundredth of a Preferred Share (or of a share of a class or series of

the Company’s preferred stock having equivalent rights, preferences and privileges), per Right

(subject to adjustment).

In the event, directly or indirectly, (a) the Company shall consolidate with, or me rge with

and into, any other Person, (b) any Person shall consolidate with the Company, or merge with

and into the Company and the Company shall be the continuing or surviving corporation of such

merger and, in connection with such merger, all or part of the shares of Common Stock shall be

changed into or exchanged for stock or other securities of any other person (or the Company) or

cash or any other property, or (c) the Company shall sell or otherwise transfer (or one or more of

its subsidiaries shall sell or otherwise transfer), in one or more transactions, assets or earning

power aggregating 50% or more of the assets or earning power of the Company and its

subsidiaries (taken as a whole) to any other person other than the Company or one or more of i ts

wholly-owned subsidiaries, then, and in each such case, proper provision shall be made so that

(i) each holder of a Right (other than an Acquiring Person whose Rights will become void) shall

thereafter have the right to receive, upon the exercise thereof at a price equa l to the then current

Purchase Price multiplied by the number of one one-hundredths of a Preferred Share for which a

Right is then exercisable, in accordance with the terms of the Rights Plan and in lieu of Preferred

Shares, such number of shares of common stock of such other person (including the Company as

successor thereto or as the surviving corporation) as shall equal the result obtained by (A)

multiplying the then current Purchase Price by the number of one one-hundredths of a Preferred

Share for which a Right is then exercisable and dividing that product by (B) 50% of the then

current per share market price of common stock of such other person on the date of

consummation of such consolidation, merger, sale or transfer; (ii) the issuer of such shares of

common stock shall thereafter be liable for, and shall assume, by virtue of such consolidat ion,

merger, sale or transfer, all the obligations and duties of the Company pursuant to the Rights

Plan; (iii) the term “Company” shall thereafter be deemed to refer to suc h issuer; and (iv) such

issuer shall take such steps in connection with such consummation as may be necessary t o assure

that the provisions of the Rights Plan shall thereafter be applicable, as nearly as reasonably may

be, in relation to the common stock thereafter deliverable upon tire exercise of the Rights.

DISCLOSURES AND NOTICES§24.759

September 1992 24-425

At any time prior to the acquisition by a Person or group of affiliated or associated Persons

of beneficial ownership of 20% or more of the outstanding shares of Common Stock, the Board

of Directors of the Company may redeem the Rights in whole, but not in part, at a price of $.01

per Right (the “Redemption Price”). The redemption of the Rights may be made e ffective at such

time on such basis and with such conditions as the Board of Directors in its sole disc retion may

establish. In addition, if a bidder who does not beneficially own more than 1% of the shares of

Common Stock (and who has not within the past year owned in excess of 1% of the shares of

Common Stock and, at a time he held such greater than 1% stake, disclosed, or cause d the

disclosure of, an intention which relates to or would result in the acquisition or infl uence of

control of the Company) proposes to acquire all of the shares of Common Stock (and all othe r

shares of capital stock of the Company entitled to vote with the shares of Common Stock in the

election of directors or on mergers,

§24.759 PROXY STATEMENTS:

STRATEGY & FORMS

24-426© 1992 Jefren Publishing

Company, Inc.

consolidations, sales of all or substantially all of the Company’s assets, liquidations, dissol utions

or windings up) for cash at a price which a nationally recognized investment banker selec ted by

such bidder states ill writing is fair, and such bidder has obtained written financi ng commitments

(or otherwise has financing) and complies with certain procedural requirements, then the

Company, upon the request of the bidder, will hold a special stockholders’ meeting to vote on a

resolution requesting the Board of Directors to accept the bidder’s proposal. if a majority of the

outstanding shares entitled to vote on the proposal vote in favor of such resolution, then for a

period of 60 days after such meeting the Rights will be automatically redeemed a t the

Redemption Price immediately prior to the consummation of any tender offer for all of suc h

shares at a price per share in cash equal to or greater than the price offered by such bidder;

provided, however, that no redemption will be permitted or required after the acquisition by any

Person or group of affiliated or associated Persons of beneficial ownership of 20% or more of the

outstanding Shares. Immediately upon any redemption of the Rights, the right to exercise the

Rights will terminate and the only right of the holders of Rights will be to recei ve the

Redemption Price.

The terms of the Rights may be amended by the Board of Directors of the Company without

the consent of the holders of the Rights, including an amendment to lower the threshold for

exercisability of the Rights from 20% to not less than the greater of (i) any percent age greater

than the largest percentage of the outstanding shares of Common Stock then known to the

Company to be beneficially owned by any Person or group of affiliated or associated Persons

and (ii) 15%, except that from and after such time as any Persou becomes an Acquiring Person

no such amendment may adversely affect the interests of the holders of the Rights.

(c) Supermajority Provisions. Certain Articles of the Company’s Certificate of

Incorporation provide: (i) that certain business combinations involving the Company and any

beneficial owner of 20% or more of the outstanding voting securities of the Company be

approved by the holders of at least 80% of the Company’s voting securities, unless certain

conditions, including a minimum price requirement, are satisfied, or unless a majorit y of the

Continuing Directors (as defined in the Company’s Certificate of Incorporation) had waived suc h

conditions or had approved, prior to the time such person became a 20% beneficial owner, the

acquisition of such 20% beneficial ownership position or the proposed business combination, (ii)

that any action taken by the Company’s stockholders be taken at an annual or specia l meeting

held upon prior notice and pursuant to a vote (in addition, the Company’s By-laws contain a

provision the effect of which is to prohibit the stockholders of the Company from calling a

special meeting without the approval of the Board of Directors, thereby preventing stockhol ders,

without such approval, from initiating action other than at the Annual Meeting of St ockholders),

except that holders of any of the Company’s preferred stock may if authorized act by writ ten

consent under certain circumstances as provided in Article FOURTH of the Company’s

Certificate of Incorporation and (iii) the vote of not less than 80% of the Company’s outsta nding

voting securities is required to repeal, alter or amend the Company’s By-laws, any of the

provisions described above and the provisions in the Company’s Certificate of Incorporation

with respect to the division of the Board of Directors into classes. In view of these require ments,

the Board believes that it is highly improbable that the Offeror will be able to satisfy the

Supermajority Condition. See Item 6.

DISCLOSURES AND NOTICES§24.759

September 1992 24-427

Item 9. Material to be Filed as Exhibits.

1. —Pages 7 through 17 of the Proxy Statement.2. —Employment Agreement dated as of February 1, 1988 between the Company and John Masefield.

3. —Employment Agreement dated as of February 1, 1988 between the Company and George R. Dietz.

4. —Employment Agreement dated as of February 1, 1988 between the Company and Thomas J. DeAngelo.

5. —Form of Letter from the Chairman and Chief Executive Officer of the Company to the Company’s Stockholders.*

6. —Form of Press Release.

7. —Opinion of Baring Brothers & Co., Inc.* Included in mailing to all stockholders.