US Legal’s Survivor’s Guide to A Death in the Family

1

US LEGAL, INC.

US Legal’s Survivor’s

Guide to a Death in the

Family

Copyright © 2009 by US Legal, Inc.

Neal Walker, Staff Attorney

July 2009

�US Legal’s Survivor’s Guide to A Death in the Family

2

This guide discusses the practical as well as legal tasks that confront

survivors―primarily the decedent’s surviving spouse or domestic partner―upon the

death of a family member, with particular attention to the following matters:

1.

Obituary.

2.

Burial insurance.

3.

Funeral and burial rights, arrangements, and expenses.

a. Cremation services.

b. Scattering of ashes within National and National Military Parks.

c. Burial at sea.

4.

Anatomical and whole-body gifts.

5.

How Social Security can help when a family member dies.

6.

Essential information and documents needed by survivor.

7.

Example of probate information form.

8.

Support groups.

9.

Changing title to decedent’s motor vehicle.

10.

Access to decedent’s safe-deposit box.

11.

Non-probate distribution of sums on deposit with financial institutions to

decedent’s spouse or heirs.

12.

Homeowner’s or renter’s insurance.

13.

Vacant dwelling insurance.

14.

Decedent’s last will.

15.

Legal advice and probate proceedings.

16.

Fees received by personal representative.

17.

Personal representative and survivor’s responsibility for the income tax liability

of the decedent and the estate of decedent.

18.

Decedent’s income-tax returns (Form 1040).

19.

Income tax return of an estate (Form 1041).

�US Legal’s Survivor’s Guide to A Death in the Family

3

20.

Claiming a decedent’s income-tax refund (Form 1310).

21.

Claiming benefits under a life-insurance policy.

22.

Survivor’s eligibility for either rollover or distribution from a decedent’s

qualified retirement plan or IRA.

�US Legal’s Survivor’s Guide to A Death in the Family

4

1.

OBITUARY.

Both newspaper and online obituary notices are available. Newspaper’s policies vary,

with some publishing only obituaries written by the newspaper’s staff, and others

accepting submitted obituaries. An online search under “obituary” will reveal many

obituary websites. The Atlanta Journal-Constitution’s website is one example of the

many obituary information and services that are available online; please see:

http://www.ajc.com/info/content/services/info/obituaryhelp.html.

2.

BURIAL INSURANCE.

According to the Insurance Information Institute, “‘[b]urial insurance’ usually refers to

a whole life insurance policy with a death benefit of from $5,000 to $25,000.” Please see:

http://www.iii.org/individuals/life/special/burial/. Further information on burial and

other forms of insurance is available at: http://www.iii.org/insurance_topics/. Insurance

is a regulated industry. Each state has a Department of Insurance. A consumer can view

the website of any state’s Department of Insurance simply by typing the name of a state

followed by the phrase “department of insurance” in the search window of a web

browser. Each state’s Department of Insurance has consumer information available on

its website.

3.

FUNERAL AND BURIAL RIGHTS, ARRANGEMENTS, AND EXPENSES.

Burial rights and anatomical gifts are governed by the law of the state in which the

decedent resided or, if the decedent’s body is not returned to the decedent’s state of

residence, then of the state in which the body is present. An example of one state’s

burial and anatomical gift statute may be found online at the Oregon Legislature’s

website: http://www.leg.state.or.us/ors/097.html. The National Funeral Directors’

Association offers information about funerals to the public at:

http://www.nfda.org/index.php/public. An online search under “alternative funerals”

will reveal numerous local organizations throughout the United States that offer

alternative funeral arrangements including cremation. The United States Conference of

Catholic Bishops declares that the Roman Catholic Church prefers burial but permits

both cremation and burial at sea; please see:

http://www.usccb.org/liturgy/cremation.shtml. The American Association of Retired

�US Legal’s Survivor’s Guide to A Death in the Family

5

Persons (AARP) offers a summary of Preneed Funeral and Burial Agreements; please

see http://assets.aarp.org/rgcenter/consume/d17093_preneed.pdf. The states regulate the

funeral and burial business. Consumer information about funeral and burial expenses

as well as providers is available online from many sources, including by way of

example the following:

•

California Department of Consumer Affairs:

http://www.cfb.ca.gov/consumer/funeral.shtml.

•

Connecticut Care Planning Council ― Funeral and Burial Preplanning:

http://www.careconnecticut.org/list22_ct_Funeral_Burial_Pre-Planning_PreNeed.htm.

•

Florida Attorney General:

http://myfloridalegal.com/pages.nsf/main/fe6c72fa035a16bc85256cc900514e6a!Open

Document.

•

Georgia Secretary of State: http://sos.georgia.gov/Securities/ceminfo.htm.

•

Maryland Division of Occupational and Professional Licensing:

http://www.dllr.state.md.us/license/cem/consumertips.htm.

•

Michigan Department of Human Services:

http://www.ftc.gov/bcp/edu/pubs/consumer/products/pro19.shtm.

•

New York State Department of Health:

http://www.health.state.ny.us/professionals/patients/patient_rights/funeral.htm.

•

Oregon Department of Finance (Prearranged Funeral Plans):

http://dfcs.oregon.gov/preneed.html.

•

Texas Funeral Service Commission: http://www.tfsc.state.tx.us/.

•

U.S. Federal Trade Commission:

http://www.ftc.gov/bcp/edu/pubs/consumer/products/pro19.shtm.

•

Wisconsin Department of Health Services ― Funeral and Cemetery Aids Program:

http://dhs.wisconsin.gov/em/WFCAP/index.htm.

a. Cremation Services.

Information about cremation services and providers is available online; see, for

example: http://www.cremation.com/;

�US Legal’s Survivor’s Guide to A Death in the Family

6

http://www.thefuneraldirectory.com/cremationfaq.html; and

http://www.cremationassociation.org/html/for_consumers.html.

b. Scattering of Ashes within National Parks and National Military Parks.

As a general rule, National Parks allow the scattering of ashes within the boundaries of

a national park, but require application and a special use permit to do so. The scope of

authorization and the procedures vary from park-to-park. Interested persons should

first learn the rules, the information is available online, then follow the procedures and

rules applicable to the chosen park. Examples of online information currently available

include: Mount Rainer NP http://www.nps.gov/mora/planyourvisit/upload/AshesForm-3.pdf; Grand Teton NP http://www.nps.gov/grte/planyourvisit/permits.htm; Yosemite NP http://www.nps.gov/yose/planyourvisit/ashes.htm; Shenandoah NP http://www.nps.gov/shen/planyourvisit/permits.htm; Fredericksburg and Spotsylvania

Battlefields NMP - http://www.nps.gov/frsp/parkmgmt/lawsandpolicies.htm.

c. Burial at Sea.

The United States Navy Mortuary Affairs Department offers burial at sea for Navy and

Marine veterans and their family members. For general information see: U.S. Navy ―

Burial at Sea: http://www.history.navy.mil/faqs/faq85-1.htm. For eligibility

requirements and instructions, please see:

http://www.navy.mil/navydata/questions/burial.html, or call toll-free 1-866-787-0081

and follow the voice menu.

4.

ANATOMICAL AND WHOLE-BODY GIFTS.

The full text of the Revised Uniform Anatomical Gift Act (2006) may be found online at

http://www.anatomicalgiftact.org/DesktopDefault.aspx?tabindex=1&tabid=63.

Information about anatomical and whole-body gifts is available online; by way of

example, please see: http://www.anatomicgift.com/;

http://dms.dartmouth.edu/anatomy/gifts/; http://www.biogift.org/;

http://dhs.wisconsin.gov/rl_dsl/Publications/09-010.htm; and

http://medschool.duke.edu/modules/som_anat_gft_pgm/index.php?id=1. Anatomical

gift forms that are valid for each state are available at the US Legal Forms website:

http://www.uslegalforms.com/powerofattorney/anatomicalgifts/.

�US Legal’s Survivor’s Guide to A Death in the Family

7

5.

HOW SOCIAL SECURITY CAN HELP WHEN A FAMILY MEMBER DIES.

Social Security should be notified as soon as possible when a person dies. In most cases,

the funeral director will report the person's death to Social Security. You will need to

furnish the funeral director with the deceased's Social Security number so he or she can

make the report.

Some of the deceased's family members may be able to receive Social Security benefits if

the deceased person worked long enough under Social Security to qualify for benefits.

You should get in touch with Social Security as soon as you can to ensure the family

receives all of the benefits to which it may be entitled. Please read the following

information carefully to learn what benefits may be available.

One-Time Payment. A one-time payment of $255 can be paid to the surviving spouse if

he or she was living with the deceased; or, if living apart, was receiving certain Social

Security benefits on the deceased's record. If there is no surviving spouse, the payment

is made to a child who is eligible for benefits on the deceased's record in the month of

death.

Monthly Benefits. Certain family members may be eligible to receive monthly benefits,

including:

A widow or widower age 60 or older (age 50 or older if disabled);

A surviving spouse at any age who is caring for the deceased's child under age

16 or disabled;

An unmarried child of the deceased who is:

Younger than age 18 (or age 18 or 19 if he or she is a full-time student in

an elementary or secondary school); or

Age 18 or older with a disability that began before age 22;

Parents, age 62 or older, who were dependent on the deceased for at least half of

their support; and

A surviving divorced spouse, under certain circumstances.

MANDATORY RETURN OF BENEFIT. If the deceased was receiving Social Security

benefits, you must return the benefit received for the month of death or any later

months. For example, if the person dies in July, you must return the benefit paid

�US Legal’s Survivor’s Guide to A Death in the Family

8

in August. If benefits were paid by direct deposit, contact the bank or other

financial institution. Request that any funds received for the month of death or

later be returned to Social Security. If the benefits were paid by check, do not

cash any checks received for the month in which the person dies or later. Return

the checks to Social Security as soon as possible.

However, eligible family members may be able to receive death benefits for the month

in which the beneficiary died.

Contacting Social Security. The Social Security website is a valuable resource for

information about all of Social Security's programs. There are a number of things you

can do online at: http://www.ssa.gov/.

In addition to using the Social Security website, you can call the Social Security

Administration toll-free at 1-800-772-1213. The Social Security Administration can

answer specific questions from 7 a.m. to 7 p.m., Monday through Friday. It can provide

information by automated phone service 24 hours a day. (You can use the automated

response system to tell it a new address or request a replacement Medicare card.) If you

are deaf or hard of hearing, you may call the TTY number, 1-800-325-0778.

The Social Security Administration treats all calls confidentially to ensure that you

receive accurate and courteous service. That is why a second Social Security

representative monitors some telephone calls.

Additional information about the Social Security Administration’s survivor’s benefits

program is available at http://www.ssa.gov/pgm/links_survivor.htm.

ESSENTIAL INFORMATION AND DOCUMENTS NEEDED BY SURVIVOR.

6.

The descendant’s widow, widower, or other survivor might need other documents or

information, but at a minimum, the survivor will need the following information and

documents:

•

Decedent’s Social Security number.

•

Certified copies of the decedent’s death certificate.

•

Marriage certificates, if any; divorce decrees, if any.

•

Original life-insurance policies.

•

Decedent’s original last will.

�US Legal’s Survivor’s Guide to A Death in the Family

9

7.

•

If Decedent’s original last will is lost or unavailable (perhaps believed to be in safe

deposit box), then copy of decedent’s last will.

•

Safe-deposit box institution, number, and key. If no key is available, the institution

probably will charge a fee to drill the box and remove the existing lock.

•

Bank and brokerage account information (name of institution, account numbers,

account balances, names of any pay-on-death (POD) beneficiaries of decedent’s bank

accounts, and names of any transfer-on-death (TOD) beneficiaries of decedent’s

brokerage accounts.

•

IRA, 401(k) plan, 403(b) plan, and any annuity information (name of custodian,

account numbers, account balances, names of designated beneficiaries).

•

Names and addresses of decedent’s devisees (the persons to whom decedent devised

property in decedent’s last will).

•

Names and addresses of decedents heirs (decedent’s spouse, descendents, siblings,

parents (if alive), and grandparents (if alive).

•

Names and addresses of any persons with whom the decedent held title to property,

real or personal, with others, whether as joint tenants, tenants-in-common, or copartners.

•

Names and addresses of any persons with whom decedent engaged in any closelyheld business, whether as partner, shareholder, or member.

•

Names, addresses, account numbers, and account balances of decedent’s creditors

(including any unpaid health-care providers).

•

Name of decedent’s lawyers.

•

Name of decedent’s tax preparer.

EXAMPLE OF PROBATE INFORMATION FORM (The Form Illustrates the

Kind of Information Required of an Executor of a Decedent’s Estate):

A. PROBATE INFORMATION FORM

Decedent's full name [ ] Married [ ] Single [ ] Divorced [ ] Widowed

Decedent's Residence address at death (street, city, state)

Decedent’s Date of birth Date and place of death

Proof of death: [ ] Death certificate [ ] Obituary [ ] Other (specify)

�US Legal’s Survivor’s Guide to A Death in the Family

10

The decedent died: [ ] with a will [ ] without a will. Date of will (and

codicils)

Requested action: appointment of [ ] administrator [ ] executor [ ]

curator [ ] probate of will

Name of person making request

Mailing address

Basis for request: [ ] executor named in will [ ] sole distributee [ ]

other distributee [ ] creditor

Name of person seeking appointment

Day telephone Night telephone

Residence address

Mailing address, if different

Name of any additional person seeking appointment

Day telephone Night telephone

Residence address

Mailing address, if different

Name of assisting attorney, if any Telephone

Attorney's mailing address

The total value of the decedent's real and personal estate [ ] did [ ]

did not exceed $15,000 on the date of death.

I hereby certify that to the best of my knowledge and belief this is

an accurate statement of facts, and I acknowledge a continuing

legal duty to report any later discovered errors or inconsistencies to

the Clerk of the Court.

B. INFORMATION TO BE FURNISHED BY EACH PERSON SEEKING

APPOINTMENT

Are you a person under a disability? [ ] yes [ ] no.

Have you ever been convicted of a felony? [ ] yes [ ] no.

Have you ever filed for bankruptcy? [ ] yes [ ] no.

�US Legal’s Survivor’s Guide to A Death in the Family

11

Are you now, or have you ever been, an attorney at law in Virginia

or elsewhere? [ ] yes [ ] no.

I (we) hereby certify that to the best of my (our) knowledge and

belief this is an accurate statement of facts, and I (we)

acknowledge a continuing duty to report any later discovered

errors or inconsistencies to the Clerk of Court.

8. SUPPORT GROUPS.

Many grief and bereavement support groups maintain websites, examples of which are as

follows:

•

Alive Alone - http://www.alivealone.org/.

A support group for the education of bereaved parents, whose only child or

all children are deceased.

•

Child Suicide - http://childsuicide.homestead.com.

•

The Compassionate Friends - http://www.compassionatefriends.org/.

A national self-help support organization, which assists families in the positive

resolution of grief following the death of a child, and provides information to

help others be supportive.

•

Gift from Within - PTSD Resources for Survivors and Caregivers:

http://www.giftfromwithin.org/html/groups.html#groups.

•

Griefshare: Grief Recovery Support Groups - http://www.griefshare.org.

Features resources to assist and encourage people grieving the death of a

friend or family member, and includes database of more than 1200 listings of

support groups.

•

Helping All Loved Ones Survive, Inc - http://www.halos.org.

HALOS is a nonprofit organization that provides information, emotional

support, and referrals to surviving friends and family members of homicide

victims.

•

Military.com: http://www.military.com/benefits/survivor-benefits/tragedyassistance-program-for-survivors.

•

National Donor Family Council - http://www.donorfamily.org. National

organization for families whose loved ones have donated organs or tissues

upon death. Includes grief resources, message board, pen pals, newsletter.

Free membership.

•

National Resource Directory – An Online Partnership for Wounded, Ill, and

Injured Service Members, Veterans, their Families, and those Who Support

Them:

�US Legal’s Survivor’s Guide to A Death in the Family

12

https://www.nationalresourcedirectory.org/nrd/public/DisplayPage.do?pare

ntFolderId=6645.

•

Survivors of Suicide: http://www.survivorsofsuicide.com/.

•

Suicide Survivor Support Group:

http://www.yellowribbon.org/SurvivorSupportGroups.html.

•

TAPS - Tragedy Assistance Programs for Survivors: http://www.taps.org/. A

national non-profit organization providing services to all those who have lost

a loved one on active duty with the Armed Forces. Offers a survivor peer

support network. Grief counseling referral and case worker assistance and

crisis information.

•

Twinless Twins - http://www.twinlesstwins.org/. A support group for twins and

other multiples that have experienced the death of their twin.

•

Widows Too Young - http://www.widowstooyoung.com.

A support group for young widows and widowers, to help them start life

again.

9.

CHANGING TITLE TO DECEDENT’S MOTOR VEHICLE.

Many states have adopted a statute that authorizes transfer of title to a motor vehicle

titled in the name of a decedent solely upon the records of the agency charged with

licensing vehicles in that state. The requirements and procedure for such a transfer of

title in New Jersey are online at:

http://www.state.nj.us/mvc/Vehicle/TransferringVehicle.htm. For Nebraska residents,

online information regarding transfer of title to a decedent’s vehicle, ATV, or boat is

available at: http://www.dmv.ne.gov/dvr/mvtitles/transdecednt.html.

10.

ACCESS TO DECEDENT’S SAFETY-DEPOSIT BOX.

Access to safe-deposit boxes is discussed at http://www.foreignborn.com/selfhelp/banking/10-sd_boxes.htm. As a general rule, only the owner/renter or a person

authorized by the owner/renter upon the bank’s records may access a safe-deposit box.

Upon the death of a decedent who has rented a box in his or her sole name and who has

not granted access privileges to anyone else, a bank as a general rule will open the box

only upon a court order. If the original of the decedent’s last will is in the safe-deposit

box, then to gain access to the box, an heir of the decedent may have to initiate a

proceeding for administration of an intestate estate, or alternatively, attempt proof a

lost will, and then ultimately obtain either an order of administration of an intestate

�US Legal’s Survivor’s Guide to A Death in the Family

13

estate or letters testamentary upon proof of a lost will in order to gain access to the safedeposit box. In the event the box contains the original will of the decedent, and it is the

decedent’s last will, the probate proceeding then might need to be modified and all

interested persons might need to be re-notified of the existence of the original will.

11.

NON-PROBATE DISTRIBUTION OF SUMS ON DEPOSIT WITH

FINANCIAL INSTITUTIONS TO DECEDENT’S SPOUSE OR HEIRS.

Many states have adopted a statute, typically located in the state’s banking code, that

authorizes distribution upon written statement or affidavit of the depositor’s heirs or

devisees of a sum on deposit in bank accounts when the sum on deposit is less than the

amount stated in the statute. Georgia, for example, authorizes such a distribution when

the amount on deposit is less than $10,000 and the depositor dies intestate (that is,

without a valid will). Georgia Code § 7-1-239.

12.

HOMEOWNER’S OR RENTER’S INSURANCE.

The survivor should examine the decedent’s homeowner’s or renter’s insurance policy.

For information regarding such insurance, please see the website of the Insurance

Information Institute, at:

http://www.iii.org/individuals/HomeownersandRentersInsurance/. Typically the

homeowner’s or renter’s policy excludes coverage for a vacant dwelling.

13.

VACANT DWELLING INSURANCE.

Not all property and casualty insurers offer vacant dwelling insurance. Those that offer

it generally offer it for periods of 3, 6, or 12 months. For information about it, please see

the following websites for examples of companies or agencies that offer it and the

conditions of coverage.

• Foremost Insurance Group - http://www.foremost.com/products/vacanthome/index.htm;

• Shelly, Middlebrooks O’Leary, Inc. - http://www.shellyins.com/vacant-dwellinginsurance.php;

• Southern Cross Underwriters http://www.universalspecialty.com/prod_vacant_dwellings.html;

�US Legal’s Survivor’s Guide to A Death in the Family

14

• Thum Insurance http://www.thuminsurance.com/content.aspx?sectionid=2&contentid=84.

14.

DECEDENT’S LAST WILL.

The decedent’s last will is a very significant document: it contains the decedent’s final

statement before witnesses of how he or she wishes to dispose of his or her remaining

property. The decedent may have made other legal arrangements for the disposition of

particular kinds of property, such as a pay-on-death (POD) designation for a bank

account, or a transfer-on-death (TOD) designation for brokerage accounts. If so, then

those designations―and not the decedent’s will―control the disposition of those assets.

Bear in mind that any contractual or gratuitous disposition of property previously made

by the decedent has legal priority over the decedent’s dispositive scheme as expressed

in the will. The dispositive scheme expressed in the decedent’s last will only controls

property not otherwise legally disposed of by the decedent.

That said, the decedent’s last will remains a significant document in every estate. If any

prior disposition of property fails ― for instance, if the decedent lacked capacity at the

time of the prior transaction ― then the will controls the disposition of that property.

Many states have laws that require any person in possession of a decedent’s will to

deliver it over upon the decedent’s death either to the person nominated as personal

representative in the will or to any person appointed by a court of competent

jurisdiction as the personal representative of the decedent’s estate.

No person other than the maker of a will has legal authority to destroy or conceal a will.

15.

LEGAL ADVICE AND PROBATE PROCEEDINGS.

A decedent’s survivor always needs legal advice, and generally the sooner the better,

because property rights exist in a legal landscape. Probate law is fundamentally about

property rights, titles, and interests. Probate is the legal post-mortem (which simply

means after death) process by which a court-appointed personal representative acting

independently of the court but under court supervision and ultimately accountable to

the court administers the decedent’s estate.

Personal Representative’s Duties. The duties of a personal representative are to collect

all the decedent’s assets, pay the creditors, and distribute the remaining assets to the

�US Legal’s Survivor’s Guide to A Death in the Family

15

decedent’s devisees or heirs. The personal representative must also perform the

following duties:

•

Apply for an employer identification number (EIN) for the estate.

•

File both the decedent’s income-tax return and the estate’s income-tax return

when due.

•

Pay the tax determined up to the date of discharge from duties.

Probate terminology.

•

Testate means to die with a valid will; intestate means to die without a valid will.

•

Devisee is a person who takes under a decedent’s will. Heir is a person who

takes under a state’s law of intestate succession.

•

Personal representative is the person in charge of an estate. Personal

representative is the official term in many states; other states retain the older

terms executor (or executrix) for testate estates, and administrator (or

adminstratrix) for intestate estates. The IRS uses the term personal representative

to mean anyone who is in charge of the decedent’s property.

Employer Identification Number (EIN). The first action a personal representative

should take is to apply to the IRS for an EIN. You should apply for this number as soon

as possible because you need to enter it on returns, statements, and other documents

that you file concerning the estate. You also must give the number to payers of interest

and dividends and other payers who must file a return concerning the estate. You can

get an EIN by applying online at www.irs.gov/businesses, or by calling 1-800-829-4933,

Monday through Friday. Generally, if you apply online, you will receive your EIN

immediately upon completing the application. You can also apply using Form SS-4,

Application for Employer Identification Number. Generally, if you apply by mail, it

takes about 4 weeks to get your EIN.

Forms 1099. Payers of interest and dividends report amounts to the IRS on Form 1099

using the identification number of the person to whom the account is payable. After a

decedent’s death, the Forms 1099 must reflect the identification number of the estate or

beneficiary to whom the amounts are payable. The personal representative handling the

estate must furnish the this identification number to the payer.

�US Legal’s Survivor’s Guide to A Death in the Family

16

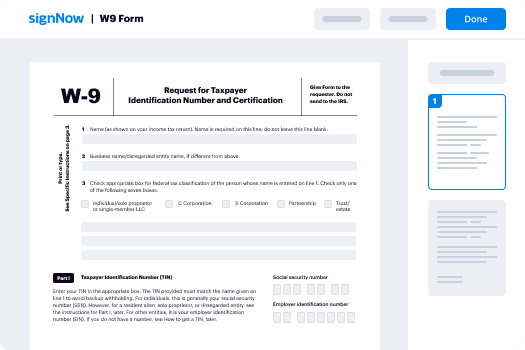

Form W-9. If the estate or a survivor may receive interest or dividends after being

informed of the decedent’s death, the payer should give the personal representative (or

the survivor) a Form W-9, Request for Taxpayer Identification Number and

Certification (or a similar substitute form). Complete this form to inform the payer of

the estate’s (or if completed by the survivor, the survivor’s) identification number and

return it to the payer.

Insolvent Estate. A decedent’s estate might be insolvent, that is, it’s assets might be

insufficient to pay all the decedent’s debts. In that event, the debts due the United States

must be paid first. Both the decedent’s federal income tax liabilities at the time of death

and the estate’s income tax liability are debts due the United States. See IRS Publication

559 – Survivors, Executors, and Administrators, p. 3: http://www.irs.gov/pub/irspdf/p559.pdf.

Spouse’s Elective Share. A spouse under the laws of the state in which the married

couple resided frequently has a statutory right to an elective share of a testate

decedent’s estate, when the decedent’s will gives the spouse a lesser amount than the

amount of the statutory elective share. The elective share amount generally is stated as a

percentage of the decedent’s estate. For examples of elective share statutes, see:

https://www.oregonlaws.org/ors/114.105.html - Oregon;

http://delcode.delaware.gov/title12/c009/index.shtml - Delaware; and

http://law.justia.com/alabama/codes/30792/43-8-70.html - Alabama.

16.

FEES RECEIVED BY PERSONAL REPRESENTATIVES.

All personal representatives must include in their gross income fees paid to them from

an estate. If paid to a professional executor or administrator, self-employment tax also

applies to such fees. For a non-professional executor or administrator (a person serving

in such capacity in an isolated instance, such as a friend or relative of the decedent),

self-employment tax only applies if a trade or business is included in the estate’s assets,

the executor actively participates in the business, and the fees are related to operation of

the business.

17.

PERSONAL REPRESENTATIVE AND SURVIVOR’S RESPONSIBILITY FOR

THE INCOME-TAX LIABILITY OF THE DECEDENT AND THE ESTATE OF

DECEDENT.

�US Legal’s Survivor’s Guide to A Death in the Family

17

All persons interested or involved in a decedent’s estate should be aware of the federal

tax laws regarding the final income-tax return of a decedent, as well as the potential

liability to the IRS of those who exercise custody or control of the decedent’s assets.

18.

DECEDENT’S INCOME-TAX RETURNS (Form 1040).

Final Income-Tax Return. The personal representative must file the final income tax

return (Form 1040) of the decedent for the year of death and any returns not filed for

preceding years. A surviving spouse, under certain circumstances, may have to file the

returns for the decedent.

Returns for Preceding Years. If an individual died after the close of the tax year, but

before the return for that year was filed, the return for the year just closed will not be

the final return. The return for that year will be a regular return and the personal

representative must file it.

Joint Return. Generally, the personal representative and the surviving spouse can file a

joint return for the decedent and the surviving spouse. However, the surviving spouse

alone can file the joint return if no personal representative has been appointed before

the due date for filing the final joint return for the year of death. A surviving spouse

who files a joint return for the year of death may qualify for special tax rates for the

following 2 years.

Qualifying Widows and Widowers. If the decedent died within the 2 years preceding

the year for which the widow or widower’s return is being filed, the widow(er) may be

eligible to claim the filing status of qualifying widow(er) with dependent child can

qualify to use the married-filing-jointly tax rates.

Surviving Spouse’s Remarriage. A final joint return with the decedent cannot be filed if

the surviving spouse remarried before the end of the year of the decedent’s death. The

filing status of the decedent in this instance is married filing a separate return.

19.

INCOME TAX RETURN OF AN ESTATE (Form 1041).

An estate is a taxable entity. An estate is a taxable entity, separate and apart from the

decedent and comes into being with the death of the individual. It exists until the final

distribution of its assets to the heirs and other beneficiaries. The income earned by the

assets during this period must be reported to the IRS by the estate under the conditions

�US Legal’s Survivor’s Guide to A Death in the Family

18

described in IRS Publication 559. The tax generally is figured in the same manner and

on the same basis as for individuals. The estate’s income, like an individual’s income,

must be reported annually on either a calendar or fiscal year basis. The personal

representative chooses the estate’s accounting period when filing its first Form 1041.

The estate’s first tax year can be any period that ends on the last day of a month and

does not exceed 12 months.

Filing Requirements. Every domestic estate with gross income of $600 or more during

a tax year must file a Form 1041. If one or more of the beneficiaries of the domestic

estate are nonresident alien individuals, the personal representative must file Form

1041, even if the gross income of the estate is less than $600.

IRS Publication 559. A survivor who wishes to know the income tax duties and

liabilities of a personal representatives should download and study IRS Publication 559,

entitled “Survivors, Executors, and Administrators”: http://www.irs.gov/pub/irspdf/p559.pdf.

20.

CLAIMING A DECEDENT’S INCOME-TAX REFUND (Form 1310).

A return should be filed to obtain a refund if tax was withheld from salaries, wages,

pensions, or annuities, or if estimated tax was paid, even if a return is not required to be

filed. Also, the decedent may be entitled to other credits that result in a refund.

Generally, a person who is filing a return for a decedent and claiming a refund must file

Form 1310 with the return. However, if the person claiming the refund is a surviving

spouse filing a joint return with the defendant, or a court-appointed or certified

personal representative filing an original return for the decedent, Form 1310 is not

needed. The personal representative must attach to the return a copy of the court

certificate showing that he or she was appointed the personal representative. For

additional information on claiming a refund, see IRS Publication 559, Survivors,

Executors, and Administrators, p.4, at: http://www.irs.gov/pub/irs-pdf/p559.pdf.

21.

CLAIMING BENEFITS UNDER A LIFE-INSURANCE POLICY.

How-to-Claim Death Benefits. For information on how to claim death benefits upon a

policy of life insurance see: “Filing a Life-Insurance Claim”:

http://www.acli.com/ACLI/Consumers/Life+Insurance/Filing+a+Claim/; and “How to

File Life-Insurance Claims”: http://www.quickquote.com/lifilehow.html.

�US Legal’s Survivor’s Guide to A Death in the Family

19

For Taxable Estates Only. Claimants of decedent’s whose estate’s are taxable under

either the United States Estate Tax or Generation-Skipping Transfer Tax should ask the

insurance company to complete and deliver to the executor of the decedent’s estate an

IRS Form 712 contemporaneously with any distribution to a beneficiary under the

policy. The executor of the decedent’s estate must submit a completed and executed

Form 712 with the Form 706, the United States Estate Tax or Generation-Skipping

Transfer Tax return.

VA Policies. To file a claim for benefits under a Veterans’ Administration life-insurance

policy, see: http://www.insurance.va.gov/inForceGliSite/claims/deathClaims.htm.

22.

SURVIVOR’S ELIGIBILITY FOR EITHER ROLLOVER OR DISTRIBUTION

FROM A DECEDENT’S QUALIFIED RETIREMENT PLAN OR IRA.

Discussion of the rules regarding rollover or distributions from a decedent’s qualified

retirement plan or individual retirement account is beyond the scope of this guide. Any

survivor of a decedent who participated in a plan or IRA should seek information from

the plan administrator or the IRA custodian. Survivors who desire information may

download several relevant publications, as well as forms, from the Internal Revenue

Service at its publications website:

http://www.irs.gov/formspubs/article/0,,id=99248,00.html; or its general website:

http://www.irs.gov/.

IRS Publications:

General Rules for Pensions and Annuities (IRS Publication 939):

http://www.irs.gov/pub/irs-pdf/p939.pdf.

Individual Retirement Arrangements (IRS Publication 590):

http://www.irs.gov/pub/irs-pdf/p590.pdf.

Pension and Annuity Income (IRS Publication 575):

http://www.irs.gov/pub/irs-pdf/p575.pdf.

Tax Guide to U.S. Civil Service Retirement Benefits (IRS Publication 721):

http://www.irs.gov/pub/irs-pdf/p721.pdf.

Tax-Sheltered Annuity Plans (403(B) Plans) (IRS Publication 571):

http://www.irs.gov/pub/irs-pdf/p571.pdf.

�US Legal’s Survivor’s Guide to A Death in the Family

20

�