Firma Acuerdo De Cobertura Fácil

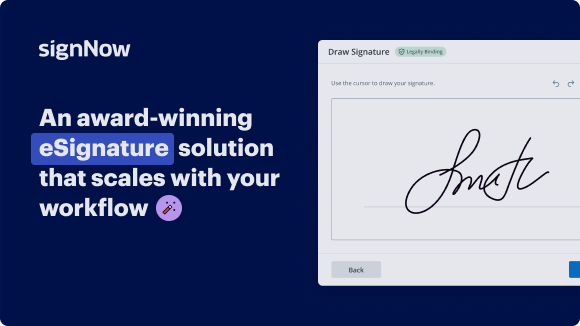

Solución de firma electrónica galardonada

Mejora tu flujo de trabajo de documentos con airSlate SignNow

Flujos de firma electrónica versátiles

Visibilidad rápida del estado del documento

Configuración de integración fácil y rápida

Firma acuerdo de cobertura en cualquier dispositivo

Registro de auditoría avanzado

Requisitos de seguridad rigurosos

Vea las firmas electrónicas de airSlate SignNow en acción

Soluciones de airSlate SignNow para una mayor eficiencia

Las reseñas de nuestros usuarios hablan por sí mismas

Por qué elegir airSlate SignNow

-

Prueba gratuita de 7 días. Elige el plan que necesitas y pruébalo sin riesgos.

-

Precios honestos para planes completos. airSlate SignNow ofrece planes de suscripción sin cargos adicionales ni tarifas ocultas al renovar.

-

Seguridad de nivel empresarial. airSlate SignNow te ayuda a cumplir con los estándares de seguridad globales.

Tu guía paso a paso — sign hedging agreement

Usando la firma electrónica de airSlate SignNow, cualquier organización puede mejorar los flujos de firma y firmar en línea en tiempo real, brindando una mejor experiencia a clientes y empleados. Usa firma del Acuerdo de Cobertura en unos pocos pasos sencillos. Nuestras aplicaciones móviles portátiles hacen posible trabajar en movimiento, incluso sin conexión! firma electrónica desde cualquier lugar del mundo y realiza tareas en poco tiempo.

Sigue las instrucciones paso a paso para usar firma del Acuerdo de Cobertura:

- Inicia sesión en tu perfil de airSlate SignNow.

- Encuentra tu documento en tus carpetas o sube uno nuevo.

- Accede a la plantilla ajustando usando el menú Herramientas.

- Arrastra y suelta campos rellenables, añade texto y firma electrónicamente.

- Añade varios firmantes mediante correos electrónicos y configura el orden de firma.

- Indica qué usuarios pueden recibir un documento firmado.

- Utiliza Opciones avanzadas para reducir el acceso al registro y establecer una fecha de vencimiento.

- Presiona Guardar y Cerrar cuando termines.

Además, hay funciones más extendidas disponibles para firma del Acuerdo de Cobertura. Incluye usuarios en tu espacio de trabajo colaborativo, navega por los equipos y monitorea la colaboración. Millones de usuarios en EE. UU. y Europa concuerdan en que un sistema que une a las personas en un área de trabajo cohesiva, es lo que las empresas necesitan para mantener los flujos de trabajo funcionando sin problemas. La API REST de airSlate SignNow te permite integrar firmas electrónicas en tu aplicación, sitio web, CRM o nube. Prueba airSlate SignNow y obtén flujos de firma electrónica más rápidos, suaves y en general más productivos!

Cómo funciona

Funciones de airSlate SignNow que los usuarios adoran

Vea resultados excepcionales firma Acuerdo de Cobertura fácil

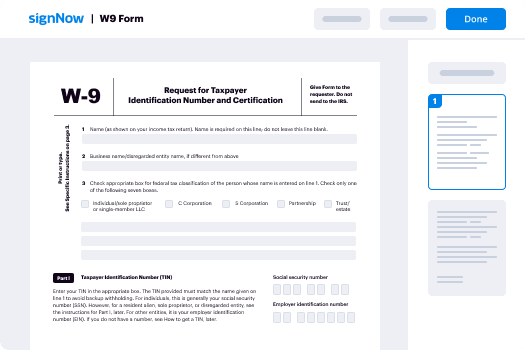

Cómo completar y firmar un documento en línea

Prueba la forma más rápida de firmar el Acuerdo de Cobertura. Evita flujos de trabajo en papel y gestiona documentos directamente desde airSlate SignNow. Completa y comparte tus formularios desde la oficina o trabaja sin problemas en movimiento. No se requiere instalación ni software adicional. Todas las funciones están disponibles en línea, solo ingresa a signnow.com y crea tu propio flujo de firma electrónica.

Guía rápida para firmar el Acuerdo de Cobertura en minutos

- Crea una cuenta en airSlate SignNow (si aún no te has registrado) o inicia sesión usando tu Google o Facebook.

- Haz clic en Subir y selecciona uno de tus documentos.

- Usa la herramienta Mi Firma para crear tu firma única.

- Convierte el documento en un PDF dinámico con campos rellenables.

- Completa tu nuevo formulario y haz clic en Hecho.

Una vez terminado, envía una invitación para firmar a múltiples destinatarios. Obtén un contrato ejecutable en minutos usando cualquier dispositivo. Explora más funciones para crear PDFs profesionales; añade campos rellenables firma del Acuerdo de Cobertura y colabora en equipos. La solución de firma electrónica proporciona un flujo de trabajo seguro y funciona con base en la certificación SOC 2 Tipo II. Asegúrate de que tus datos estén protegidos y que nadie pueda modificarlos.

Cómo eFirmar un PDF en Google Chrome

¿Buscas una solución para firmar el Acuerdo de Cobertura directamente desde Chrome? La extensión de airSlate SignNow para Google está aquí para ayudarte. Encuentra un documento y desde tu navegador ábrelo fácilmente en el editor. Añade campos rellenables para texto y firma. Firma el PDF y compártelo de forma segura según GDPR, certificación SOC 2 Tipo II y más.

Usando esta breve guía paso a paso, expande tu flujo de firma electrónica en Google y firma el Acuerdo de Cobertura:

- Ve a la tienda web de Chrome y busca la extensión de airSlate SignNow.

- Haz clic en Agregar a Chrome.

- Inicia sesión en tu cuenta o regístrate una nueva.

- Sube un documento y haz clic en Abrir en airSlate SignNow.

- Modifica el documento.

- Firma el PDF usando la herramienta Mi Firma.

- Haz clic en Hecho para guardar tus cambios.

- Invita a otros participantes a firmar haciendo clic en Invitar a Firmar y seleccionando sus correos electrónicos/nombres.

Crea una firma integrada en tu flujo de trabajo para firmar el Acuerdo de Cobertura y obtener PDFs firmados en minutos. Di adiós a las pilas de papeles en tu oficina y comienza a ahorrar dinero y tiempo para tareas más importantes. Elegir la extensión de Google de airSlate SignNow es una opción práctica excelente con muchas ventajas.

Cómo firmar un adjunto en Gmail

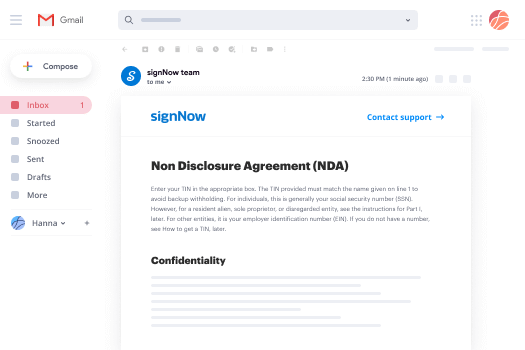

¿Eres como la mayoría, estás acostumbrado a descargar los adjuntos que recibes, imprimir y luego firmarlos, verdad? Bueno, tenemos buenas noticias para ti. Firmar documentos en tu bandeja de entrada ahora es mucho más fácil. El complemento de airSlate SignNow para Gmail te permite firmar el Acuerdo de Cobertura sin salir de tu buzón. Haz todo lo que necesitas; añade campos rellenables y envía solicitudes de firma con unos clics.

Cómo firmar el Acuerdo de Cobertura en Gmail:

- Busca airSlate SignNow para Gmail en el Mercado de G Suite y haz clic en Instalar.

- Inicia sesión en tu cuenta de airSlate SignNow o crea una nueva.

- Abre tu correo con el PDF que necesitas firmar.

- Haz clic en Subir para guardar el documento en tu cuenta de airSlate SignNow.

- Haz clic en Abrir documento para abrir el editor.

- Firma el PDF usando Mi Firma.

- Envía una solicitud de firma a los otros participantes haciendo clic en Enviar para Firmar.

- Ingresa su correo y presiona OK.

Como resultado, los otros participantes recibirán notificaciones indicándoles que deben firmar el documento. No necesitas descargar el PDF una y otra vez, simplemente firma el Acuerdo de Cobertura con unos clics. Este complemento es adecuado para quienes prefieren trabajar en cosas más valiosas en lugar de perder tiempo en nada. Aumenta tu trabajo diario obligatorio con el galardonado servicio de firma electrónica.

Cómo eFirmar una plantilla PDF en movimiento sin aplicación

Para muchos productos, realizar acuerdos en movimiento significa instalar una aplicación en tu teléfono. Nos complace decir que en airSlate SignNow hemos hecho que firmar en movimiento sea más rápido y fácil eliminando la necesidad de una aplicación móvil. Para firmar electrónicamente, abre tu navegador (cualquier navegador móvil) y accede directamente a airSlate SignNow y todas sus potentes herramientas de firma electrónica. Edita documentos, firma el Acuerdo de Cobertura y más. No se requiere instalación ni software adicional. Cierra tu acuerdo desde cualquier lugar.

Consulta nuestras instrucciones paso a paso que te enseñan cómo firmar el Acuerdo de Cobertura.

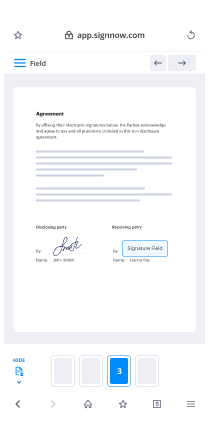

- Abre tu navegador y ve a signnow.com.

- Inicia sesión o crea una cuenta nueva.

- Sube o abre el documento que deseas firmar.

- Añade campos rellenables para texto, firma y fecha.

- Dibuja, escribe o sube tu firma.

- Haz clic en Guardar y Cerrar.

- Haz clic en Invitar a Firmar e ingresa el correo electrónico del destinatario si deseas que otros firmen el PDF.

Trabajar en móvil no es diferente a hacerlo en un escritorio: crea una plantilla reutilizable, firma el Acuerdo de Cobertura y gestiona el flujo como normalmente lo harías. En unos pocos clics, obtén un contrato ejecutable que puedes descargar a tu dispositivo y enviar a otros. Sin embargo, si realmente quieres una aplicación, descarga la aplicación móvil de airSlate SignNow. Es segura, rápida y tiene un diseño excelente. Experimenta flujos de firma electrónica fáciles desde tu lugar de trabajo, en un taxi o en un avión.

Cómo firmar un PDF usando un iPad

iOS es un sistema operativo muy popular equipado con herramientas nativas. Permite firmar y editar PDFs usando Preview sin software adicional. Sin embargo, por muy buena que sea la solución de Apple, no ofrece automatización. Mejora las capacidades de tu iPhone aprovechando la aplicación de airSlate SignNow. Usa tu iPhone o iPad para firmar el Acuerdo de Cobertura y más. Introduce automatización de firma electrónica en tu flujo móvil.

Firmar en un iPhone nunca ha sido tan fácil:

- Busca la aplicación de airSlate SignNow en la App Store e instálala.

- Crea una cuenta nueva o inicia sesión con tu Facebook o Google.

- Haz clic en Más y sube el archivo PDF que deseas firmar.

- Toca en el documento donde quieres insertar tu firma.

- Explora otras funciones: añade campos rellenables o firma el Acuerdo de Cobertura.

- Usa el botón Guardar para aplicar los cambios.

- Comparte tus documentos por correo electrónico o mediante un enlace de firma.

Haz PDFs profesionales directamente desde tu aplicación de airSlate SignNow. Aprovecha al máximo tu tiempo y trabaja desde cualquier lugar; en casa, en la oficina, en un autobús o en un avión, e incluso en la playa. Gestiona todo el flujo de documentos sin problemas: genera plantillas reutilizables, firma el Acuerdo de Cobertura y trabaja en archivos PDF con socios comerciales. Convierte tu dispositivo en una empresa altamente eficiente para ejecutar acuerdos.

Cómo firmar un archivo PDF usando un Android

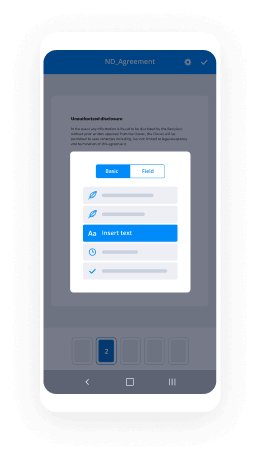

Para los usuarios de Android que gestionan documentos desde su teléfono, deben instalar software adicional. La Play Market es vasta y está llena de opciones, por lo que encontrar una buena aplicación no es difícil si tienes tiempo para explorar entre cientos de apps. Para ahorrar tiempo y evitar frustraciones, sugerimos airSlate SignNow para Android. Almacena y edita documentos, crea roles de firma e incluso firma el Acuerdo de Cobertura.

Los 9 pasos sencillos para optimizar tu flujo móvil:

- Abre la aplicación.

- Inicia sesión con tus cuentas de Facebook o Google o regístrate si aún no has autorizado.

- Haz clic en + para añadir un nuevo documento usando tu cámara, almacenamiento interno o en la nube.

- Toca en cualquier parte de tu PDF e inserta tu firma electrónica.

- Haz clic en OK para confirmar y firmar.

- Prueba más funciones de edición; añade imágenes, firma el Acuerdo de Cobertura, crea una plantilla reutilizable, etc.

- Haz clic en Guardar para aplicar los cambios una vez termines.

- Descarga el PDF o compártelo por correo electrónico.

- Utiliza la función Invitar a Firmar si deseas establecer y enviar un orden de firma a los destinatarios.

Convierte lo mundano y rutinario en algo fácil y fluido con la aplicación de airSlate SignNow para Android. Firma y envía documentos para firma desde cualquier lugar donde estés conectado a internet. Crea PDFs con aspecto profesional y firma el Acuerdo de Cobertura con unos pocos clics. Crea un proceso de firma electrónica impecable solo con tu teléfono inteligente y aumenta tu productividad total.

¡Obtenga firmas legalmente vinculantes ahora!

Preguntas frecuentes

-

¿Cómo funciona la cobertura?

La cobertura se refiere a comprar una inversión diseñada para reducir el riesgo de pérdidas de otra inversión. Los inversores a menudo compran una inversión opuesta para hacer esto, como usar una opción de venta para cubrirse contra pérdidas en una posición en acciones, ya que una pérdida en la acción será en cierta medida compensada por una ganancia en la opción. -

¿Qué es la cobertura en términos simples?

Significado de cobertura. La cobertura, en finanzas, es una estrategia de gestión de riesgos. Se trata de reducir o eliminar el riesgo de incertidumbre. ... En términos simples, es cubrir una inversión invirtiendo en otra inversión. Generalmente, cuando las personas planean cubrirse, intentan asegurarse contra un evento negativo. -

¿Qué quieres decir con cobertura?

Una estrategia de gestión de riesgos utilizada para limitar o compensar la probabilidad de pérdida por fluctuaciones en los precios de productos básicos, monedas o valores. En efecto, la cobertura es una transferencia de riesgo sin comprar pólizas de seguro. -

¿Qué quieres decir con cobertura en finanzas?

Cubrirse contra el riesgo de inversión significa usar estratégicamente instrumentos financieros o estrategias de mercado para compensar el riesgo de movimientos adversos en los precios. ... Entonces, la cobertura, en su mayor parte, no es una técnica para ganar dinero, sino para reducir pérdidas potenciales. -

¿Qué es un acuerdo de cobertura?

Un acuerdo de cobertura significa cualquier swap, tope, collar, compra a plazo o acuerdos o arreglos similares relacionados con tasas de interés, tipos de cambio o precios de commodities, ya sea en general o bajo contingencias específicas. Basado en 148 documentos 148. \uff0b Nueva lista. -

¿Cuáles son las actividades de cobertura?

La cobertura es una estrategia de gestión de riesgos empleada para compensar pérdidas en inversiones. La reducción del riesgo generalmente resulta en una reducción de las ganancias potenciales. Las estrategias de cobertura generalmente involucran derivados, como opciones y futuros. -

¿Qué significa cubrir un préstamo?

Cubrirse contra el riesgo de inversión significa usar estratégicamente instrumentos financieros o estrategias de mercado para compensar el riesgo de movimientos adversos en los precios. ... Entonces, la cobertura, en su mayor parte, no es una técnica para ganar dinero, sino para reducir pérdidas potenciales. -

¿Cómo se usa hedge en una oración?

Termina la poda de todos los árboles de hoja caduca y setos lo antes posible. ... Los setos son de FIG. inglesa ... A menudo se cortan para formar setos en jardines. ... Los setos más pequeños pueden estar formados por boj perenne o por arbustos de árbol. ... Al cortar, el seto (como en realidad todos los setos) debe ser XVI. -

¿Cómo ganan dinero los fondos de cobertura?

El fondo de cobertura gana dinero cobrando una tarifa de gestión y una tarifa de rendimiento. Aunque estas tarifas difieren según el fondo, generalmente son del 2% y del 20% de los activos bajo gestión. Tarifas de gestión: Esta tarifa se calcula como un porcentaje de los activos bajo gestión. ... Este incentivo motiva al fondo a generar rendimientos excesivos. -

¿Por qué el acuerdo maestro de ISDA?

El Acuerdo Maestro de ISDA es el contrato estándar utilizado para gobernar todas las transacciones de derivados OTC (sobre mercado) celebradas entre las partes. ... El propósito del Acuerdo Maestro de ISDA es establecer disposiciones que rijan la relación general de las partes1. -

¿Cómo se cubre el USD?

Pida prestado la moneda extranjera en una cantidad equivalente al valor presente del recepcionista. ... Convierta la moneda extranjera en moneda nacional a la tasa de cambio spot. Deposite la moneda nacional a la tasa de interés vigente.