Plantilla De Acuerdo De Liquidación De Deuda Fácil De Usar

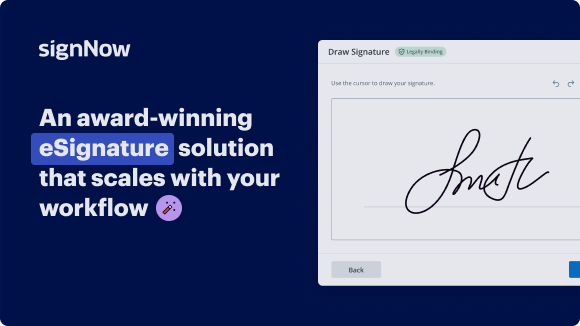

Solución de firma electrónica galardonada

Obtén las potentes capacidades de firma electrónica que necesitas de la empresa en la que confías

Selecciona el servicio profesional diseñado para profesionales

Configura la API de firma electrónica con facilidad

Trabaja mejor en equipo

Firma plantilla de acuerdo de liquidación de deuda en minutos

Reduce el tiempo de cierre

Mantén los datos sensibles seguros

Vea las firmas electrónicas de airSlate SignNow en acción

Soluciones de airSlate SignNow para una mayor eficiencia

Las reseñas de nuestros usuarios hablan por sí mismas

Por qué elegir airSlate SignNow

-

Prueba gratuita de 7 días. Elige el plan que necesitas y pruébalo sin riesgos.

-

Precios honestos para planes completos. airSlate SignNow ofrece planes de suscripción sin cargos adicionales ni tarifas ocultas al renovar.

-

Seguridad de nivel empresarial. airSlate SignNow te ayuda a cumplir con los estándares de seguridad globales.

Tu guía paso a paso — sign debt settlement agreement template

Al emplear la firma electrónica de airSlate SignNow, cualquier empresa puede aumentar los flujos de firma y firmar en línea en tiempo real, ofreciendo una experiencia mejorada a clientes y empleados. Usa la firma en la Plantilla de Acuerdo de Liquidación de Deuda en unos pocos pasos sencillos. Nuestras aplicaciones móviles permiten trabajar en movimiento, incluso sin conexión! Firma contratos desde cualquier lugar del mundo y cierra tratos más rápido.

Sigue la guía paso a paso para usar la Plantilla de Acuerdo de Liquidación de Deuda:

- Inicia sesión en tu cuenta de airSlate SignNow.

- Encuentra tu documento en tus carpetas o sube uno nuevo.

- Abre el documento y haz ediciones usando el menú Herramientas.

- Arrastra y suelta áreas rellenables, escribe texto y firma.

- Incluye múltiples firmantes usando sus correos electrónicos y establece el orden de firma.

- Indica qué usuarios recibirán un documento firmado.

- Usa Opciones avanzadas para restringir el acceso al documento y establecer una fecha de vencimiento.

- Haz clic en Guardar y cerrar cuando termines.

Además, hay más herramientas innovadoras disponibles para firmar la Plantilla de Acuerdo de Liquidación de Deuda. Agrega usuarios a tu entorno de trabajo común, navega por los equipos y realiza un seguimiento de la cooperación. Millones de consumidores en EE. UU. y Europa reconocen que un sistema que reúne a las personas en un área de trabajo holística es exactamente lo que las empresas necesitan para mantener los flujos de trabajo funcionando sin problemas. La API REST de airSlate SignNow te permite integrar firmas electrónicas en tu aplicación, sitio web, CRM o nube. Descubre airSlate SignNow y obtén flujos de firma electrónica más rápidos, fáciles y en general más productivos!

Cómo funciona

Funciones de airSlate SignNow que los usuarios adoran

Vea resultados excepcionales Plantilla de Acuerdo de Liquidación de Deuda fácil de usar

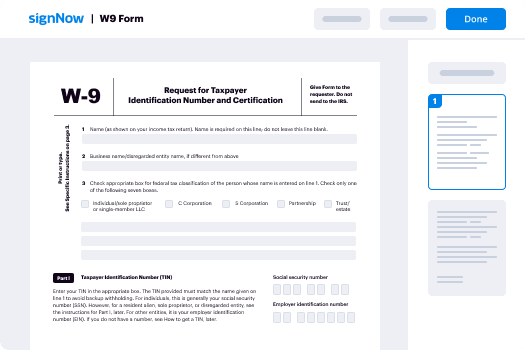

Cómo enviar y firmar un PDF en línea

Prueba la forma más rápida de firmar la Plantilla de Acuerdo de Liquidación de Deuda. Evita flujos de trabajo en papel y gestiona documentos directamente desde airSlate SignNow. Completa y comparte tus formularios desde la oficina o trabaja sin problemas en movimiento. No se requiere instalación ni software adicional. Todas las funciones están disponibles en línea, solo visita signnow.com y crea tu propio flujo de firma electrónica.

Guía rápida para firmar la Plantilla de Acuerdo de Liquidación de Deuda en minutos

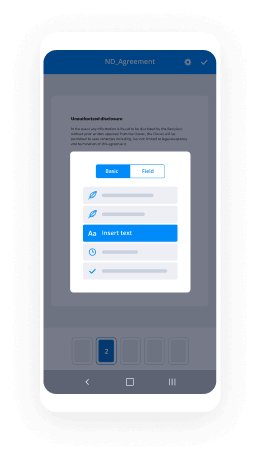

- Crea una cuenta en airSlate SignNow (si aún no te has registrado) o inicia sesión con tu Google o Facebook.

- Haz clic en Subir y selecciona uno de tus documentos.

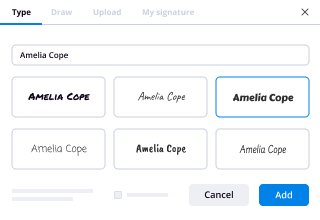

- Usa la herramienta Mi Firma para crear tu firma única.

- Convierte el documento en un PDF dinámico con campos rellenables.

- Llena tu nuevo formulario y haz clic en Hecho.

Una vez terminado, envía una invitación para firmar a múltiples destinatarios. Obtén un contrato ejecutable en minutos usando cualquier dispositivo. Explora más funciones para crear PDFs profesionales; añade campos rellenables, firma la Plantilla de Acuerdo de Liquidación de Deuda y colabora en equipos. La solución de firma electrónica ofrece un flujo de trabajo seguro y funciones basadas en la certificación SOC 2 Tipo II. Asegúrate de que todos tus datos estén protegidos y que nadie pueda editarlos.

Cómo firmar electrónicamente una plantilla PDF en Google Chrome

¿Buscas una solución para firmar la Plantilla de Acuerdo de Liquidación de Deuda directamente desde Chrome? La extensión de airSlate SignNow para Google está aquí para ayudarte. Encuentra un documento y desde tu navegador ábrelo fácilmente en el editor. Añade campos rellenables para texto y firma. Firma el PDF y compártelo de forma segura según GDPR, certificación SOC 2 Tipo II y más.

Usando esta breve guía paso a paso, expande tu flujo de firma electrónica en Google y firma la Plantilla de Acuerdo de Liquidación de Deuda:

- Ve a la tienda web de Chrome y busca la extensión de airSlate SignNow.

- Haz clic en Agregar a Chrome.

- Inicia sesión en tu cuenta o regístrate una nueva.

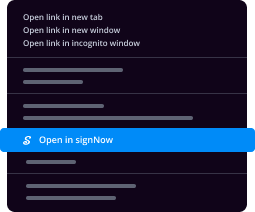

- Sube un documento y haz clic en Abrir en airSlate SignNow.

- Modifica el documento.

- Firma el PDF usando la herramienta Mi Firma.

- Haz clic en Hecho para guardar tus ediciones.

- Invita a otros participantes a firmar haciendo clic en Invitar a Firmar y seleccionando sus correos electrónicos/nombres.

Crea una firma que esté integrada en tu flujo de trabajo para firmar la Plantilla de Acuerdo de Liquidación de Deuda y obtener PDFs firmados electrónicamente en minutos. Di adiós a las pilas de papeles en tu oficina y comienza a ahorrar dinero y tiempo para tareas más importantes. Elegir la extensión de Google de airSlate SignNow es una decisión muy conveniente con muchas ventajas.

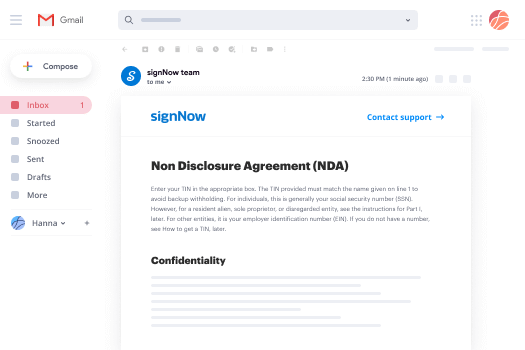

Cómo firmar electrónicamente un adjunto en Gmail

Si eres como la mayoría, estás acostumbrado a descargar los adjuntos que recibes, imprimirlos y luego firmarlos, ¿verdad? Bueno, tenemos buenas noticias para ti. Firmar documentos en tu bandeja de entrada ahora es mucho más fácil. El complemento de airSlate SignNow para Gmail te permite firmar la Plantilla de Acuerdo de Liquidación de Deuda sin salir de tu buzón. Haz todo lo que necesitas; añade campos rellenables y envía solicitudes de firma con unos clics.

Cómo firmar la Plantilla de Acuerdo de Liquidación de Deuda en Gmail:

- Busca airSlate SignNow para Gmail en el Mercado de G Suite y haz clic en Instalar.

- Inicia sesión en tu cuenta de airSlate SignNow o crea una nueva.

- Abre tu correo con el PDF que necesitas firmar.

- Haz clic en Subir para guardar el documento en tu cuenta de airSlate SignNow.

- Haz clic en Abrir documento para abrir el editor.

- Firma el PDF usando Mi Firma.

- Envía una solicitud de firma a los otros participantes haciendo clic en Enviar para Firmar.

- Ingresa su correo y presiona OK.

Como resultado, los otros participantes recibirán notificaciones indicándoles que deben firmar el documento. No es necesario descargar el PDF una y otra vez, simplemente firma la Plantilla de Acuerdo de Liquidación de Deuda con unos clics. Este complemento es adecuado para quienes prefieren trabajar en tareas más valiosas en lugar de perder tiempo en cosas sin importancia. Incrementa tu trabajo diario obligatorio con la solución de firma electrónica galardonada.

Cómo firmar electrónicamente un PDF en movimiento sin una aplicación móvil

Para muchos productos, realizar tratos en movimiento significa instalar una aplicación en tu teléfono. En airSlate SignNow estamos felices de decir que hemos hecho que firmar en movimiento sea más rápido y fácil eliminando la necesidad de una aplicación móvil. Para firmar electrónicamente, abre tu navegador (cualquier navegador móvil) y accede directamente a airSlate SignNow y todas sus potentes herramientas de firma electrónica. Edita documentos, firma la Plantilla de Acuerdo de Liquidación de Deuda y más. No se requiere instalación ni software adicional. Cierra tu trato desde cualquier lugar.

Consulta nuestras instrucciones paso a paso que te enseñan cómo firmar la Plantilla de Acuerdo de Liquidación de Deuda.

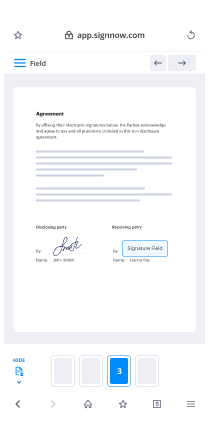

- Abre tu navegador y ve a signnow.com.

- Inicia sesión o registra una nueva cuenta.

- Sube o abre el documento que deseas editar.

- Añade campos rellenables para texto, firma y fecha.

- Dibuja, escribe o sube tu firma.

- Haz clic en Guardar y Cerrar.

- Haz clic en Invitar a Firmar e ingresa el correo electrónico del destinatario si quieres que otros firmen el PDF.

Trabajar en móvil no es diferente que en un escritorio: crea una plantilla reutilizable, firma la Plantilla de Acuerdo de Liquidación de Deuda y gestiona el flujo como normalmente lo harías. En unos pocos clics, obtén un contrato ejecutable que puedes descargar a tu dispositivo y enviar a otros. Sin embargo, si realmente quieres una aplicación, descarga la aplicación móvil de airSlate SignNow. Es segura, rápida y tiene un excelente diseño. Experimenta flujos de firma electrónica sin esfuerzo desde tu lugar de trabajo, en un taxi o en un avión.

Cómo firmar un archivo PDF usando un iPhone

iOS es un sistema operativo muy popular equipado con herramientas nativas. Permite firmar y editar PDFs usando Preview sin software adicional. Sin embargo, por muy buena que sea la solución de Apple, no ofrece automatización. Mejora las capacidades de tu iPhone aprovechando la aplicación de airSlate SignNow. Usa tu iPhone o iPad para firmar la Plantilla de Acuerdo de Liquidación de Deuda y más. Introduce la automatización de firma electrónica en tu flujo móvil.

Firmar en un iPhone nunca ha sido tan fácil:

- Busca la aplicación de airSlate SignNow en la App Store e instálala.

- Crea una cuenta nueva o inicia sesión con tu Facebook o Google.

- Haz clic en Plus y sube el archivo PDF que deseas firmar.

- Toca en el documento donde quieres insertar tu firma.

- Explora otras funciones: añade campos rellenables o firma la Plantilla de Acuerdo de Liquidación de Deuda.

- Usa el botón Guardar para aplicar los cambios.

- Comparte tus documentos por correo electrónico o mediante un enlace de firma.

Haz PDFs profesionales directamente desde tu aplicación de airSlate SignNow. Aprovecha al máximo tu tiempo y trabaja desde cualquier lugar; en casa, en la oficina, en un autobús o en un avión, e incluso en la playa. Gestiona todo el flujo de documentos sin problemas: crea plantillas reutilizables, firma la Plantilla de Acuerdo de Liquidación de Deuda y trabaja en archivos PDF con socios comerciales. Convierte tu dispositivo en una herramienta empresarial potente para cerrar contratos.

Cómo firmar un PDF aprovechando un Android

Para los usuarios de Android, gestionar documentos desde su teléfono requiere instalar software adicional. La Play Market es vasta y está llena de opciones, por lo que encontrar una buena aplicación no es difícil si tienes tiempo para explorar entre cientos de apps. Para ahorrar tiempo y evitar frustraciones, te sugerimos airSlate SignNow para Android. Almacena y edita documentos, crea roles de firma e incluso firma la Plantilla de Acuerdo de Liquidación de Deuda.

Los 9 pasos sencillos para optimizar tu flujo de trabajo móvil:

- Abre la aplicación.

- Inicia sesión usando tus cuentas de Facebook o Google o regístrate si aún no has autorizado.

- Haz clic en + para añadir un nuevo documento usando tu cámara, almacenamiento interno o en la nube.

- Toca en cualquier parte de tu PDF e inserta tu firma electrónica.

- Haz clic en OK para confirmar y firmar.

- Prueba más funciones de edición; añade imágenes, firma la Plantilla de Acuerdo de Liquidación de Deuda, crea una plantilla reutilizable, etc.

- Haz clic en Guardar para aplicar los cambios una vez termines.

- Descarga el PDF o compártelo por correo electrónico.

- Utiliza la función Invitar a firmar si quieres establecer y enviar un orden de firma a los destinatarios.

Convierte lo mundano y rutinario en algo fácil y fluido con la aplicación de airSlate SignNow para Android. Firma y envía documentos para firma desde cualquier lugar donde estés conectado a internet. Crea PDFs con aspecto profesional y firma la Plantilla de Acuerdo de Liquidación de Deuda con unos pocos clics. Crea un flujo de firma electrónica perfecto solo con tu teléfono inteligente y aumenta tu productividad general.

¡Obtenga firmas legalmente vinculantes ahora!

Preguntas frecuentes

-

¿Cómo escribo un acuerdo de liquidación de deuda?

Un acuerdo de liquidación de deuda es una forma de contrato. Un acuerdo de liquidación debe contener ocho hechos, incluyendo una descripción de la deuda, la cantidad adeudada, el acreedor original y cualquier número de cuenta. Deja claro que la cantidad que pagas lleva la deuda a $0 y cierra el asunto por completo. -

¿Es buena idea la liquidación de deuda?

¿Es buena idea la liquidación de deuda? La respuesta corta: las opiniones están divididas. La liquidación de deuda puede ayudar a algunas personas a salir de la deuda a un costo menor que lo que deben. ... Así funciona la liquidación de deuda: dejas de hacer pagos a tus acreedores por un período de tiempo, a menudo seis meses o más. -

¿Qué significa liquidar una deuda?

Liquidar una deuda significa que un acreedor ha aceptado recibir menos de la cantidad que debes como pago completo. También significa que los cobradores no pueden seguir acosándote por el dinero y no tienes que preocuparte de que puedan demandarte por la deuda. ... La liquidación de deuda puede destruir tu crédito. -

¿Qué es un acuerdo de pago?

Un Acuerdo de Pago es un esquema de los términos y condiciones importantes de un préstamo. Los períodos de pago, las cantidades y las tasas de interés pueden ser críticos para el acuerdo de préstamo y probablemente sea mejor documentar todos esos elementos por escrito. -

¿Qué pasa si cancelo la ayuda para la deuda nacional?

Si no podemos liquidar tu deuda o si no estás satisfecho por cualquier motivo hasta el momento en que resolvamos tus deudas, puedes cancelar en cualquier momento sin penalizaciones ni tarifas! Si no podemos liquidar alguna de tus cuentas, no nos pagas. ¡Es así de simple! Obtenemos resultados o no pagas! -

¿Cuál es la cantidad mínima que un cobrador aceptará para liquidar?

Un cobrador puede aceptar alrededor del 50 por ciento de la factura, y Loftsgordon recomienda comenzar las negociaciones con un monto bajo para permitir que el cobrador contraoferta. Si ofreces un pago único o cualquier arreglo de pago alternativo, asegúrate de poder cumplir con esos nuevos parámetros de pago. -

¿Cuánto puede reducir un cobrador de deudas?

Un cobrador puede aceptar alrededor del 50 por ciento de la factura, y Loftsgordon recomienda comenzar las negociaciones con un monto bajo para permitir que el cobrador contraoferta. Si ofreces un pago único o cualquier arreglo de pago alternativo, asegúrate de poder cumplir con esos nuevos parámetros de pago.