Sign Mortgage Financing Agreement Securely with SignNow

Solución de firma electrónica galardonada

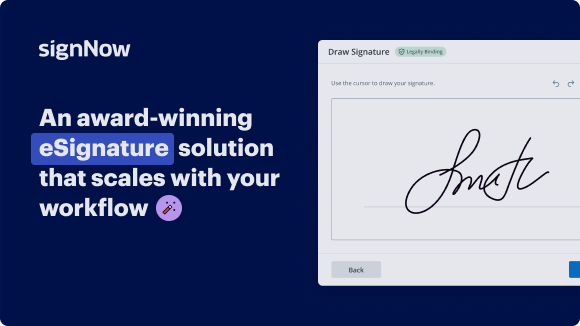

Do more online with a globally-trusted eSignature platform

Standout signing experience

Robust reporting and analytics

Mobile eSigning in person and remotely

Industry regulations and compliance

Sign mortgage financing agreement, quicker than ever before

Handy eSignature extensions

Vea las firmas electrónicas de airSlate SignNow en acción

Soluciones de airSlate SignNow para una mayor eficiencia

Las reseñas de nuestros usuarios hablan por sí mismas

Por qué elegir airSlate SignNow

-

Prueba gratuita de 7 días. Elige el plan que necesitas y pruébalo sin riesgos.

-

Precios honestos para planes completos. airSlate SignNow ofrece planes de suscripción sin cargos adicionales ni tarifas ocultas al renovar.

-

Seguridad de nivel empresarial. airSlate SignNow te ayuda a cumplir con los estándares de seguridad globales.

Tu guía paso a paso — sign mortgage financing agreement

Adopting airSlate SignNow’s electronic signature any business can accelerate signature workflows and sign online in real-time, delivering a better experience to consumers and employees. Use sign Mortgage Financing Agreement in a few easy steps. Our mobile apps make operating on the move possible, even while offline! Sign signNows from any place in the world and close tasks in no time.

Follow the walk-through guide for using sign Mortgage Financing Agreement:

- Log in to your airSlate SignNow account.

- Find your needed form within your folders or upload a new one.

- Open the record and edit content using the Tools list.

- Drop fillable fields, type textual content and eSign it.

- Add multiple signers by emails configure the signing sequence.

- Specify which users will receive an completed version.

- Use Advanced Options to limit access to the record add an expiry date.

- Click Save and Close when completed.

Moreover, there are more innovative features available for sign Mortgage Financing Agreement. Add users to your collaborative work enviroment, view teams, and keep track of cooperation. Numerous customers all over the US and Europe recognize that a solution that brings people together in one holistic digital location, is what companies need to keep workflows functioning efficiently. The airSlate SignNow REST API allows you to integrate eSignatures into your application, website, CRM or cloud. Try out airSlate SignNow and enjoy faster, smoother and overall more efficient eSignature workflows!

Cómo funciona

Funciones de airSlate SignNow que los usuarios adoran

Vea resultados excepcionales Sign Mortgage Financing Agreement Securely with signNow

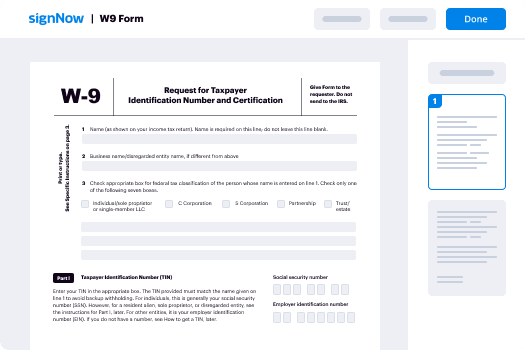

How to fill in and eSign a PDF online

Try out the fastest way to sign Mortgage Financing Agreement. Avoid paper-based workflows and manage documents right from airSlate SignNow. Complete and share your forms from the office or seamlessly work on-the-go. No installation or additional software required. All features are available online, just go to signnow.com and create your own eSignature flow.

A brief guide on how to sign Mortgage Financing Agreement in minutes

- Create an airSlate SignNow account (if you haven’t registered yet) or log in using your Google or Facebook.

- Click Upload and select one of your documents.

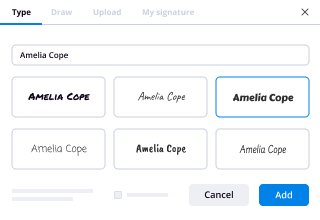

- Use the My Signature tool to create your unique signature.

- Turn the document into a dynamic PDF with fillable fields.

- Fill out your new form and click Done.

Once finished, send an invite to sign to multiple recipients. Get an enforceable contract in minutes using any device. Explore more features for making professional PDFs; add fillable fields sign Mortgage Financing Agreement and collaborate in teams. The eSignature solution supplies a protected workflow and functions based on SOC 2 Type II Certification. Make sure that your data are protected so no person can take them.

How to eSign a PDF file in Google Chrome

Are you looking for a solution to sign Mortgage Financing Agreement directly from Chrome? The airSlate SignNow extension for Google is here to help. Find a document and right from your browser easily open it in the editor. Add fillable fields for text and signature. Sign the PDF and share it safely according to GDPR, SOC 2 Type II Certification and more.

Using this brief how-to guide below, expand your eSignature workflow into Google and sign Mortgage Financing Agreement:

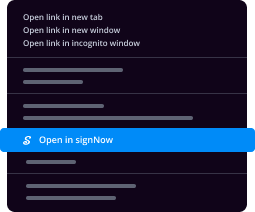

- Go to the Chrome web store and find the airSlate SignNow extension.

- Click Add to Chrome.

- Log in to your account or register a new one.

- Upload a document and click Open in airSlate SignNow.

- Modify the document.

- Sign the PDF using the My Signature tool.

- Click Done to save your edits.

- Invite other participants to sign by clicking Invite to Sign and selecting their emails/names.

Create a signature that’s built in to your workflow to sign Mortgage Financing Agreement and get PDFs eSigned in minutes. Say goodbye to the piles of papers sitting on your workplace and begin saving money and time for more crucial tasks. Picking out the airSlate SignNow Google extension is a great convenient option with a lot of benefits.

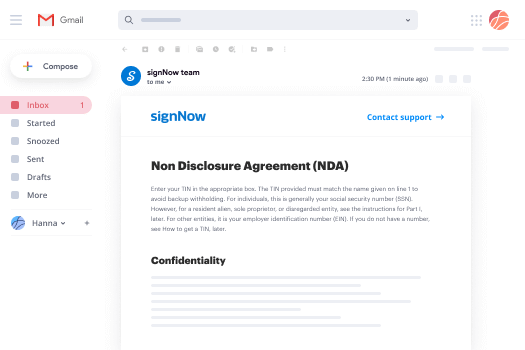

How to eSign an attachment in Gmail

If you’re like most, you’re used to downloading the attachments you get, printing them out and then signing them, right? Well, we have good news for you. Signing documents in your inbox just got a lot easier. The airSlate SignNow add-on for Gmail allows you to sign Mortgage Financing Agreement without leaving your mailbox. Do everything you need; add fillable fields and send signing requests in clicks.

How to sign Mortgage Financing Agreement in Gmail:

- Find airSlate SignNow for Gmail in the G Suite Marketplace and click Install.

- Log in to your airSlate SignNow account or create a new one.

- Open up your email with the PDF you need to sign.

- Click Upload to save the document to your airSlate SignNow account.

- Click Open document to open the editor.

- Sign the PDF using My Signature.

- Send a signing request to the other participants with the Send to Sign button.

- Enter their email and press OK.

As a result, the other participants will receive notifications telling them to sign the document. No need to download the PDF file over and over again, just sign Mortgage Financing Agreement in clicks. This add-one is suitable for those who choose working on more valuable things rather than wasting time for absolutely nothing. Boost your daily compulsory labour with the award-winning eSignature platform.

How to sign a PDF file on the go with no application

For many products, getting deals done on the go means installing an app on your phone. We’re happy to say at airSlate SignNow we’ve made singing on the go faster and easier by eliminating the need for a mobile app. To eSign, open your browser (any mobile browser) and get direct access to airSlate SignNow and all its powerful eSignature tools. Edit docs, sign Mortgage Financing Agreement and more. No installation or additional software required. Close your deal from anywhere.

Take a look at our step-by-step instructions that teach you how to sign Mortgage Financing Agreement.

- Open your browser and go to signnow.com.

- Log in or register a new account.

- Upload or open the document you want to edit.

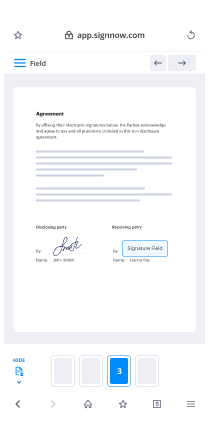

- Add fillable fields for text, signature and date.

- Draw, type or upload your signature.

- Click Save and Close.

- Click Invite to Sign and enter a recipient’s email if you need others to sign the PDF.

Working on mobile is no different than on a desktop: create a reusable template, sign Mortgage Financing Agreement and manage the flow as you would normally. In a couple of clicks, get an enforceable contract that you can download to your device and send to others. Yet, if you really want an application, download the airSlate SignNow mobile app. It’s secure, quick and has a great layout. Experience seamless eSignature workflows from your business office, in a taxi or on a plane.

How to sign a PDF file utilizing an iPhone

iOS is a very popular operating system packed with native tools. It allows you to sign and edit PDFs using Preview without any additional software. However, as great as Apple’s solution is, it doesn't provide any automation. Enhance your iPhone’s capabilities by taking advantage of the airSlate SignNow app. Utilize your iPhone or iPad to sign Mortgage Financing Agreement and more. Introduce eSignature automation to your mobile workflow.

Signing on an iPhone has never been easier:

- Find the airSlate SignNow app in the AppStore and install it.

- Create a new account or log in with your Facebook or Google.

- Click Plus and upload the PDF file you want to sign.

- Tap on the document where you want to insert your signature.

- Explore other features: add fillable fields or sign Mortgage Financing Agreement.

- Use the Save button to apply the changes.

- Share your documents via email or a singing link.

Make a professional PDFs right from your airSlate SignNow app. Get the most out of your time and work from anywhere; at home, in the office, on a bus or plane, and even at the beach. Manage an entire record workflow seamlessly: generate reusable templates, sign Mortgage Financing Agreement and work on PDF files with business partners. Turn your device into a highly effective business instrument for executing offers.

How to sign a PDF file Android

For Android users to manage documents from their phone, they have to install additional software. The Play Market is vast and plump with options, so finding a good application isn’t too hard if you have time to browse through hundreds of apps. To save time and prevent frustration, we suggest airSlate SignNow for Android. Store and edit documents, create signing roles, and even sign Mortgage Financing Agreement.

The 9 simple steps to optimizing your mobile workflow:

- Open the app.

- Log in using your Facebook or Google accounts or register if you haven’t authorized already.

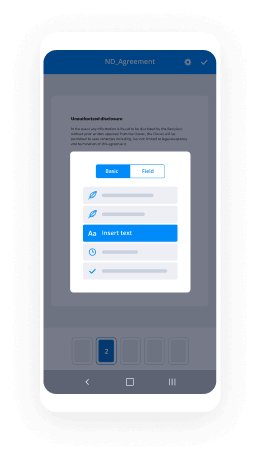

- Click on + to add a new document using your camera, internal or cloud storages.

- Tap anywhere on your PDF and insert your eSignature.

- Click OK to confirm and sign.

- Try more editing features; add images, sign Mortgage Financing Agreement, create a reusable template, etc.

- Click Save to apply changes once you finish.

- Download the PDF or share it via email.

- Use the Invite to sign function if you want to set & send a signing order to recipients.

Turn the mundane and routine into easy and smooth with the airSlate SignNow app for Android. Sign and send documents for signature from any place you’re connected to the internet. Build professional-looking PDFs and sign Mortgage Financing Agreement with a few clicks. Created a flawless eSignature process with only your smartphone and improve your overall efficiency.

¡Obtenga firmas legalmente vinculantes ahora!

Preguntas frecuentes

-

Does the lender have to sign the mortgage?

A real estate property loan is generally referred to as a mortgage. ... The primary borrower and all co-borrowers sign the mortgage or trust deed. State law dictates whether a mortgage or a trust deed is recorded, but some states permit either document to be used, says Private Money Lending. -

Who is present at a mortgage closing?

Who Attends the Closing of a House? Depending on where you live, those at your closing appointment might include you (the buyer), the seller, the escrow/closing agent, the attorney (who might also be the closing agent), a title company representative, the mortgage lender, and the real estate agents. -

Who signs promissory note?

In general, at least the borrower should sign the promissory note. Depending how much the parties trust each other, you may also wish to have the lender sign as well AND get the signatures signNowd. -

Who signs a mortgage note?

While the mortgage deed or contract itself hypothecates or imposes a lien on the title to real property as security for a loan, the mortgage note states the amount of debt and the rate of interest, and obligates the borrower, who signs the note, personally responsible for repayment. -

Can a non borrower be on title?

All borrowers on the mortgage application typically must be on title as an owner. However, non-borrowers can be on title as well. This means that both you and your spouse or partner are considered official owners of the residence. -

Can you be on the mortgage but not the note?

A: No. First you did not sign the promissory note you are not responsible or obligated to pay the payments. However if the payments are not made then the property will be foreclosed and ultimately sold. Thus your rights to stay in the home will someday be cutoff. -

What happens after the contract is signed?

Title. In most states, once the contract is signed and an earnest money check is written, the check is deposited with a third party such as an attorney or a title and escrow company. ... A title search confirms that the seller has the legal right to sell the property, and that the title is free of liens. -

Is a loan better than a mortgage?

Personal loans typically have much shorter repayment terms and higher interest rates than mortgage loans, making them a poor choice in that situation. However, if you're planning to purchase a very small home or mobile home, where the cost is much lower, a personal loan may be a decent option. -

When buying a house when do you get the deed?

The day the deed gets recorded is the day you own the home. Depending on the county, you usually get the deed mailed to you in a week to sometimes 3 weeks or more. But they does not affect your ownership. When the loan is paid off, if you have a loan, you get a release of that loan when paid off. -

Do loans affect your mortgage?

When you're applying for a mortgage, any debts you have -- auto loans, student loans, credit cards, and personal loans -- can affect how much you can borrow and whether you can qualify for a mortgage in the first place. -

What are credit arrangements?

A \u201cCredit Arrangement\u201d is a maximum amount a client (individual, group or company) can take in loans and overdrafts. ... A client or a group may have multiple Credit Arrangements, each linked with specific loan and overdraft accounts. -

Will I get a mortgage if I have an agreement in principle?

A mortgage in principle does not guarantee that your application for a mortgage will be accepted, nor does it make any guarantees about the amount that you can borrow. That's because the initial credit checks are limited, so the lender doesn't have a full view of your financial situation. -

What are the 3 types of credits?

There are three types of credit accounts: revolving, installment and open. One of the most common types of credit accounts, revolving credit is a line of credit that you can borrow from freely but that has a cap, known as a credit limit, on how much can be used at any given time. -

At what stage can a mortgage be declined?

The stages at which mortgages can be declined are: Mortgage not applied for (bank or broker has told you that you won't qualify) Decision in principle declined. Refused after a decision in principle is approved.