Signer Accord De Couverture Facilité

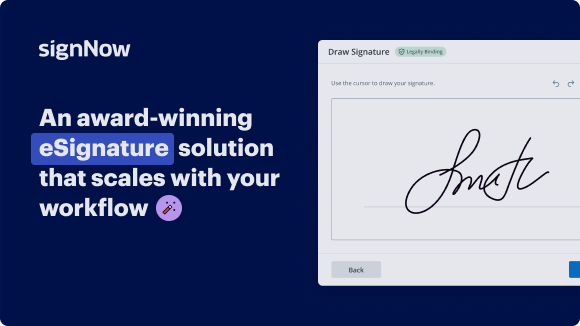

Solution eSignature primée

Améliorez votre flux de travail documentaire avec airSlate SignNow

Flux de travail eSignature polyvalents

Visibilité rapide sur l'état du document

Configuration d'intégration facile et rapide

Signer un accord de couverture sur n'importe quel appareil

Traçabilité avancée des audits

Exigences de sécurité rigoureuses

Découvrez les signatures électroniques airSlate SignNow en action

Solutions airSlate SignNow pour une meilleure efficacité

Les avis de nos utilisateurs parlent d'eux-mêmes

Pourquoi choisir airSlate SignNow

-

Essai gratuit de 7 jours. Choisissez le forfait dont vous avez besoin et essayez-le sans risque.

-

Tarification honnête pour des forfaits complets. airSlate SignNow propose des abonnements sans frais supplémentaires ni frais cachés lors du renouvellement.

-

Sécurité de niveau entreprise. airSlate SignNow vous aide à respecter les normes de sécurité mondiales.

Votre guide étape par étape — sign hedging agreement

En utilisant la signature électronique d'airSlate SignNow, toute organisation peut améliorer ses flux de signature et signer en ligne en temps réel, offrant une meilleure expérience aux consommateurs et au personnel. Utilisez signer Accord de couverture en quelques étapes simples. Nos applications mobiles portables rendent le travail en déplacement possible, même hors ligne! eSign signNow de n'importe où dans le monde et réalisez des tâches en un rien de temps.

Suivez les instructions étape par étape pour utiliser signer Accord de couverture :

- Connectez-vous à votre profil airSlate SignNow.

- Trouvez votre document dans vos dossiers ou téléchargez-en un nouveau.

- Accédez au modèle en utilisant le menu Outils.

- Faites glisser et déposez les champs remplissables, ajoutez du texte et eSignez-le.

- Ajoutez plusieurs signataires par e-mails, configurez l'ordre de signature.

- Indiquez quels utilisateurs peuvent recevoir un document signé.

- Utilisez Options avancées pour limiter l'accès au document et définir une date d'expiration.

- Appuyez sur Enregistrer et Fermer une fois terminé.

De plus, il existe des fonctions plus avancées accessibles pour signer Accord de couverture. Ajoutez des utilisateurs à votre espace de travail collaboratif, parcourez les équipes et surveillez la collaboration. Des millions d'utilisateurs à travers les États-Unis et l'Europe conviennent qu'un système qui rassemble les gens dans un espace de travail cohésif est ce dont les entreprises ont besoin pour que les flux de travail fonctionnent sans problème. L'API REST airSlate SignNow vous permet d'intégrer les signatures électroniques dans votre application, site web, CRM ou cloud. Essayez airSlate SignNow et obtenez des flux de signature électronique plus rapides, plus fluides et globalement plus productifs!

Comment ça marche

Fonctionnalités airSlate SignNow appréciées par les utilisateurs

Découvrez des résultats exceptionnels signer Accord de couverture facilité

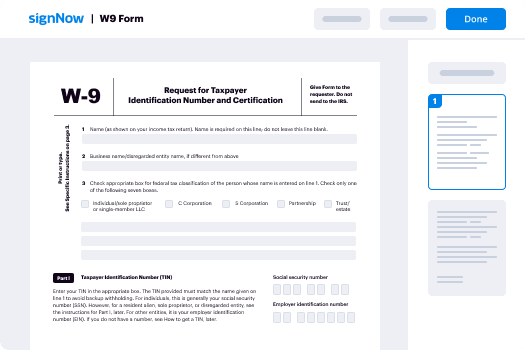

Comment remplir et signer un document en ligne

Essayez la méthode la plus rapide pour signer Accord de couverture. Évitez les flux de travail papier et gérez les documents directement depuis airSlate SignNow. Remplissez et partagez vos formulaires depuis le bureau ou travaillez sans effort en déplacement. Aucune installation ou logiciel supplémentaire requis. Toutes les fonctionnalités sont disponibles en ligne, il suffit d'aller sur signnow.com et de créer votre propre flux de signature électronique.

Guide rapide pour signer Accord de couverture en quelques minutes

- Créez un compte airSlate SignNow (si vous ne vous êtes pas encore inscrit) ou connectez-vous avec votre Google ou Facebook.

- Cliquez sur Télécharger et sélectionnez l'un de vos documents.

- Utilisez l'outil Ma Signature pour créer votre signature unique.

- Transformez le document en un PDF dynamique avec des champs remplissables.

- Remplissez votre nouveau formulaire et cliquez sur Terminé.

Une fois terminé, envoyez une invitation à signer à plusieurs destinataires. Obtenez un contrat exécutoire en quelques minutes avec n'importe quel appareil. Explorez plus de fonctionnalités pour créer des PDF professionnels ; ajoutez des champs remplissables, signez Accord de couverture et collaborez en équipe. La solution de signature électronique offre un flux de travail sécurisé et fonctionne selon la certification SOC 2 Type II. Assurez-vous que vos données sont protégées et qu'aucune personne ne peut les modifier.

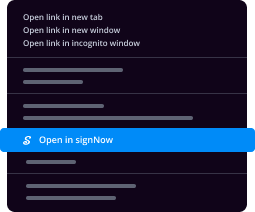

Comment eSigner un PDF dans Google Chrome

Vous cherchez une solution pour signer Accord de couverture directement depuis Chrome ? L'extension airSlate SignNow pour Google est là pour vous aider. Trouvez un document et, directement depuis votre navigateur, ouvrez-le facilement dans l'éditeur. Ajoutez des champs remplissables pour le texte et la signature. Signez le PDF et partagez-le en toute sécurité conformément au RGPD, à la certification SOC 2 Type II et plus encore.

En utilisant ce guide rapide ci-dessous, étendez votre flux de signature électronique dans Google et signez Accord de couverture :

- Allez sur le Chrome Web Store et trouvez l'extension airSlate SignNow.

- Cliquez sur Ajouter à Chrome.

- Connectez-vous à votre compte ou inscrivez-vous en un nouveau.

- Téléchargez un document et cliquez sur Ouvrir dans airSlate SignNow.

- Modifiez le document.

- Signez le PDF en utilisant l'outil Ma Signature.

- Cliquez sur Terminé pour enregistrer vos modifications.

- Invitez d'autres participants à signer en cliquant sur Inviter à Signer et en sélectionnant leurs e-mails/noms.

Créez une signature intégrée à votre flux de travail pour signer Accord de couverture et obtenir des PDFs signés électroniquement en quelques minutes. Dites adieu aux piles de papiers sur votre bureau et commencez à économiser de l'argent et du temps pour des tâches plus importantes. Choisir l'extension Google airSlate SignNow est une excellente option pratique avec de nombreux avantages.

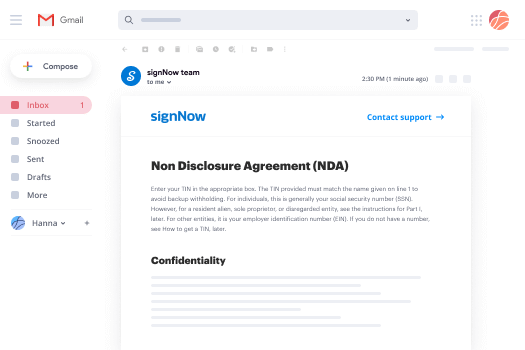

Comment signer une pièce jointe dans Gmail

Si vous êtes comme la plupart, vous avez l'habitude de télécharger les pièces jointes que vous recevez, de les imprimer puis de les signer, n'est-ce pas ? Bonne nouvelle : signer des documents dans votre boîte mail devient beaucoup plus facile. L'add-on airSlate SignNow pour Gmail vous permet de signer Accord de couverture sans quitter votre boîte de réception. Faites tout ce dont vous avez besoin ; ajoutez des champs remplissables et envoyez des demandes de signature en quelques clics.

Comment signer Accord de couverture dans Gmail :

- Trouvez airSlate SignNow pour Gmail dans le G Suite Marketplace et cliquez sur Installer.

- Connectez-vous à votre compte airSlate SignNow ou créez-en un nouveau.

- Ouvrez votre e-mail avec le PDF que vous devez signer.

- Cliquez sur Télécharger pour enregistrer le document dans votre compte airSlate SignNow.

- Cliquez sur Ouvrir le document pour ouvrir l'éditeur.

- Signez le PDF en utilisant Ma Signature.

- Envoyez une demande de signature aux autres participants avec le bouton Envoyer pour Signature.

- Entrez leur e-mail et appuyez sur OK.

En conséquence, les autres participants recevront des notifications leur demandant de signer le document. Plus besoin de télécharger le PDF encore et encore, signez Accord de couverture en quelques clics. Cet add-on est adapté à ceux qui préfèrent travailler sur des choses plus importantes plutôt que de perdre du temps inutilement. Accélérez votre travail quotidien avec le service de signature électronique primé.

Comment eSigner un modèle PDF en déplacement sans application

Pour de nombreux produits, effectuer des transactions en déplacement signifie installer une application sur votre téléphone. Nous sommes heureux de dire qu'avec airSlate SignNow, nous avons rendu la signature en déplacement plus rapide et plus facile en éliminant le besoin d'une application mobile. Pour eSigner, ouvrez votre navigateur (n'importe quel navigateur mobile) et accédez directement à airSlate SignNow et à tous ses puissants outils de signature électronique. Modifiez des documents, signez Accord de couverture et plus encore. Aucune installation ou logiciel supplémentaire requis. Concluez votre transaction de n'importe où.

Consultez nos instructions étape par étape qui vous apprennent comment signer Accord de couverture.

- Ouvrez votre navigateur et allez sur signnow.com.

- Connectez-vous ou inscrivez-vous avec un nouveau compte.

- Téléchargez ou ouvrez le document que vous souhaitez signer.

- Ajoutez des champs remplissables pour le texte, la signature et la date.

- Tracez, tapez ou téléchargez votre signature.

- Cliquez sur Enregistrer et Fermer.

- Cliquez sur Inviter à Signer et entrez l'e-mail d'un destinataire si vous souhaitez que d'autres signent le PDF.

Travailler sur mobile n'est pas différent de sur un ordinateur de bureau : créez un modèle réutilisable, signez Accord de couverture et gérez le flux comme vous le feriez normalement. En quelques clics, obtenez un contrat exécutoire que vous pouvez télécharger sur votre appareil et envoyer à d'autres. Cependant, si vous souhaitez vraiment une application, téléchargez l'application mobile airSlate SignNow. Elle est sécurisée, rapide et dispose d'une excellente mise en page. Expérimentez des flux de signature électronique faciles depuis votre lieu de travail, dans un taxi ou dans un avion.

Comment signer un PDF avec un iPad

iOS est un système d'exploitation très populaire doté d'outils natifs. Il vous permet de signer et d'éditer des PDFs en utilisant Aperçu sans logiciel supplémentaire. Cependant, aussi géniale que soit la solution d'Apple, elle ne propose pas d'automatisation. Améliorez les capacités de votre iPhone en utilisant l'application airSlate SignNow. Utilisez votre iPhone ou iPad pour signer Accord de couverture et plus encore. Introduisez l'automatisation de la signature électronique dans votre flux de travail mobile.

Signer sur un iPhone n'a jamais été aussi facile :

- Trouvez l'application airSlate SignNow dans l'App Store et installez-la.

- Créez un nouveau compte ou connectez-vous avec votre Facebook ou Google.

- Cliquez sur Plus et téléchargez le fichier PDF que vous souhaitez signer. li>Tapez sur le document à l'endroit où vous souhaitez insérer votre signature.

- Explorez d'autres fonctionnalités : ajoutez des champs remplissables ou signez Accord de couverture.

- Utilisez le bouton Enregistrer pour appliquer les modifications.

- Partagez vos documents par e-mail ou lien de signature.

Créez des PDFs professionnels directement depuis votre application airSlate SignNow. Optimisez votre temps et travaillez de n'importe où ; à la maison, au bureau, dans un bus ou un avion, et même à la plage. Gérez un flux de documents complet sans effort : générez des modèles réutilisables, signez Accord de couverture et travaillez sur des fichiers PDF avec des partenaires commerciaux. Transformez votre appareil en une entreprise très efficace pour exécuter des transactions.

Comment signer un fichier PDF avec un Android

Pour les utilisateurs Android, pour gérer des documents depuis leur téléphone, ils doivent installer un logiciel supplémentaire. Le Play Market est vaste et regorge d'options, donc trouver une bonne application n'est pas trop difficile si vous avez le temps de parcourir des centaines d'applications. Pour gagner du temps et éviter la frustration, nous suggérons airSlate SignNow pour Android. Stockez et modifiez des documents, créez des rôles de signature, et même signez Accord de couverture.

Les 9 étapes simples pour optimiser votre flux de travail mobile :

- Ouvrez l'application.

- Connectez-vous avec vos comptes Facebook ou Google ou inscrivez-vous si vous ne l'avez pas encore fait.

- Cliquez sur + pour ajouter un nouveau document en utilisant votre caméra, stockage interne ou cloud.

- Tapez n'importe où sur votre PDF et insérez votre eSignature.

- Cliquez sur OK pour confirmer et signer.

- Essayez plus de fonctionnalités d'édition ; ajoutez des images, signez Accord de couverture, créez un modèle réutilisable, etc.

- Cliquez sur Enregistrer pour appliquer les modifications une fois terminé.

- Téléchargez le PDF ou partagez-le par e-mail.

- Utilisez la fonction Inviter à signer si vous souhaitez définir et envoyer un ordre de signature aux destinataires.

Transformez la routine en quelque chose de simple et fluide avec l'application airSlate SignNow pour Android. Signez et envoyez des documents pour signature depuis n'importe quel endroit connecté à Internet. Créez des PDFs professionnels et signez Accord de couverture en quelques clics. Créez un processus de signature électronique impeccable avec seulement votre smartphone et augmentez votre productivité globale.

Obtenez des signatures juridiquement contraignantes dès maintenant !

FAQ

-

Comment fonctionne la couverture?

La couverture fait référence à l'achat d'un investissement conçu pour réduire le risque de pertes d'un autre investissement. Les investisseurs achèteront souvent un investissement opposé pour ce faire, comme en utilisant une option de vente pour se couvrir contre les pertes dans une position boursière, car une perte dans l'action sera en quelque sorte compensée par un gain dans l'option. -

Qu'est-ce que la couverture en termes simples?

Signification de la couverture. La couverture, en finance, est une stratégie de gestion des risques. Elle consiste à réduire ou éliminer le risque d'incertitude. ... En termes simples, il s'agit de couvrir un investissement en investissant dans un autre investissement. En général, lorsque les gens prévoient de couvrir, ils essaient de se protéger contre un événement négatif. -

Que signifie la couverture?

Une stratégie de gestion des risques utilisée pour limiter ou compenser la probabilité de perte due aux fluctuations des prix des matières premières, des devises ou des titres. En effet, la couverture est un transfert de risque sans achat de polices d'assurance. -

Que signifie la couverture en finance?

Couvrir le risque d'investissement signifie utiliser stratégiquement des instruments financiers ou des stratégies de marché pour compenser le risque de mouvements de prix défavorables. ... Donc, la couverture, pour la plupart, n'est pas une technique pour gagner de l'argent mais pour réduire la perte potentielle. -

Qu'est-ce qu'un accord de couverture?

Un accord de couverture désigne tout swap, plafond, collerette, achat à terme ou accords ou arrangements similaires traitant des taux d'intérêt, des taux de change ou des prix des matières premières, généralement ou sous des contingences spécifiques. Sur la base de 148 documents 148. \uff0b Nouvelle liste. -

Quelles sont les activités de couverture?

La couverture est une stratégie de gestion des risques employée pour compenser les pertes dans les investissements. La réduction du risque entraîne généralement une réduction des profits potentiels. Les stratégies de couverture impliquent généralement des dérivés, tels que des options et des contrats à terme. -

Que signifie couvrir un prêt?

Couvrir le risque d'investissement signifie utiliser stratégiquement des instruments financiers ou des stratégies de marché pour compenser le risque de mouvements de prix défavorables. ... Donc, la couverture, pour la plupart, n'est pas une technique pour gagner de l'argent mais pour réduire la perte potentielle. -

Comment utiliser le mot hedge dans une phrase?

Terminez la taille de tous les arbres à feuilles caduques et haies dès que possible. ... Les haies sont de FIG. anglaise. ... Il est souvent taillé de manière à former des haies dans les jardins. ... Des haies plus petites peuvent être formées de buis à feuilles persistantes ou de buissons d'arbres. ... Lors de la coupe, la haie (ainsi que toutes les haies) doit être XVI. -

Comment les fonds spéculatifs gagnent-ils de l'argent?

Un fonds spéculatif gagne de l'argent en facturant des frais de gestion et des frais de performance. Bien que ces frais diffèrent selon le fonds, ils tournent généralement autour de 2% et 20% des actifs sous gestion. Frais de gestion : Ces frais sont calculés en pourcentage des actifs sous gestion. ... Cette prime incite le fonds à générer des rendements excessifs. -

Pourquoi l'ISDA est-elle un accord-cadre?

L'Accord-cadre ISDA est le contrat standard utilisé pour régir toutes les transactions de dérivés de gré à gré (OTC) conclues entre les parties. ... Le but de l'Accord-cadre ISDA est de définir les dispositions régissant la relation globale des parties1. -

Comment couvrir le USD?

Empruntez la devise étrangère pour un montant équivalent à la valeur actuelle du receveur. ... Convertissez la devise étrangère en devise nationale au taux de change au comptant. Placez la devise nationale en dépôt à taux d'intérêt en vigueur.