Fill and Sign the State of Hawaii Tax Form G 45 2015

Convenient instructions on preparing your ‘State Of Hawaii Tax Form G 45 2015’ online

Are you fed up with the complications of handling paperwork? Look no further than airSlate SignNow, the premier eSignature solution for individuals and businesses. Bid farewell to the monotonous task of printing and scanning documents. With airSlate SignNow, you can easily fill out and approve documents online. Utilize the robust features embedded in this user-friendly and cost-effective platform and transform your method of document management. Whether you need to approve forms or collect electronic signatures, airSlate SignNow manages everything seamlessly, needing just a few clicks.

Follow this detailed guide:

- Sign in to your account or sign up for a free trial with our service.

- Click +Create to upload a file from your device, cloud, or our form library.

- Open your ‘State Of Hawaii Tax Form G 45 2015’ in the editor.

- Click Me (Fill Out Now) to set up the document on your end.

- Add and designate fillable fields for other participants (if necessary).

- Continue with the Send Invite settings to request eSignatures from others.

- Download, print your copy, or convert it into a reusable template.

Don’t worry if you need to collaborate with others on your State Of Hawaii Tax Form G 45 2015 or send it for notarization—our solution offers everything you require to complete such tasks. Register with airSlate SignNow today and elevate your document management to a new level!

FAQs

-

What is the State Of Hawaii Tax Form G 45?

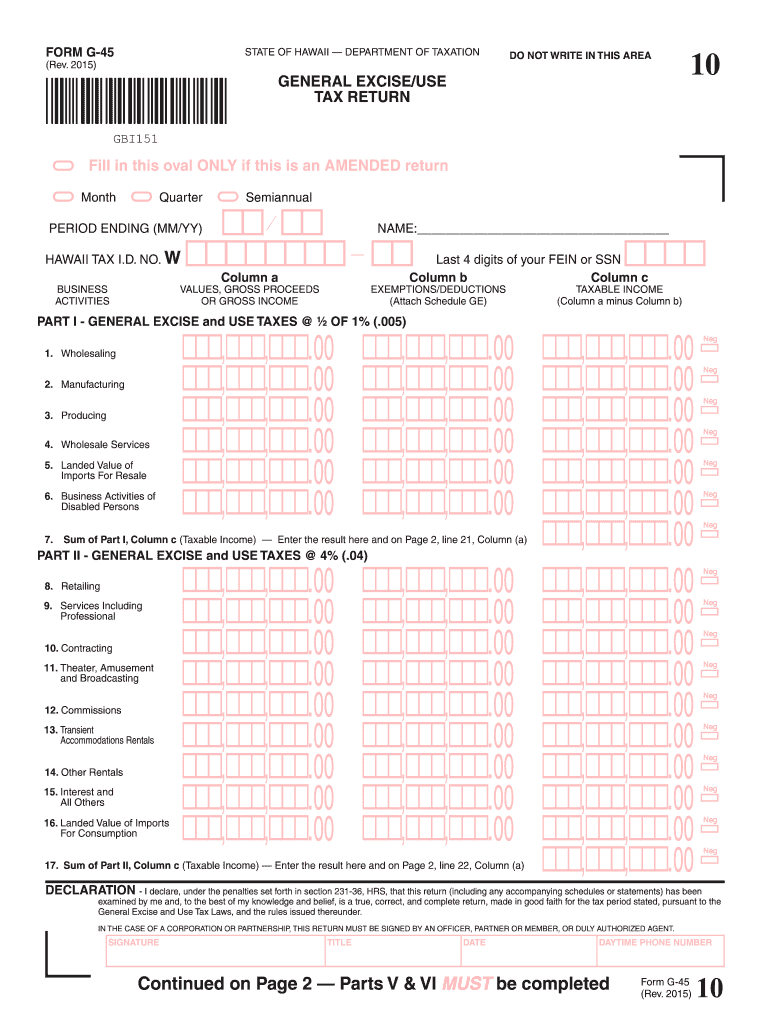

The State Of Hawaii Tax Form G 45 is a tax form used by businesses to report and pay their General Excise Tax (GET) to the Hawaii Department of Taxation. This form is essential for ensuring compliance with state tax regulations and is typically filed quarterly. By using airSlate SignNow, you can easily prepare and submit the State Of Hawaii Tax Form G 45 electronically, saving you time and reducing the risk of errors.

-

How can airSlate SignNow help with the State Of Hawaii Tax Form G 45?

airSlate SignNow provides a user-friendly platform that simplifies the process of completing and eSigning the State Of Hawaii Tax Form G 45. With features like customizable templates and secure cloud storage, you can efficiently manage your tax documents and ensure they are filed on time. Our solution also allows you to collaborate with your team, making it easier to gather necessary information for the form.

-

Is there a cost associated with using airSlate SignNow for the State Of Hawaii Tax Form G 45?

Yes, airSlate SignNow offers a range of pricing plans tailored to different business needs, which include features for managing the State Of Hawaii Tax Form G 45. Our plans are designed to be cost-effective, ensuring that businesses of all sizes can access the tools they need for efficient document management and eSigning. You can choose a plan that fits your budget while benefiting from our comprehensive solution.

-

Can I track the status of my State Of Hawaii Tax Form G 45 submission with airSlate SignNow?

Absolutely! With airSlate SignNow, you can easily track the status of your State Of Hawaii Tax Form G 45 submission in real-time. Our platform provides notifications and updates, so you always know when your documents are viewed, signed, and submitted. This feature helps you maintain transparency and ensures that you stay on top of your tax filing deadlines.

-

What integrations does airSlate SignNow offer for the State Of Hawaii Tax Form G 45?

airSlate SignNow integrates seamlessly with various accounting and tax software, allowing for a smooth workflow when handling the State Of Hawaii Tax Form G 45. You can connect with popular applications like QuickBooks and Xero to import data directly into the form, minimizing manual entry and reducing errors. This integration enhances your overall efficiency in managing tax documents.

-

Are there templates available for the State Of Hawaii Tax Form G 45 in airSlate SignNow?

Yes, airSlate SignNow provides ready-to-use templates for the State Of Hawaii Tax Form G 45, making it easier for you to get started. These templates are designed to comply with state requirements and can be customized to fit your specific business needs. By using our templates, you can save time and ensure that your tax form is completed accurately.

-

What security measures does airSlate SignNow have for the State Of Hawaii Tax Form G 45?

airSlate SignNow prioritizes the security of your documents, including the State Of Hawaii Tax Form G 45, by employing industry-standard encryption and secure cloud storage. We ensure that your sensitive tax information is protected at all times. Additionally, our platform includes features like user authentication and audit trails to further enhance document security.

Find out other state of hawaii tax form g 45 2015

- Close deals faster

- Improve productivity

- Delight customers

- Increase revenue

- Save time & money

- Reduce payment cycles