Realize Signed Order with airSlate SignNow

Award-winning eSignature solution

Do more online with a globally-trusted eSignature platform

Remarkable signing experience

Robust reports and analytics

Mobile eSigning in person and remotely

Industry regulations and conformity

Realize signed order, faster than ever

Handy eSignature extensions

See airSlate SignNow eSignatures in action

airSlate SignNow solutions for better efficiency

Our user reviews speak for themselves

Why choose airSlate SignNow

-

Free 7-day trial. Choose the plan you need and try it risk-free.

-

Honest pricing for full-featured plans. airSlate SignNow offers subscription plans with no overages or hidden fees at renewal.

-

Enterprise-grade security. airSlate SignNow helps you comply with global security standards.

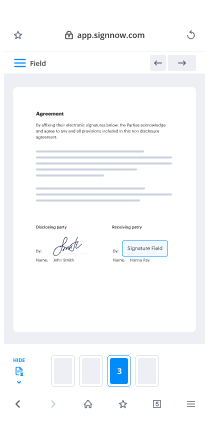

Your step-by-step guide — realize signed order

Leveraging airSlate SignNow’s eSignature any organization can increase signature workflows and eSign in real-time, supplying an improved experience to clients and employees. realize signed order in a couple of simple actions. Our mobile apps make working on the move possible, even while off-line! Sign signNows from anywhere in the world and make trades faster.

Take a step-by-step guideline to realize signed order:

- Sign in to your airSlate SignNow profile.

- Find your needed form in your folders or import a new one.

- the template and edit content using the Tools list.

- Place fillable fields, type text and sign it.

- Add numerous signers using their emails and set up the signing sequence.

- Indicate which recipients can get an executed doc.

- Use Advanced Options to reduce access to the template add an expiry date.

- Press Save and Close when finished.

In addition, there are more advanced capabilities available to realize signed order. Include users to your shared work enviroment, browse teams, and monitor collaboration. Millions of people all over the US and Europe recognize that a solution that brings everything together in one unified workspace, is exactly what enterprises need to keep workflows working effortlessly. The airSlate SignNow REST API enables you to embed eSignatures into your app, internet site, CRM or cloud. Check out airSlate SignNow and enjoy quicker, smoother and overall more productive eSignature workflows!

How it works

airSlate SignNow features that users love

See exceptional results realize signed order with airSlate SignNow

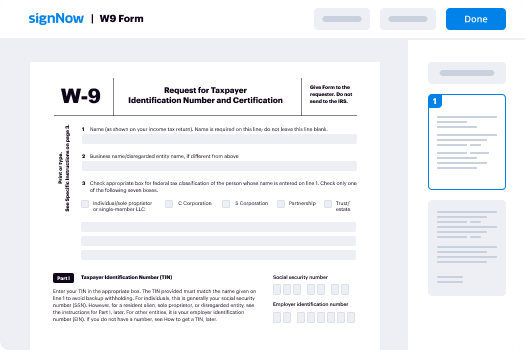

How to submit and eSign a PDF online

Try out the fastest way to realize signed order. Avoid paper-based workflows and manage documents right from airSlate SignNow. Complete and share your forms from the office or seamlessly work on-the-go. No installation or additional software required. All features are available online, just go to signnow.com and create your own eSignature flow.

A brief guide on how to realize signed order in minutes

- Create an airSlate SignNow account (if you haven’t registered yet) or log in using your Google or Facebook.

- Click Upload and select one of your documents.

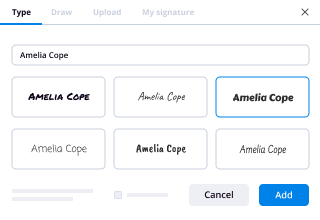

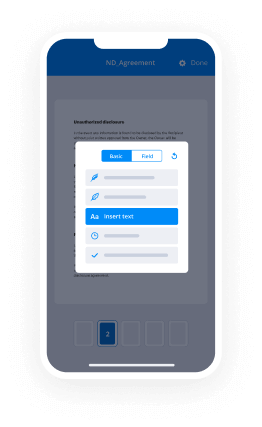

- Use the My Signature tool to create your unique signature.

- Turn the document into a dynamic PDF with fillable fields.

- Fill out your new form and click Done.

Once finished, send an invite to sign to multiple recipients. Get an enforceable contract in minutes using any device. Explore more features for making professional PDFs; add fillable fields realize signed order and collaborate in teams. The eSignature solution gives a secure workflow and operates based on SOC 2 Type II Certification. Ensure that your information are guarded and that no one can change them.

How to eSign a PDF in Google Chrome

Are you looking for a solution to realize signed order directly from Chrome? The airSlate SignNow extension for Google is here to help. Find a document and right from your browser easily open it in the editor. Add fillable fields for text and signature. Sign the PDF and share it safely according to GDPR, SOC 2 Type II Certification and more.

Using this brief how-to guide below, expand your eSignature workflow into Google and realize signed order:

- Go to the Chrome web store and find the airSlate SignNow extension.

- Click Add to Chrome.

- Log in to your account or register a new one.

- Upload a document and click Open in airSlate SignNow.

- Modify the document.

- Sign the PDF using the My Signature tool.

- Click Done to save your edits.

- Invite other participants to sign by clicking Invite to Sign and selecting their emails/names.

Create a signature that’s built in to your workflow to realize signed order and get PDFs eSigned in minutes. Say goodbye to the piles of papers on your desk and start saving money and time for more important activities. Picking out the airSlate SignNow Google extension is a smart handy choice with many different benefits.

How to eSign an attachment in Gmail

If you’re like most, you’re used to downloading the attachments you get, printing them out and then signing them, right? Well, we have good news for you. Signing documents in your inbox just got a lot easier. The airSlate SignNow add-on for Gmail allows you to realize signed order without leaving your mailbox. Do everything you need; add fillable fields and send signing requests in clicks.

How to realize signed order in Gmail:

- Find airSlate SignNow for Gmail in the G Suite Marketplace and click Install.

- Log in to your airSlate SignNow account or create a new one.

- Open up your email with the PDF you need to sign.

- Click Upload to save the document to your airSlate SignNow account.

- Click Open document to open the editor.

- Sign the PDF using My Signature.

- Send a signing request to the other participants with the Send to Sign button.

- Enter their email and press OK.

As a result, the other participants will receive notifications telling them to sign the document. No need to download the PDF file over and over again, just realize signed order in clicks. This add-one is suitable for those who like focusing on more significant goals rather than wasting time for absolutely nothing. Improve your daily monotonous tasks with the award-winning eSignature platform.

How to eSign a PDF on the go without an app

For many products, getting deals done on the go means installing an app on your phone. We’re happy to say at airSlate SignNow we’ve made singing on the go faster and easier by eliminating the need for a mobile app. To eSign, open your browser (any mobile browser) and get direct access to airSlate SignNow and all its powerful eSignature tools. Edit docs, realize signed order and more. No installation or additional software required. Close your deal from anywhere.

Take a look at our step-by-step instructions that teach you how to realize signed order.

- Open your browser and go to signnow.com.

- Log in or register a new account.

- Upload or open the document you want to edit.

- Add fillable fields for text, signature and date.

- Draw, type or upload your signature.

- Click Save and Close.

- Click Invite to Sign and enter a recipient’s email if you need others to sign the PDF.

Working on mobile is no different than on a desktop: create a reusable template, realize signed order and manage the flow as you would normally. In a couple of clicks, get an enforceable contract that you can download to your device and send to others. Yet, if you want a software, download the airSlate SignNow app. It’s secure, fast and has a great interface. Enjoy easy eSignature workflows from your office, in a taxi or on a plane.

How to sign a PDF file having an iPhone

iOS is a very popular operating system packed with native tools. It allows you to sign and edit PDFs using Preview without any additional software. However, as great as Apple’s solution is, it doesn't provide any automation. Enhance your iPhone’s capabilities by taking advantage of the airSlate SignNow app. Utilize your iPhone or iPad to realize signed order and more. Introduce eSignature automation to your mobile workflow.

Signing on an iPhone has never been easier:

- Find the airSlate SignNow app in the AppStore and install it.

- Create a new account or log in with your Facebook or Google.

- Click Plus and upload the PDF file you want to sign.

- Tap on the document where you want to insert your signature.

- Explore other features: add fillable fields or realize signed order.

- Use the Save button to apply the changes.

- Share your documents via email or a singing link.

Make a professional PDFs right from your airSlate SignNow app. Get the most out of your time and work from anywhere; at home, in the office, on a bus or plane, and even at the beach. Manage an entire record workflow effortlessly: create reusable templates, realize signed order and work on PDFs with business partners. Turn your device right into a effective organization tool for closing deals.

How to sign a PDF using an Android

For Android users to manage documents from their phone, they have to install additional software. The Play Market is vast and plump with options, so finding a good application isn’t too hard if you have time to browse through hundreds of apps. To save time and prevent frustration, we suggest airSlate SignNow for Android. Store and edit documents, create signing roles, and even realize signed order.

The 9 simple steps to optimizing your mobile workflow:

- Open the app.

- Log in using your Facebook or Google accounts or register if you haven’t authorized already.

- Click on + to add a new document using your camera, internal or cloud storages.

- Tap anywhere on your PDF and insert your eSignature.

- Click OK to confirm and sign.

- Try more editing features; add images, realize signed order, create a reusable template, etc.

- Click Save to apply changes once you finish.

- Download the PDF or share it via email.

- Use the Invite to sign function if you want to set & send a signing order to recipients.

Turn the mundane and routine into easy and smooth with the airSlate SignNow app for Android. Sign and send documents for signature from any place you’re connected to the internet. Generate professional-looking PDFs and realize signed order with a few clicks. Assembled a flawless eSignature process with just your mobile phone and boost your overall productivity.

Get legally-binding signatures now!

FAQs

-

Does a court order have to be signed?

A court order must be signed by a judge; some jurisdictions may also require it to be signNowd. ... Most orders are written, and are signed by the judge. Some orders, however, are spoken orally by the judge in open court, and are only reduced to writing in the transcript of the proceedings. -

What makes a court order invalid?

The Court order is invalid because the court had no authority to act (subject matter jurisdiction), or you were not served with legal notice in the original case (personal jurisdiction). -

What is the difference between a ruling and an order?

As nouns the difference between order and ruling is that order is (uncountable) arrangement, disposition, sequence while ruling is an order or a decision on a point of law from someone in authority. -

What do you do if your ex doesn't follow a court order?

Filing an Enforcement Motion It is up to you to inform the court of your ex's violation of the order, and to petition the court to force your ex to comply. Some states call this an \u201cenforcement motion,\u201d while others refer to this as a \u201cmotion of contempt.\u201d Your ex will receive a notice of the motion and a court date. -

What happens if you violate a temporary custody order?

First, since the arrangement is essentially a court order, violating a child custody or visitation agreement can lead to contempt of court issues. This can result in consequences including possible criminal penalties such as fines or jail time. -

How long does it take a judge to sign a proposed order?

The California rules of court do not require proposed orders be submitted until five days after the hearing. However, it remains best practice to bring a copy with you, to better get the judge's confirmation and file it on opposing party within the deadline. -

How long does a judge have to answer a motion?

Any party may file a response to a motion; Rule 27(a)(2) governs its contents. The response must be filed within 10 days after service of the motion unless the court shortens or extends the time. -

Can a judge refuse to hear a motion?

Motions must be made in writing and they must follow certain criteria, including things like notice requirements. ... If the Motions do not meet procedural requirements, then the clerk may refuse to file them or the Judge may refuse to hear them. -

What does proposed order mean in court?

First, a proposed Order is something that you attach to a brief or a motion or petition where you are asking the Court to grant some type of relief that you are requesting. -

What does order in the court mean?

A court order is an official proclamation by a judge (or panel of judges) that defines the legal relationships between the parties to a hearing, a trial, an appeal or other court proceedings. Such ruling requires or authorizes the carrying out of certain steps by one or more parties to a case. -

How do you know if you have a restraining order on you?

Give them your name and date of birth and ask if you have a restraining order. Or, go down to the local law enforcement office with your ID and ask them. If there is a restraining order placed against you, you must be notified of said restraint. -

Can I find out if someone has a restraining order against them?

First search online for the county or state's court website to see if they have information on whether or not there's a restraining order open against you. If you cannot access the information online, visit or call your county office and have someone in the office help you conduct the search. -

Is a protection order public record?

Yes. A restraining order will appear on your criminal record. Although a restraining order is a civil order, whenever someone runs your record for probation, employment, or immigration purposes, it will show that someone had or has a restraining order against you. -

How are you notified of a restraining order?

Normal restraining orders. Since the defendant is usually present at the hearing, they are considered notified. If they don't show up for the hearing, then they will be notified \u2014 again, usually by the sheriff \u2014 of the courts decision. Both parties will generally get a mail notification as well, for their records. -

Do restraining orders come in the mail?

Serve your signNows on the restrained person Have someone \u201cserve\u201d (give) the restrained person a copy of the order and other signNows you filed. The signNows must be delivered in person. You cannot send them by mail.

What active users are saying — realize signed order

Related searches to realize signed order with airSlate airSlate SignNow

Realize signed order

so we're coming to the end of 2020 and starting 2021. things are going back to normal for a lot of people but there's still a lot of uncertainty specifically around forbearances and mortgages i'm going to explain to you what the difference is between a federally backed and a private lender mortgage and how it affects you when the forbearance has come to an end many people do not realize that all the federal laws that are currently in place to protect people due to the coronavirus only apply to a certain number of mortgages not to all the mortgages in the united states i'm going to explain to you what the differences are and how you can come out of the forbearance without losing your home my name is diego mendez i'm a bankruptcy low modification foreclosure lawyer here in miami florida i was around in 2008 for the last crash and i've seen a lot of the same things going on this time around that were happening back then i created this channel on youtube to help people avoid financial ruin that i saw in the last crash please subscribe to my channel because i'm going to be making more and more of these videos relating to loan modifications forbearances and other types of government assistance relating to mortgages so as i explained we are entering into a time of uncertainty the end of the forbearance periods brings a lot of stress for people because we're not sure what's going to happen at the end i can explain to you what certain types of mortgage companies are going to do at the end of the forbearance and what other types of mortgage companies are going to do but you need to understand one thing as a lot of people have realized we are living in two americas now i'm not talking blue state red state or anything related to that kind of political talk uh what i'm talking about is that there are two types of mortgages in the united states there are federally backed and private lender mortgages depending on what kind of mortgage you have is what's going to happen with you at the end of the forbearance period the people who have federally backed mortgages are going to have a much easier time dealing with the end of the forbearance than people who have non-federally backed private lender type mortgages i'm going to explain to the difference right now so you understand where you are in the spectrum of mortgages and how you can use this information to your benefit now the biggest difference between federally backed and non-federally backed private lenders are that the federally backed obviously are guaranteed by the government and the government can control what these lenders do the only federally backed mortgages that exist in the united states are fha va usda fannie mae and freddie mac you don't necessarily get a bill from these companies or these entities you will get a bill from another servicing company that services these loans but these are the ones that are federally backed you know if you have a federally backed mortgage they've already reached out to you they've already explained your options they've told you the different things you can do the biggest thing with these type of mortgages for you to understand when the forbearances end that there's no lump sum requirement you're not required to come up with 10 or 12 or 15 or 18 months of back payments in one lump sum that's the biggest benefit i've done other videos which i explained the different options for these type of mortgages when you come out i'm going to put the link up there you can link to the other video and watch them if you have this type of mortgage but the biggest thing you need to understand is that this type of mortgage does not require lump sum that's the biggest benefit and the thing you have that on your side when you're dealing with this type of mortgage now the problem is that 40 percent of the united states has something called a private lender mortgage these type of lenders i'm not saying they're all bad and i'm not making any generalizations in terms of what they're doing because i'm not sure exactly what each one of them will do into the future the biggest difference between these lenders and the ones i mentioned before is that these lenders are not covered by the cares act nor are they covered by any of the other coronavirus related legislation and presidential executive orders that have been signed these lenders can do whatever they want with their customers if you do not pay them they are able to ask for whatever terms you agree to when you sign the mortgage that means these lenders can ask you for lump sum or short fast repayments when you come out of forbearance it's very very important that when you come out of forbearance and you have any of these lenders and others that you're very clear with them as to what you can do and hopefully they have some option for you to pay back what you owe either in a short term or at the back end or some other form of assistance for you remember private lenders are not covered by the cares act you have limited protections when you're dealing with a private lender a private lender can ask for a lump sum at the end of forbearance so when you enter into a forbearance make sure that you understand what the lender expects from you at the end it feels really nice to not have to pay mortgage for three or four months or six months but it feels really bad have to come up with 12 000 or 20 000 in a lump sum at the end a lot of times the consumer finds themselves in a foreclosure situation at the end of the forbearance because they cannot come up with a lump sum or the short repayment of six months or one year even for the amount of money that they didn't pay during the forbearance period be sure that if you do not have a federally backed mortgage which are the ones that i listed in this document here these companies have their own rules i'm not saying that they're going to foreclose immediately i'm sure they're doing something for their customers but they are not bound by any other legislation or the executive orders that are currently being considered signed by this administration or the previous administration so make sure that if you have penny map quicken loans home bridge and any of the other ones that are out there that you're talking to them constantly and that everything that they send you you're paying attention to because you do not want a surprise bill of 25 000 at the end of your forbearance because if you couldn't come up with it for the year that you run forbearance it's highly unlikely that you're going to be able to come up with it at the end so be very very careful with these lenders be sure to communicate with your lender be sure to call them and ask them what can i do at the end of the forbearance what do you expect from me it's very important that you communicate with them there are options like loan modifications and some other options that you might want to consider if you're unable to come up with a lump sum that these lenders might require you to come up with be sure that you understand what they're offering be sure that you apply for whatever assistance they have pay attention to what they send you in the mail and be very very vigilant do not trust your instincts do not trust the things that you hear on television or that people tell you over the phone only read what they mail to you and pay attention to that if you do not understand what they're sending you speak to somebody who does either an attorney or somebody who deals with this type of thing ask them to help you interpret what it is that they're offering you do not make the mistake of signing something that will then turn into a big problem for you a lot of people are going to lose their homes because of this so be very very vigilant and be very careful my name is diego mendez i'm a bankruptcy and loan modification and foreclosure lawyer here in miami florida i've helped thousands of people with these type of issues throughout the years i was around the last crash i was representing debtors and people in foreclosure at that time and i'm still doing it now i'm helping people right now it's getting very very busy for us but we're still helping people with this type of issue i'm gonna keep making these type of videos so that people understand their options and their legal rights in these situations please subscribe to my channel like my videos and i'll keep making videos so that everybody's informed and we all come out of this coronavirus mess together with our homes and hopefully with our sanity and our financial situation in order thank you very much

Show moreFrequently asked questions

What is needed for an electronic signature?

How do I make an electronic signature without a scanner?

How do I add an electronic signature to my document?

Get more for realize signed order with airSlate SignNow

- Print electronically sign Business Travel Itinerary

- Prove electronically signed Landscaping Services Contract Template

- Endorse digisign Construction Equipment Lease Proposal Template

- Authorize electronically sign draft

- Anneal mark Free Construction Contract

- Justify esign Freelance Web Design Proposal Template

- Try countersign Speaker Agreement Template – BaseCRM Version

- Add Assignment Agreement signed

- Send Website Quote Template digi-sign

- Fax Promotion Letter to Employee esign

- Seal Music Press Release initial

- Password Advertising Proposal Template signature

- Pass Licensing Agreement email signature

- Renew Web Design Contract digital signature

- Test Boy Scout Camp Physical Form electronically signed

- Require Subscription Agreement Template byline

- Comment proof countersignature

- Boost cosigner electronically sign

- Call for successor signed electronically

- Void Amendment to LLC Operating Agreement template autograph

- Adopt Support Agreement template digital sign

- Vouch Free Raffle Ticket template initial

- Establish Alabama Bill of Sale template electronically sign

- Clear Limousine Service Contract Template template countersignature

- Complete Pet Health Record template digital signature

- Force Design Invoice Template template mark

- Permit Income Verification Letter template signed

- Customize Photo Licensing Agreement template digi-sign