Signed Inquiry Made Easy

Award-winning eSignature solution

Do more online with a globally-trusted eSignature platform

Outstanding signing experience

Robust reporting and analytics

Mobile eSigning in person and remotely

Industry polices and compliance

Signed inquiry, faster than ever

Handy eSignature add-ons

See airSlate SignNow eSignatures in action

airSlate SignNow solutions for better efficiency

Our user reviews speak for themselves

Why choose airSlate SignNow

-

Free 7-day trial. Choose the plan you need and try it risk-free.

-

Honest pricing for full-featured plans. airSlate SignNow offers subscription plans with no overages or hidden fees at renewal.

-

Enterprise-grade security. airSlate SignNow helps you comply with global security standards.

Your step-by-step guide — signed inquiry

Using airSlate SignNow’s electronic signature any company can accelerate signature workflows and sign online in real-time, giving a greater experience to clients and workers. Use signed inquiry in a couple of simple actions. Our handheld mobile apps make working on the move feasible, even while offline! Sign signNows from anywhere in the world and close up tasks faster.

Take a stepwise instruction for using signed inquiry:

- Log on to your airSlate SignNow account.

- Locate your record in your folders or upload a new one.

- Open the record adjust using the Tools menu.

- Place fillable fields, add textual content and sign it.

- Add several signees via emails and set up the signing sequence.

- Choose which users will receive an signed doc.

- Use Advanced Options to limit access to the record add an expiry date.

- Tap Save and Close when completed.

In addition, there are more enhanced capabilities available for signed inquiry. Include users to your common workspace, browse teams, and keep track of teamwork. Numerous users across the US and Europe recognize that a system that brings everything together in one unified enviroment, is what businesses need to keep workflows functioning efficiently. The airSlate SignNow REST API allows you to integrate eSignatures into your application, website, CRM or cloud. Try out airSlate SignNow and get faster, easier and overall more efficient eSignature workflows!

How it works

airSlate SignNow features that users love

See exceptional results signed inquiry made easy

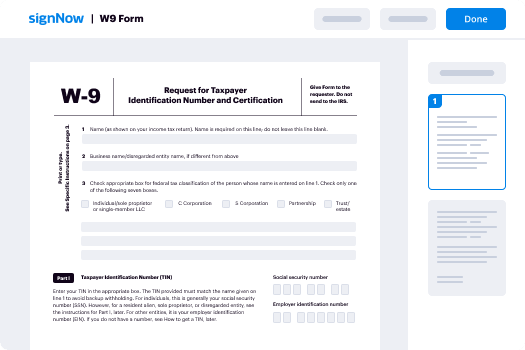

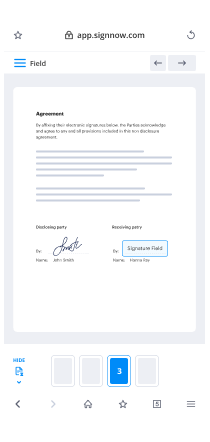

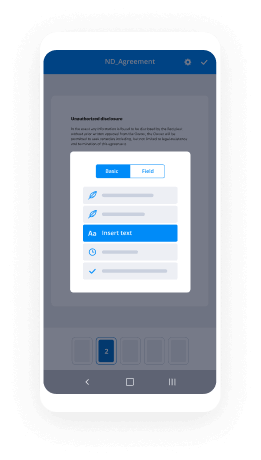

How to fill in and sign a document online

Try out the fastest way to signed inquiry. Avoid paper-based workflows and manage documents right from airSlate SignNow. Complete and share your forms from the office or seamlessly work on-the-go. No installation or additional software required. All features are available online, just go to signnow.com and create your own eSignature flow.

A brief guide on how to signed inquiry in minutes

- Create an airSlate SignNow account (if you haven’t registered yet) or log in using your Google or Facebook.

- Click Upload and select one of your documents.

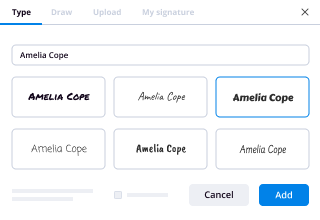

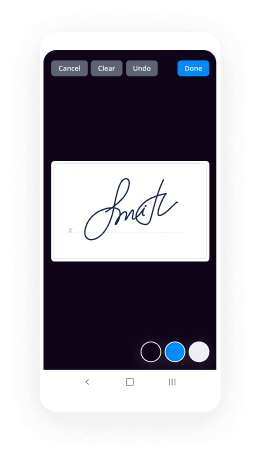

- Use the My Signature tool to create your unique signature.

- Turn the document into a dynamic PDF with fillable fields.

- Fill out your new form and click Done.

Once finished, send an invite to sign to multiple recipients. Get an enforceable contract in minutes using any device. Explore more features for making professional PDFs; add fillable fields signed inquiry and collaborate in teams. The eSignature solution supplies a protected process and functions in accordance with SOC 2 Type II Certification. Make sure that all of your records are protected and therefore no person can edit them.

How to eSign a PDF template in Google Chrome

Are you looking for a solution to signed inquiry directly from Chrome? The airSlate SignNow extension for Google is here to help. Find a document and right from your browser easily open it in the editor. Add fillable fields for text and signature. Sign the PDF and share it safely according to GDPR, SOC 2 Type II Certification and more.

Using this brief how-to guide below, expand your eSignature workflow into Google and signed inquiry:

- Go to the Chrome web store and find the airSlate SignNow extension.

- Click Add to Chrome.

- Log in to your account or register a new one.

- Upload a document and click Open in airSlate SignNow.

- Modify the document.

- Sign the PDF using the My Signature tool.

- Click Done to save your edits.

- Invite other participants to sign by clicking Invite to Sign and selecting their emails/names.

Create a signature that’s built in to your workflow to signed inquiry and get PDFs eSigned in minutes. Say goodbye to the piles of papers sitting on your workplace and begin saving money and time for extra important duties. Selecting the airSlate SignNow Google extension is a smart convenient decision with lots of advantages.

How to sign an attachment in Gmail

If you’re like most, you’re used to downloading the attachments you get, printing them out and then signing them, right? Well, we have good news for you. Signing documents in your inbox just got a lot easier. The airSlate SignNow add-on for Gmail allows you to signed inquiry without leaving your mailbox. Do everything you need; add fillable fields and send signing requests in clicks.

How to signed inquiry in Gmail:

- Find airSlate SignNow for Gmail in the G Suite Marketplace and click Install.

- Log in to your airSlate SignNow account or create a new one.

- Open up your email with the PDF you need to sign.

- Click Upload to save the document to your airSlate SignNow account.

- Click Open document to open the editor.

- Sign the PDF using My Signature.

- Send a signing request to the other participants with the Send to Sign button.

- Enter their email and press OK.

As a result, the other participants will receive notifications telling them to sign the document. No need to download the PDF file over and over again, just signed inquiry in clicks. This add-one is suitable for those who like focusing on more important goals rather than burning time for practically nothing. Improve your day-to-day monotonous tasks with the award-winning eSignature service.

How to sign a PDF template on the go with no mobile app

For many products, getting deals done on the go means installing an app on your phone. We’re happy to say at airSlate SignNow we’ve made singing on the go faster and easier by eliminating the need for a mobile app. To eSign, open your browser (any mobile browser) and get direct access to airSlate SignNow and all its powerful eSignature tools. Edit docs, signed inquiry and more. No installation or additional software required. Close your deal from anywhere.

Take a look at our step-by-step instructions that teach you how to signed inquiry.

- Open your browser and go to signnow.com.

- Log in or register a new account.

- Upload or open the document you want to edit.

- Add fillable fields for text, signature and date.

- Draw, type or upload your signature.

- Click Save and Close.

- Click Invite to Sign and enter a recipient’s email if you need others to sign the PDF.

Working on mobile is no different than on a desktop: create a reusable template, signed inquiry and manage the flow as you would normally. In a couple of clicks, get an enforceable contract that you can download to your device and send to others. Yet, if you really want a software, download the airSlate SignNow mobile app. It’s comfortable, fast and has an excellent interface. Take advantage of in effortless eSignature workflows from the business office, in a taxi or on an airplane.

How to sign a PDF file using an iPad

iOS is a very popular operating system packed with native tools. It allows you to sign and edit PDFs using Preview without any additional software. However, as great as Apple’s solution is, it doesn't provide any automation. Enhance your iPhone’s capabilities by taking advantage of the airSlate SignNow app. Utilize your iPhone or iPad to signed inquiry and more. Introduce eSignature automation to your mobile workflow.

Signing on an iPhone has never been easier:

- Find the airSlate SignNow app in the AppStore and install it.

- Create a new account or log in with your Facebook or Google.

- Click Plus and upload the PDF file you want to sign.

- Tap on the document where you want to insert your signature.

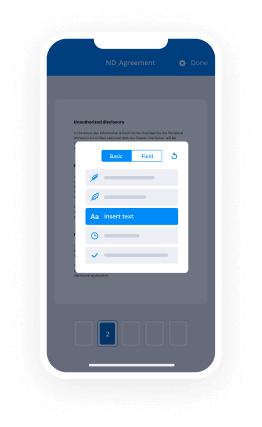

- Explore other features: add fillable fields or signed inquiry.

- Use the Save button to apply the changes.

- Share your documents via email or a singing link.

Make a professional PDFs right from your airSlate SignNow app. Get the most out of your time and work from anywhere; at home, in the office, on a bus or plane, and even at the beach. Manage an entire record workflow easily: create reusable templates, signed inquiry and work on documents with business partners. Transform your device right into a potent business for executing contracts.

How to eSign a PDF file taking advantage of an Android

For Android users to manage documents from their phone, they have to install additional software. The Play Market is vast and plump with options, so finding a good application isn’t too hard if you have time to browse through hundreds of apps. To save time and prevent frustration, we suggest airSlate SignNow for Android. Store and edit documents, create signing roles, and even signed inquiry.

The 9 simple steps to optimizing your mobile workflow:

- Open the app.

- Log in using your Facebook or Google accounts or register if you haven’t authorized already.

- Click on + to add a new document using your camera, internal or cloud storages.

- Tap anywhere on your PDF and insert your eSignature.

- Click OK to confirm and sign.

- Try more editing features; add images, signed inquiry, create a reusable template, etc.

- Click Save to apply changes once you finish.

- Download the PDF or share it via email.

- Use the Invite to sign function if you want to set & send a signing order to recipients.

Turn the mundane and routine into easy and smooth with the airSlate SignNow app for Android. Sign and send documents for signature from any place you’re connected to the internet. Build professional PDFs and signed inquiry with a few clicks. Put together a faultless eSignature process with just your smartphone and improve your total productiveness.

Get legally-binding signatures now!

FAQs

-

Can someone check your credit without your permission?

According to the federal Fair Credit Reporting Act, only those with a legitimate need can request \u2013 and obtain\u2013 a copy of your credit report. However, not all of them need your permission to view your credit reports. The great thing about your credit reports is that they show you who has accessed them. -

Is it illegal to run credit without authorization?

The Fair Credit Reporting Act (FCRA) has a strict limit on who can check your credit and under what circumstance. The law regulates credit reporting and ensures that only business entities with a specific, legitimate purpose, and not members of the general public, can check your credit without written permission. -

Can I sue for unauthorized credit check?

Legally, they have no right to do this unless they've obtained a court order. If they haven't, \u201cyou absolutely have the right to sue them as this violates the Fair Credit Reporting Act,\u201d says personal finance author David Bakke. -

Who can request my credit report?

The federal Fair Credit Reporting Act (FCRA) (15 U.S.C. ... According to the FRCA, the following people and entities can request your credit report: Creditors and potential creditors (including credit card issuers and car loan lenders). -

How do you pull someone's credit report?

Contact one of three credit reporting agencies. They are Equifax, Experian and TransUnion. Going through one of these agencies is the only legitimate way to obtain someone's credit report. The credit report lists detailed information about employment, credit history, previous tenancies and current debts. -

Can you check someone else's credit?

The short answer is yes. With the proper authority, anyone can obtain a copy of another person's credit report. The key here, though, is having what the Fair Credit Reporting Act refers to as \u201cpermissible purpose\u201d to access the report. -

Can I check my husbands credit report?

A: No, you can't check your spouse's (or ex's) personal credit reports. In order to request a consumer report on someone else, you must have what's called a \u201cpermissible purpose\u201d under federal law, and marriage or divorce is not one of them. -

Does Cosigning hurt your credit?

In a strict sense, the answer is no. The fact that you are a cosigner in and of itself does not necessarily hurt your credit. However, even if the cosigned account is paid on time, the debt may affect your credit scores and revolving utilization, which could affect your ability to get a loan in the future. -

Why you should never co sign?

At that point, you risk having to pay back money you didn't actually borrow yourself, or having your wages garnished if you can't make those payments. Furthermore, if you cosign a loan that the primary borrower falls behind on, you risk damaging your own credit score. -

Will Cosigning affect me buying a house?

Although you can still get a mortgage if you co-sign for someone else, you may have a harder time qualifying. That's due to the increased risk you present to a lender if you become responsible for payments on the co-signed loan. -

What credit score does a cosigner need?

Generally, a cosigner is only needed when your credit score or income may not be strong enough to meet a financial institution's underwriting guidelines. If you have a stronger credit score, typically 650 and above, along with sufficient income to cover the loan payment, it's likely you will not need a co-signer. -

Can you be denied a loan with a cosigner?

A cosigner promises payment if the borrower defaults on a loan. It provides an additional layer of insurance for the lender, but there's no obligation to accept a cosigner and the bank could deny you anyway. -

Can loan be denied after closing?

After Closing Although it's rare, it is even possible for your lender to pull a refinance loan after closing. Technically, your loan doesn't actually fund during the rescission period, so the lender could decide to not send the money. If you aren't in some form of default, though, this would be a bsignNow of contract. -

Can lender check credit after closing?

Here's the short answer: Most lenders who offer FHA loans will check your credit score at least twice. They do an initial pull shortly after you apply for financing, and they often do a second pull just before the scheduled closing day. ... Any major changes could potentially derail your loan. -

How soon can you apply for credit after closing?

Re: Applying for credit after closing. You can apply as soon as you close regardless of when you take possession. Your mortgage should have funded (by wire to the title company/ attorney) before you even signed so that the seller's funds can be disbursed.

What active users are saying — signed inquiry

Signed inquiry

this resolution maybe it's because i'm not a lawyer this resolution basically for me it is noting the contract duration and approving the terms and conditions yes now did you not approve the contract the the times and conditions of the contract then yes we appreciate you so how could you approve a contract that you did not know because you have said you don't know that contract i've just stopped you from going back to the 2012 contract now to remind you that miss softmayer is talking about the march 2016 contract now she has shown you a resolution you agree that you approved so how could you have approved a contract without knowing it i am considering that it is stated like this check if you say then i approved here that is fine let us continue no but the question remains how could you have approved a contract you did not know i didn't think that this is a contract i thought we were approving only the terms and conditions not the whole contract the whole contract would have the whole lot of mercury the price and everything and then the terms of conditions you are a chartered accountant you are a chartered accountant you have said you have you approved this contract initially you said you didn't know about this contract you are shown a resolution you accept that you you you approve the contract now what are you saying you say you don't know the contract you know the times and conditions i'm saying my knowledge of the contract sorry i'm saying my knowledge of the contract when miss hoffmayer is saying i am approving the contract the contract will start from page one up to the last page however the terms and conditions would be part of the contract not to the whole contract and therefore precisely because the terms and conditions of a contract are part of the contract it is precisely because of that that you should know the contract if you say you approve the terms and conditions what is perplexing is that you say you don't know the contract but you know the terms no i'm saying my understanding is that as i was saying the terms and conditions would be included as part of a bigger document that's what i understand that's number one number two these terms and conditions of this contract my understanding was that they were the terms and conditions of the contract that was ended many years ago so now when you are saying therefore the contract was entered into in march 2016 that means therefore here you are saying we were approving the terms and conditions of the contract that was entered into in march 2016 but now my question would be why would we approve only the terms and conditions instead of approving the whole contract i mean you can't know the terms and conditions of a contract without knowing the contract because the terms and conditions are the contract a contract has got terms and conditions and if you know the terms and conditions you know the contract isn't it i think we should continue miss miss do you accept what i'm saying that a contract consists of terms and conditions and if you know the terms and conditions it means you know the contract you accept that and other information sorry and other information yes but we're not talking about other information we talk about the terms and conditions i'm not talking about what's the address of the parties or the addresses of the parties to the contract we're talking about the terms and conditions do you accept that if you know the terms and conditions you therefore know the contract yes okay all right

Show moreFrequently asked questions

How can I eSign a contract?

How can I insert an electronic signature into a PDF?

How do I sign documents sent to my email?

Get more for signed inquiry made easy

- Print signature service Scholarship Certificate

- Prove electronically signing Pest Control Proposal Template

- Endorse digi-sign IT Consulting Agreement Template

- Authorize signature service Severance Agreement

- Anneal signatory Service Invoice

- Justify eSignature Photo Release Form

- Try initial UX Design Proposal Template

- Add Rights Agreement electronically signing

- Send Book Proposal Template mark

- Fax Simple Medical History signed

- Seal Website Evaluation autograph

- Password Equipment Lease digital sign

- Pass Event Photography Contract Template initial

- Renew Advance Directive electronically sign

- Test Basketball League Registration Event countersignature

- Require Property Management Agreement Template digital signature

- Comment patron signature block

- Boost caller esign

- Compel man digi-sign

- Void Business Requirements Document Template (BRD) template eSign

- Adopt warrant template eSignature

- Vouch Invoice Template for Translation template autograph

- Establish Parking Ticket template electronic signature

- Clear Salvage Agreement Template template signed electronically

- Complete Coronavirus Press Release template electronically sign

- Force Architectural Proposal Template template sign

- Permit Discount Voucher template electronically signing

- Customize Freelance Video Editing Contract Template template mark