Underwrite eSigning Request with airSlate SignNow

Award-winning eSignature solution

Improve your document workflow with airSlate SignNow

Agile eSignature workflows

Fast visibility into document status

Easy and fast integration set up

Underwrite esigning request on any device

Detailed Audit Trail

Rigorous protection requirements

See airSlate SignNow eSignatures in action

airSlate SignNow solutions for better efficiency

Our user reviews speak for themselves

Why choose airSlate SignNow

-

Free 7-day trial. Choose the plan you need and try it risk-free.

-

Honest pricing for full-featured plans. airSlate SignNow offers subscription plans with no overages or hidden fees at renewal.

-

Enterprise-grade security. airSlate SignNow helps you comply with global security standards.

Your step-by-step guide — underwrite esigning request

Employing airSlate SignNow’s electronic signature any organization can enhance signature workflows and sign online in real-time, delivering an improved experience to consumers and staff members. underwrite esigning Request in a couple of easy steps. Our handheld mobile apps make working on the move feasible, even while off-line! eSign contracts from any place in the world and close trades faster.

Take a walk-through guide to underwrite esigning Request:

- Log on to your airSlate SignNow account.

- Locate your document in your folders or import a new one.

- Open up the record and make edits using the Tools list.

- Drop fillable fields, add textual content and sign it.

- List several signers by emails and set the signing order.

- Specify which recipients will receive an signed doc.

- Use Advanced Options to restrict access to the document add an expiration date.

- Click Save and Close when done.

Furthermore, there are more extended capabilities open to underwrite esigning Request. Add users to your common digital workplace, browse teams, and track collaboration. Millions of people all over the US and Europe concur that a solution that brings everything together in a single unified workspace, is the thing that organizations need to keep workflows working effortlessly. The airSlate SignNow REST API enables you to embed eSignatures into your application, internet site, CRM or cloud. Try out airSlate SignNow and get faster, smoother and overall more efficient eSignature workflows!

How it works

airSlate SignNow features that users love

See exceptional results underwrite esigning Request with airSlate SignNow

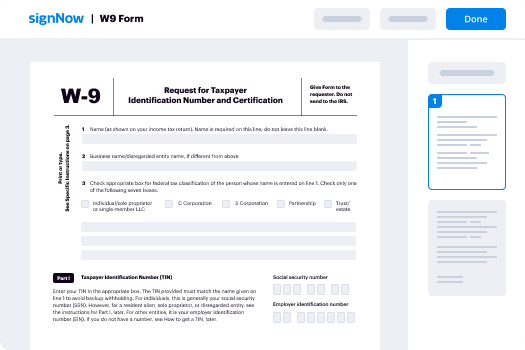

How to fill in and eSign a PDF online

Try out the fastest way to underwrite esigning Request. Avoid paper-based workflows and manage documents right from airSlate SignNow. Complete and share your forms from the office or seamlessly work on-the-go. No installation or additional software required. All features are available online, just go to signnow.com and create your own eSignature flow.

A brief guide on how to underwrite esigning Request in minutes

- Create an airSlate SignNow account (if you haven’t registered yet) or log in using your Google or Facebook.

- Click Upload and select one of your documents.

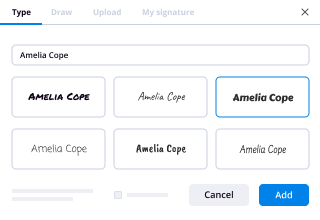

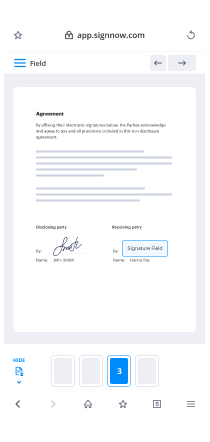

- Use the My Signature tool to create your unique signature.

- Turn the document into a dynamic PDF with fillable fields.

- Fill out your new form and click Done.

Once finished, send an invite to sign to multiple recipients. Get an enforceable contract in minutes using any device. Explore more features for making professional PDFs; add fillable fields underwrite esigning Request and collaborate in teams. The eSignature solution gives a secure workflow and functions in accordance with SOC 2 Type II Certification. Make sure that all your information are guarded so no one can edit them.

How to eSign a PDF template in Google Chrome

Are you looking for a solution to underwrite esigning Request directly from Chrome? The airSlate SignNow extension for Google is here to help. Find a document and right from your browser easily open it in the editor. Add fillable fields for text and signature. Sign the PDF and share it safely according to GDPR, SOC 2 Type II Certification and more.

Using this brief how-to guide below, expand your eSignature workflow into Google and underwrite esigning Request:

- Go to the Chrome web store and find the airSlate SignNow extension.

- Click Add to Chrome.

- Log in to your account or register a new one.

- Upload a document and click Open in airSlate SignNow.

- Modify the document.

- Sign the PDF using the My Signature tool.

- Click Done to save your edits.

- Invite other participants to sign by clicking Invite to Sign and selecting their emails/names.

Create a signature that’s built in to your workflow to underwrite esigning Request and get PDFs eSigned in minutes. Say goodbye to the piles of papers on your desk and start saving money and time for more crucial duties. Picking out the airSlate SignNow Google extension is an awesome practical choice with a lot of benefits.

How to eSign an attachment in Gmail

If you’re like most, you’re used to downloading the attachments you get, printing them out and then signing them, right? Well, we have good news for you. Signing documents in your inbox just got a lot easier. The airSlate SignNow add-on for Gmail allows you to underwrite esigning Request without leaving your mailbox. Do everything you need; add fillable fields and send signing requests in clicks.

How to underwrite esigning Request in Gmail:

- Find airSlate SignNow for Gmail in the G Suite Marketplace and click Install.

- Log in to your airSlate SignNow account or create a new one.

- Open up your email with the PDF you need to sign.

- Click Upload to save the document to your airSlate SignNow account.

- Click Open document to open the editor.

- Sign the PDF using My Signature.

- Send a signing request to the other participants with the Send to Sign button.

- Enter their email and press OK.

As a result, the other participants will receive notifications telling them to sign the document. No need to download the PDF file over and over again, just underwrite esigning Request in clicks. This add-one is suitable for those who like focusing on more significant aims as an alternative to wasting time for nothing. Improve your daily routine with the award-winning eSignature platform.

How to eSign a PDF file on the go without an mobile app

For many products, getting deals done on the go means installing an app on your phone. We’re happy to say at airSlate SignNow we’ve made singing on the go faster and easier by eliminating the need for a mobile app. To eSign, open your browser (any mobile browser) and get direct access to airSlate SignNow and all its powerful eSignature tools. Edit docs, underwrite esigning Request and more. No installation or additional software required. Close your deal from anywhere.

Take a look at our step-by-step instructions that teach you how to underwrite esigning Request.

- Open your browser and go to signnow.com.

- Log in or register a new account.

- Upload or open the document you want to edit.

- Add fillable fields for text, signature and date.

- Draw, type or upload your signature.

- Click Save and Close.

- Click Invite to Sign and enter a recipient’s email if you need others to sign the PDF.

Working on mobile is no different than on a desktop: create a reusable template, underwrite esigning Request and manage the flow as you would normally. In a couple of clicks, get an enforceable contract that you can download to your device and send to others. Yet, if you want a software, download the airSlate SignNow app. It’s secure, quick and has an intuitive design. Take advantage of in easy eSignature workflows from the workplace, in a taxi or on a plane.

How to sign a PDF file utilizing an iPhone

iOS is a very popular operating system packed with native tools. It allows you to sign and edit PDFs using Preview without any additional software. However, as great as Apple’s solution is, it doesn't provide any automation. Enhance your iPhone’s capabilities by taking advantage of the airSlate SignNow app. Utilize your iPhone or iPad to underwrite esigning Request and more. Introduce eSignature automation to your mobile workflow.

Signing on an iPhone has never been easier:

- Find the airSlate SignNow app in the AppStore and install it.

- Create a new account or log in with your Facebook or Google.

- Click Plus and upload the PDF file you want to sign.

- Tap on the document where you want to insert your signature.

- Explore other features: add fillable fields or underwrite esigning Request.

- Use the Save button to apply the changes.

- Share your documents via email or a singing link.

Make a professional PDFs right from your airSlate SignNow app. Get the most out of your time and work from anywhere; at home, in the office, on a bus or plane, and even at the beach. Manage an entire record workflow effortlessly: build reusable templates, underwrite esigning Request and work on documents with partners. Turn your device right into a powerful company instrument for closing contracts.

How to eSign a PDF taking advantage of an Android

For Android users to manage documents from their phone, they have to install additional software. The Play Market is vast and plump with options, so finding a good application isn’t too hard if you have time to browse through hundreds of apps. To save time and prevent frustration, we suggest airSlate SignNow for Android. Store and edit documents, create signing roles, and even underwrite esigning Request.

The 9 simple steps to optimizing your mobile workflow:

- Open the app.

- Log in using your Facebook or Google accounts or register if you haven’t authorized already.

- Click on + to add a new document using your camera, internal or cloud storages.

- Tap anywhere on your PDF and insert your eSignature.

- Click OK to confirm and sign.

- Try more editing features; add images, underwrite esigning Request, create a reusable template, etc.

- Click Save to apply changes once you finish.

- Download the PDF or share it via email.

- Use the Invite to sign function if you want to set & send a signing order to recipients.

Turn the mundane and routine into easy and smooth with the airSlate SignNow app for Android. Sign and send documents for signature from any place you’re connected to the internet. Generate professional-looking PDFs and underwrite esigning Request with a few clicks. Created a faultless eSignature workflow using only your smartphone and boost your total productiveness.

Get legally-binding signatures now!

FAQs

-

How long does underwriting take after conditional approval?

Under normal circumstances, your purchase application should be underwritten within 72 hours of underwriting submission and within one week after you provide your fully completed documentation to your loan officer. -

What happens after underwriting?

After a first review, the underwriter will issue a list of requirements. These requirements are called \u201cconditions\u201d or \u201cprior-to-document conditions.\u201d Your loan officer will submit all your conditions back to the underwriter, who then issues an \u201cokay\u201d for you to sign loan documents. -

What does the underwriter look for?

An underwriter is a financial expert who takes a look at your finances and assesses how much risk a lender will take on if they decide to give you a loan. More specifically, underwriters evaluate your credit history, assets, the size of the loan you request and how well they anticipate that you can pay back your loan. -

Can an underwriter deny a loan?

Your loan is never fully approved until the underwriter confirms that you are able to pay back the loan. Underwriters can deny your loan application for several reasons, from minor to major. Some of the minor reasons that your underwriting is denied for are easily fixable and can get your loan process back on track. -

Can a loan be denied after conditional approval?

A conditional approval is when a mortgage underwriter feels comfortable in issuing a full mortgage loan approval once all the conditions are met: ... Borrowers can get denied for mortgage after conditional approval if they cannot meet conditions. -

What conditions do underwriters ask?

Then, a human takes over and here come the conditions: Your first set of conditions is the signNowwork that proves your income and assets. You may also have to show a divorce decree or business license or explain a credit problem. Other hurdles include prior-to-documentation or prior-to-funding requirements. -

What happens after underwriter approves loan?

After a first review, the underwriter will issue a list of requirements. These requirements are called \u201cconditions\u201d or \u201cprior-to-document conditions.\u201d Your loan officer will submit all your conditions back to the underwriter, who then issues an \u201cokay\u201d for you to sign loan documents. -

Does appraisal happen before underwriting?

Home appraisal: The mortgage lender will order an appraisal shortly after the purchase agreement has been signed, in most cases. ... Mortgage underwriting: The loan file then moves on to the underwriter, who reviews all of the documents and determines whether or not the borrower can move on to closing. -

Why would a USDA loan get denied?

Income and debt issues. Things like unverifiable income, undisclosed debt, or even just having too much household income for your area can cause a loan to be denied. Talk with a USDA loan specialist to get a clear sense of your income and debt situation and what might be possible. -

Can my loan be denied underwriting?

Yes, your loan can be rejected during the underwriting stage. But it's more accurate to say that the underwriter can cause your mortgage to be rejected. He or she probably won't make the final decision to reject the loan. Instead, the underwriter will usually pass recommendations along to the bank or mortgage company. -

Why does underwriting take so long?

Underwriters often request additional documents. Underwriting is the most intense review. ... Underwriters often request additional documents during this stage, including letters of explanation from the borrower. It's another reason why mortgage lenders take so long to approve loans. -

Do underwriters deny loans often?

Yes, the Underwriter Can Reject Your Loan The answer is yes. He or she can make a negative decision regarding your file, and that decision can cause your loan to be rejected. First-time home buyers / borrowers often ask if they can be turned down for a loan, after they've been pre-approved by the lender. -

Is a conditional approval a good sign?

While receiving conditional approval is a great sign of your ability to buy a home, it is not a sure thing. -

What credit score do you need for USDA loan?

USDA Loan Credit Score Requirements. The USDA does not set a minimum credit score requirement, but most lenders require a score of at least 640, which is the minimum score needed to qualify for automatic approval using the USDA's Guaranteed Underwriting System (GUS).

What active users are saying — underwrite esigning request

Underwrite countersign order

in a nutshell underwriting is a service usually provided by a large financial institution that involves it taking on risk in exchange for a profit the service but its name due to the fact that in the past bankers would take on risks associated with projects such as sea voyages with them while writing their names under the risk information section nowadays underwriters are involved in anything from the banking and insurance industries to securities for example with initial public offerings as an overly simplified example one company a decides to list its shares on the open market through an initial public offering a concept covered in another video - underwriter a is a major financial institution that believes company a is an excellent business 3 as such underwriter a buy securities issued by company 8 and later on sells them on the open market at a higher price so that it is rewarded for taking on risk in the end 1 the people behind Company A are happy because they received a bunch of money - underwriter a is happy because it was able to sell Company a shares for more 3 it remains to be seen based on how Company A share prices evolved if the investors who bought from underwriter AE will be pleased or not however please note that this is an optimistic example there is the possibility of the market not being interested in buying from underwriter a at a satisfactory price the possibility of underwriter a quote unquote tricking company a at the selling at ridiculously low prices and so on let's just say when when situations aren't guaranteed all in all though this much is certain there's a clear role in the financial ecosystem for well-funded underwriters who put their capital on the line if rewarded properly

Show moreFrequently asked questions

What is needed for an electronic signature?

How do I sign a PDF without using a digital signature?

Can I create a doc and add an electronic signature?

Get more for underwrite esigning Request with airSlate SignNow

- Print electronically sign Free Graduation Certificate

- Prove electronically signed Security Proposal Template

- Endorse digisign Exclusivity Agreement Template

- Authorize electronically sign Buy Sell Agreement

- Anneal mark Bid Proposal

- Justify esign Financial Affidavit

- Try countersign Freelance Design Contract Template

- Add Cooperation Agreement eSignature

- Send Housekeeping Contract Template autograph

- Fax Promotion Acceptance Letter digital sign

- Seal Concert Press Release signed electronically

- Password Severance Agreement Template electronically sign

- Pass Purchase Order countersignature

- Renew Real Estate for Sale by Owner mark

- Test Creative Brief signed

- Require Intellectual Property Sale Agreement Template digi-sign

- Comment undersigned electronically signing

- Champion heir sign

- Call for patron countersign

- Void Privacy Policy template digisign

- Adopt Intercompany Agreement template electronic signature

- Vouch Concert Ticket template signed electronically

- Establish Simple Receipt template sign

- Clear Construction Proposal Template template electronically signing

- Complete Foster Application template mark

- Force Articles of Incorporation Template template eSign

- Permit Honeymoon Reservation Record template eSignature

- Customize Bill of Sale template autograph